It's All About Eagles, Elon, AI and Earnings

Let's look at the Super Bowl blowout, Trump blitz and why I'm likely taking Lockheed out of my Top 10.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The big game had come and passed. The result was not what too many expected. That said, maybe we should have. The two-time defending Super Bowl champion Kansas City Chiefs had been helped week in and week out by obviously incorrect calls made on the field by league officiating crews. I don't think too many fans would now disagree that this Kansas City team, without distracting from that franchise's recent dynasty, would not have gone 15-2 (15-1 with the starters in) during the regular season without the benefit of bad call after bad call made on the field week after week that prevented their opponents from making key pays at key times during a number of close games.

It becomes very difficult to see the Kansas City Chiefs as one of the top two teams in the National Football League after Sunday night's embarrassing 40-22 loss to the Philadelphia Eagles, a game that was not as close as the lopsided score. Kansas City scored 16 of their 22 points in "garbage time" after the game had been all but decided.

One also has to wonder if the Buffalo Bills, who lost the AFC Championship to Kansas City directly due to several of those bad calls, had been permitted to win that game, if the Super Bowl would have been a more competitive game. KC, carried by bad calls all year, clearly did not belong on that field in New Orleans. It seems reasonable that the Baltimore Ravens, who lost a close playoff game to Buffalo, also would have been a better representative for the AFC in this year's big game.

Major League Good News!

Pitchers & catchers report for spring training this week across all of Major League Baseball.

Super Bowl Trivia

So, the Kansas City Chiefs have failed to become the first NFL /AFL team to win three consecutive Super Bowls. The Miami Dolphins, in the 1970's also made three consecutive appearances, losing one. There is an asterisk here though. The 1965 Green Bay Packers, under Vince Lombardi won the last NFL championship before the Super Bowl between the NFL and AFL champions started playing each other after the next season. Green Bay then won the first two Super Bowls, so there has been a "three-peat."

There has been, however, one player in pro football history that has won three consecutive Super Bowls. Can you name him?

In Trump News...

President Trump made a lot of news over the weekend.

- On Sunday, in an appearance at Fox News, the president stated "I'm going to tell him (Elon Musk at the Department of Government Efficiency) very soon, like maybe in 24 hours, to go check the Department of Education...Then I'm going to go, go to the military. Let's check the military." The president added, "We're going to find billions, hundreds of millions of dollars of fraud and abuse."

- Aboard Air Force One, on the way to the Super Bowl, President Trump told reporters that possibly as soon as Monday (today), he will be placing reciprocal 25% tariffs on all steel and aluminium products imported to the U.S. in addition to already existing tariffs. The president stated simply, "Very simply, it's if they charge us, we charge them." Concerning U.S. Steel X, the president said that Nippon Steel would be allowed to invest in the firm, but not take a majority stake and added, "Tariffs are going to make it (U.S. Steel) very successful again, and I think it has good management."

- Incredibly, also while aboard Air Force One, President Trump told reporters that "We may have less debt than we thought." Elon Musk's DOGE has been investigating the Department of the Treasury, and may have found more fraud, abuse or incompetence there despite being at least temporarily hampered by federal judges. Where won't we find irregularities? My guess is that if the federal government has been spending money anywhere, there is very little chance that it has been done wisely.

- All this does make one think that maybe it's not such a good time to remain long the large defense contractors. Just take a look at the daily chart on Lockheed Martin LMT, where I still have a long (albeit smaller than it used to be) position.

I had taken LMT out of my top five heaviest weighted long positions in late November. It may be time to take this, one of my favorite longs of all-time, out of the Top Ten.

Last Week

Financial markets shaded into the red last week. The week was marked by a softer US Dollar Index and lower bond yields, that is until Friday when President Trump mentioned those tariffs that will likely be implemented early this week. That had a notable algorithmic impact on asset prices. Bitcoin traded sideways, but gold moved higher. Equities trudged along and sold off going into the weekend.

As a matter of fact, tariff talk dominated price discovery last week, more so than the earnings calendar, which was thick and included such heavyweights as Amazon AMZN and Disney DIS. Tariff talk also outweighed the macroeconomic calendar, despite that it was January Jobs Week. The president had placed 25% tariffs on both Canadian and Mexican imports last weekend, but both of those nations had surrendered on the trade front rather quickly. Hence those tariffs were postponed. Tariffs were also placed upon Chinese imports and those were countered. China, I feel, will be a much tougher nut to crack.

