It's Jobs Day and the Game Is Afoot for Investors

Everything and anything can and very likely will change this morning. Plus, have bond vigilantes gone into hiding?, the S&P 500's 'unencumbered' position, and Stephen Miran's 'odd' job stance.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Where have the bond vigilantes gone? Surely, they have not changed their minds this quickly. Correct?

The 30-year long bond paid just about 5% at its lows on Tuesday and then again at its lows on Wednesday. We did mention at the time that the 5% yield level was key support for U.S. 30-year. Overnight, ahead of the August labor market report, that yield dropped as low as 4.84%. The benchmark U.S. 10-year Note paid more than 4.3% earlier this week, but as little as 4.15% overnight.

The slope of the U.S. Treasury yield curve was steepening just a couple of days ago as inflation appeared to be heating up and as economic activity had obviously decelerated. The vigilantes were out in force. Just one thing about the bond vigilantes these days. Same as with equities traders, algorithms have been written to replace human traders across the industry in order to save on overhead.

Sure, fundamentals matter over time. We have to believe that, but at the moment nothing matters more than momentum. Nothing matters in the short-to medium-term more than headlines and no trader on earth can scan headlines and even published articles for keywords more quickly than can these high-speed, high-frequency trading algorithms. Right now, they seem to be sniffing out a weak-ish labor report that will reinforce the idea that Jerome Powell's FOMC will reduce the target range for the overnight rate on September 17.

A few days ago, that didn't matter. Only picking off the true believers of stagflation and stagnation, which may very well be real, at the long end of the curve mattered. Now, the reality of a more dovish Fed sets in. We think. Everything and anything can and very likely will change at 8:30 a.m. ET this morning. The game afoot is called risk management and you and I are the players. So, let's dance.

Oh, has anyone else noticed that the U.S. 30-day T-Bill is paying 4.22% this morning, which is inverted against everything through the 10-year Note (signaling a tough economy), but that's also down from 4.32% just a couple of days ago (signaling a dovish looking jobs report)?

Eww, Gross

Automatic Data Processing, also known as ADP, went to the tape with that firm's estimate for private sector job creation for the month of August on Thursday. The print was disappointing as ADP posted just 54,000 seasonally adjusted hires for the month, well below its estimate for 106,000 created positions in July and well below the 73,000 jobs that economists were looking for.

Where is the action across the private sector? According to ADP, the Leisure and Hospitality category added more than 50,000 jobs in August. That was offset by losses of 17,000 jobs across the Trade, Transportation and Utilities category and losses of 12,000 jobs across Education and Health Care. What's that? Correct, educators don't usually have a bad month in August. As for wage growth, pay for job-stayers is now up 4.4% year over year according to ADP, while pay for job-changers is up 7.1%.

Services Sector Strength?

Sort of. With warts, though.

The Institute for Supply Management released their non-manufacturing or "services sector" PMI for August on Thursday morning. The headline number crossed the tape at 52, up from a barely positive 50.1 in July and good for a third consecutive month in a state of expansion (above 50). New Orders were a source of strength at 56, up from 50.3 and also good for a third straight month of expansion.

However, the orders that those New Orders are replacing, Backlogged Orders, printed at a very weak 40.3, down from 44.3 and for that component, and a sixth straight month in a state of contraction. Yes, New Orders are more important, but to see order backlogs wiped almost clear is rather startling.

There are other problems. Despite three months of increasing New Orders, services sector Employment printed at 46.5, a third straight month of contraction. Eek, the cat.

It gets worse. Check this out. Services Sector Prices landed at a screaming red-hot 69.2, almost in line with July's white-hot 69.9 and, sit down for this, services sector prices have printed in a state of expansion for 99 consecutive months. That's 8.25 years, gang. That's basically Trump 2 to date, all of Biden and almost all of Trump 1. Yikes.

Markets

As Treasury debt securities rallied Thursday, so did equities. The S&P 500 gained 0.83% on the day, while the Nasdaq Composite tacked on 0.98%. The broader market outperformed the major indexes. The small-to mid-cap indices all gained between 1.26% and 1.5%. The KBW banks added 1.49% and the Philly Semiconductors gained 1.34%. Huzzah!

Ten of the 11 S&P sector SPDR ETFs closed out the Thursday session in the green, led by cyclicals such as the Discretionaries XLY, Industrials XLI and Financials XLF. All three of those funds gained more than a full percentage point on the day. Only the Utilities XLU closed in the red as the bottom three rungs on the daily performance tables were all occupied by defensives.

Among individual stocks, broadline retailers were hot, as Macy's M tacked on a 5.9% gain on top of Wednesday's 20.7% run and Amazon AMZN popped for 4.3%. Among recreational products, Peloton Interactive PTON, which is a "Stocks Under $10" name, gained 6.8% on Thursday.

For the day, winners beat losers by nearly 3 to 1 at both the NYSE and the Nasdaq. Advancing volume took a 63.7% share of composite NYSE-listed trade and a 56.3% share of composite Nasdaq-listed trade.

Aggregate trading volume? Higher on a day-over-day basis across NYSE listings and across the membership of the S&P 500. However, aggregate trade was lower across Nasdaq-listed securities, decreasing slightly the value of the day's positive session.