The release of the Bureau of Labor Statistics monthly surveys for January was a little tough to discern as the previous two months had been revised higher by about 100,000 jobs created, but the benchmark had been revised lower by 589,000 jobs. What that means is that the rate of recent hiring is stronger than we thought, but that labor markets for most of 2024 were significantly weaker (big shocker) than we thought. One real cause for concern, I thought, was the drop in average workweeks for full-time employees to just 34.1 hours. Given that 34.3 hours is historically the lower end of the range during normal economic conditions, this is potentially the canary in the coal mine and harkens back to numbers we haven't seen since the great financial crisis.

Notable AI Spending

The tech giants appear to have spoken. Alphabet GOOGL, Amazon, Meta Platforms META and Microsoft MSFT all appear to have confirmed huge capital spending on AI infrastructure in 2025, as they had in 2024, despite the potentially less expensive way to go about developing large language models that may have come to light two weeks ago when Chinese start-up Deep Seek made headlines.

Marketplace

Among the major to mid-major U.S. equity indexes....

- The S&P 500 gave up 0.95% on Friday, and 0.24% for the week.

- The Nasdaq Composite gave up 1.36% on Friday, and 0.53% for the week.

- The Nasdaq 100 gave up 1.3% on Friday but was up 0.06% for the week.

- The Russell 2000 gave up 1.19% on Friday, and 0.35% for the week.

- The S&P Small Cap 600 gave up 1.37% on Friday, and 1.17% for the week.

- The S&P Mid Cap 400 gave up 1.26% on Friday, and 1% for the week.

- The Dow Transports gave up 0.32% on Friday, and 0.98% for the week.

- The Philly Semiconductors gave up 1.63% on Friday, and 0.13% for the week.

- The KBW Bank Index gave up 0.74% on Friday but gained 0.76% for the week.

On Friday, all 11 S&P sector SPDR ETFs closed in the red, led lower by the Discretionaries XLY and the Materials XLB. For the week, seven of the 11 S&P sector SPDR ETFs actually closed in the green, as the REITs XLRE and Energy XLE took the lead. Those same Discretionaries that led markets lower on Friday, were the worst performing sector SPDR for the week at -2.84%.

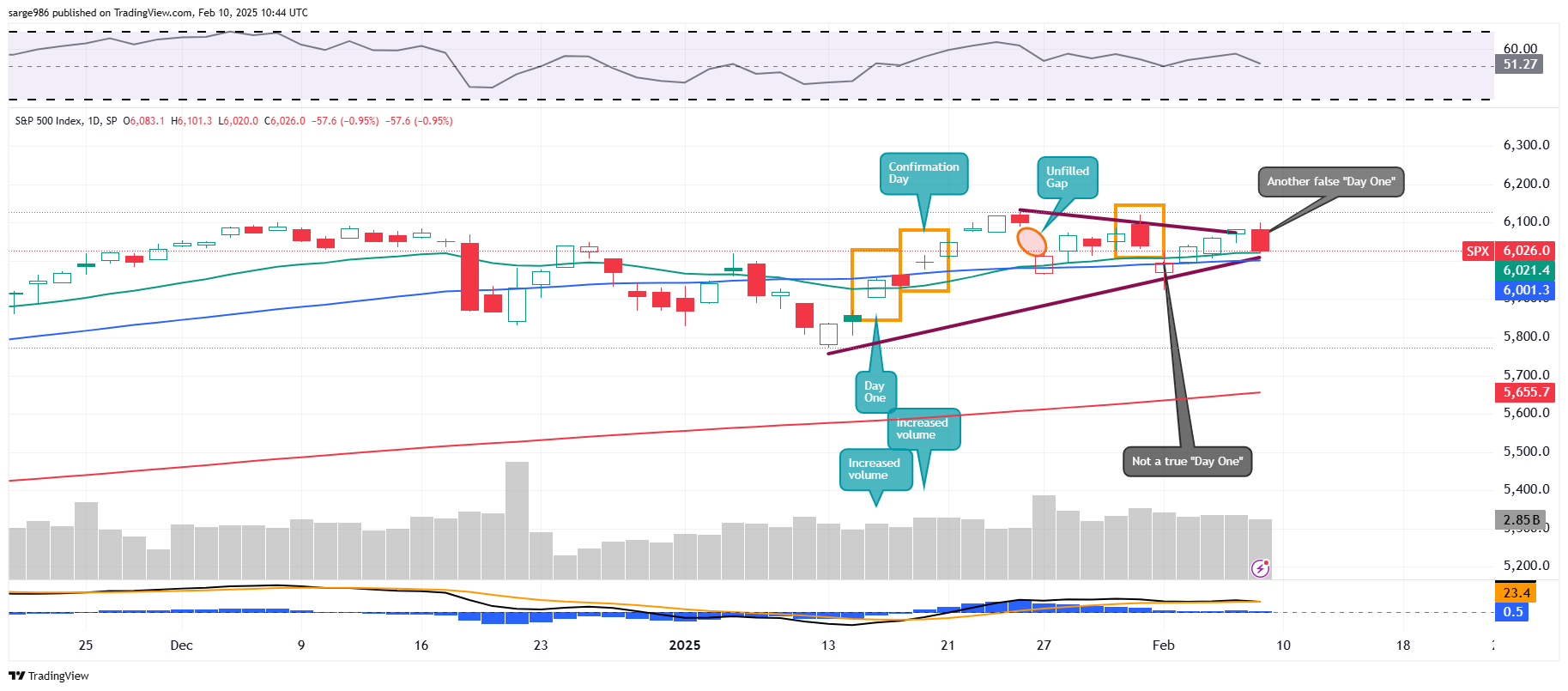

What Do the Charts Say?

Readers will note that the closing pennant formation discussed late last week, continues to close. Keep in mind that closing pennants, flags or triangles often produce explosive moves in one direction or the other. Note that Friday produced another false "Day One" trend reversal as aggregate trading volume across both the listings at the NYSE and the membership of the S&P 500 decreased on a day over day basis.