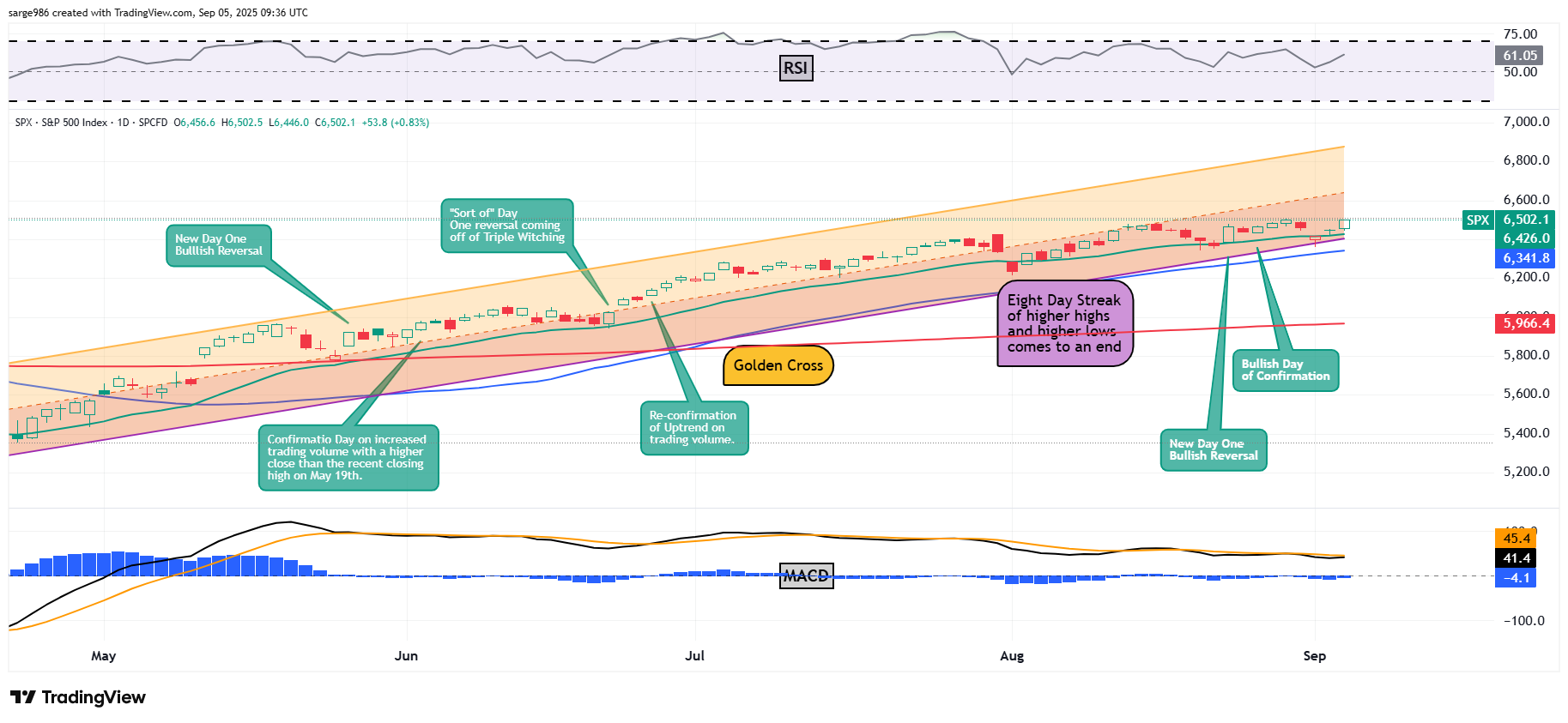

Note that the S&P 500 closed higher than last Friday's high and within six points of creating a new all-time high, which was set last Thursday. This essentially wiped out the idea that there had been a Day One bearish reversal earlier this week and wiped the slate clean.

Basically, the S&P 500 goes into Friday morning's employment report ready for anything and unencumbered by any existing or unfinished technical pattern.

Rock On

On Friday morning, Foxconn, the Taiwanese firm also known as Hon Hai Precision Industry, reported monthly revenue for August that was up 10.7% year over year. Year to date, revenue is up 16.65%, which is a record pace of growth for this firm eight months into the year.

Foxconn released a statement announcing its expectation for Q3 sales growth, both on an annual and sequential basis, and projected that cloud-based and networking product shipments are predicted to rise significantly. By extension, this is likely positive news for either Nvidia NVDA or Apple AAPL or both as Foxconn is a major supplier to both of these tech giants.

Not Quitting

Stephen Miran spent about two hours being interrogated by members of the Senate Banking Committee on Thursday. Miran has been nominated by President Trump to the Federal Reserve's Board of Governors to replace Adriana Kugler, who recently and unexpectedly resigned from her place at the Fed. There are only four months left in the term that Miran has been nominated for, and I guess he can't risk losing his day job, which I find a bit odd.

Miran, who the Democratic Party senators on the committee are skeptics of (to support central bank independence) to begin with, said "I have received advice from counsel that what is required is an unpaid leave of absence from the Council of Economic Advisers." Those employed at the central bank are not supposed to also be employed by the federal government. Miran did later add that he would "absolutely" resign from that position should he be nominated and confirmed for a longer term than the few months that he has currently been nominated for.

I don't see the risk. If the president likes Miran and likes the job he does, he would either nominate him for a full term on the Board of Governors or welcome him back to the Council. If he ticks the president off, he's toast in DC. He'll be teaching economics at a red state university. I see nothing to lose by simply leaving one job for another.

August Employment Situation (08:30 ET)

Non-Farm Payrolls: Expecting 76K, Last 73K.

Unemployment Rate: Expecting 4.3%, Last 4.2%.

Underemployment Rate: Expecting 7.9%, Last 7.9%.

Participation Rate: Expecting 62.1%, Last 62.2%.

Average Hourly Earnings: Expecting 3.9% y/y, Last 3.9% y/y.

Average Weekly Hours: Expecting 34.3, last 34.3 hours.

Other Economics (All Times Eastern)

13:00 - Baker Hughes Total Rig Count (Weekly): Last 536.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 412.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ABM (.95)

At the time of publication, Guilfoyle was long PTON, NVDA equity.