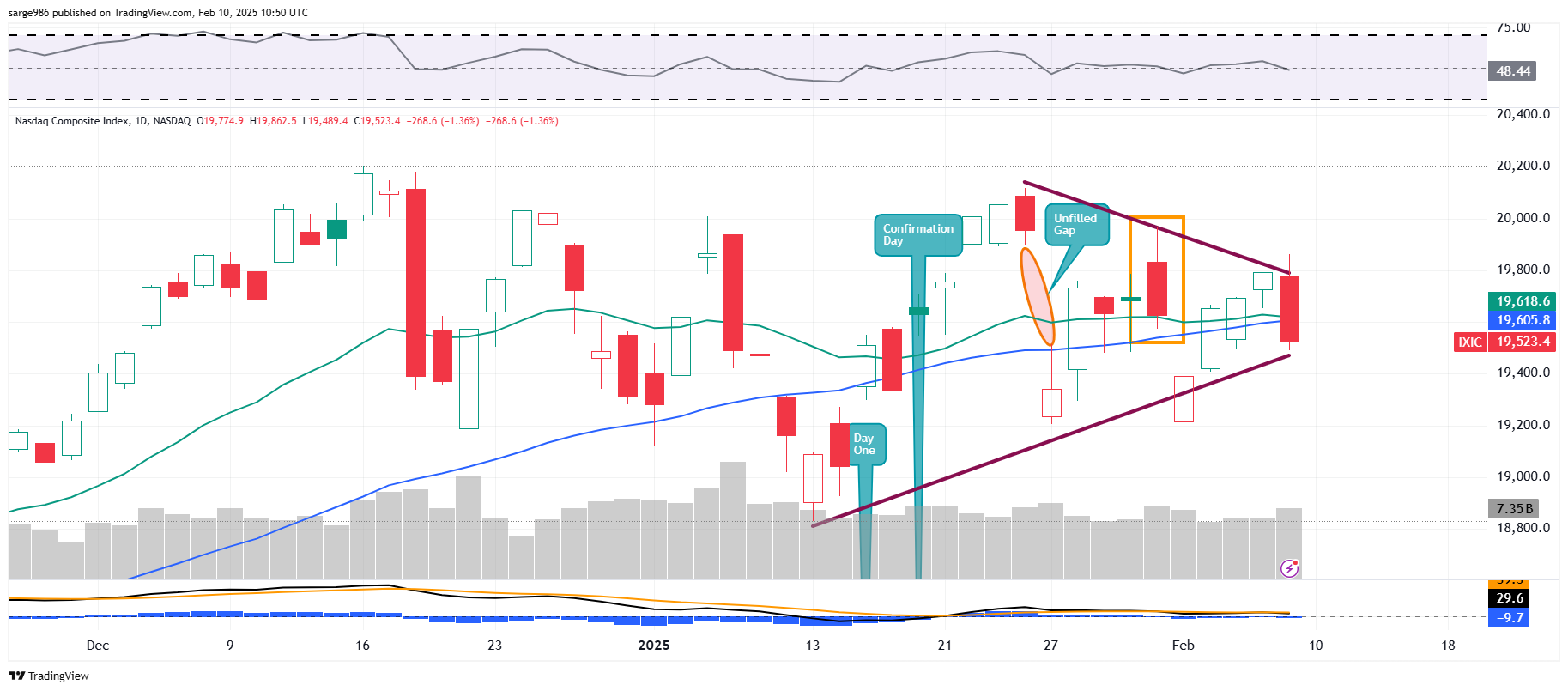

Readers will note that the Nasdaq Composite has produced similar looking activity to the S&P 500.

That said, the Nasdaq Composite is now in a weaker place, technically that the S&P 500 as the volume has been there for this index and unlike the S&P 500, the Nasdaq Composite lost its 50-day simple moving average on Friday and will have to take it back. Note, contact with that line has not been lost and that is key, more than just a simple piercing.

Earnings

According to FactSet, with 62% of the S&P 500 having reported their fourth-quarter earnings, 77% of those firms reporting have beaten earnings expectations, while 63% of those reporting have beaten revenue expectations. At this point, for the quarter, earnings growth is running at a blended (results & expectations) rate of 16.4% (up from 13.2% a week ago) on revenue growth of 5.2% (which is up from 5.0% a week ago).

For the quarter, the Financials are expected to post by far the greatest earnings growth at +51.2%, with Communication Services in second place at +30.2%. Just three sectors are expected to show a year over year earnings contraction, led lower by Energy at -28.8%. The Industrials moved from contraction to expansion last week.

As for the current quarter (Q1, 2025), consensus is currently for earnings growth of just 8.7% (down from 10.1%) on revenue of 4.5%, down from last week's 4.8%. For the full year 2025, Wall Street sees earnings growth of 13% (down from 14.3%) on revenue growth of 5.5%, down from 5.7%. It does appear that at least for the current quarter, analysts are continuing to broadly price in the impacts of tariffs.

As for valuation, the S&P 500 went into the weekend trading at 22.1 (up from 22.0) times 12-month forward looking earnings and 28.4 (up from 28.3) times 12-month trailing earnings. These ratios both remain well above their respective five-year and ten-year averages.

What's Ahead?

Aside from the likely announcement of new tariffs this week there are several issues on our collective plates for this week as Monday morning gets rolling along.

......The Fed. Fed-speak takes center stage this week as fed Chair Jerome Powell will testify on Tuesday morning before the Senate Banking Committee. On Wednesday, Powell will have to do it all over again, before the House Financial Services Committee. Fed Funds futures markets are currently pricing in a 92% probability for no rate changes on March 19 and have pushed the likelihood (59%) for a first quarter-point rate cut out to July 30 from June 18.

.... The Macro will be key as well this week. On Wednesday and Thursday, January inflation will be in focus as the Bureau of Labor Statistics releases its data for both consumer and producer level inflation. Away from inflation, January Retail Sales and January Industrial Production will both be released on Friday.

.... This will be another very heavy week of earnings releases, but the number of headline level releases will be way down. Well-known names putting the results to the tape will be McDonald's MCD on Monday, as well as Coca Cola KO, Lyft LYFT and Super Micro Computer SMCI on Tuesday. After that, we'll hear from Cisco CSCO on Wednesday, and Deere DE, Airbnb ABNB and Palo Alto Networks PANW on Thursday.

Super Bowl Trivia Answer...

Q) There has been one player in pro football history that has won three consecutive Super Bowls. Can you name him?

A) Linebacker Ken Norton Jr (Son of former heavyweight boxing champ and former United States Marine Ken Norton Sr) is the only player in NFL history to win three consecutive Super Bowls, starring for the 1992 & 1993 Dallas Cowboys and the 1994 San Francisco 49ers.

Economics (All Times Eastern)

No significant domestic macroeconomic data scheduled for release.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: MCD (2.86), MNDY (.79), ON (.97)

After the Close: COTY (.21), VRTX (4.02

At the time of publication, Guilfoyle was long LMT, AMZN, MSFT equity.