Is This Weakness a Warning ... or an Opportunity?

Investors who don't eye the markets minute-by-minute: Now is time to start accumulating risk assets. Also, a look at the Middle East, 'triple tops' on the S&P and why & when we could rally.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Worth Fighting For

So, I wander on

Asking where you might have gone

From what I knew before

Some things are worth fighting for

I'm heading in the wind

Head bowed down from what I saw

May shadow for a friend

There's some things are worth fighting for

- Tipton, Downing, Halford (Judas Priest), 2005

Worth Fighting For?

That is a question for someone else. Over the weekend, the Department of Defense / War ordered the deployment of the USS Gerald R Ford carrier strike group to the Middle East. One would imagine that with more than 30 warships in the region once all forces are in place, the Iranian regime might be forced to negotiate in earnest. This particular carrier group had been stationed in the Caribbean Sea and should be properly positioned for whatever is needed within two weeks.

I do not know the particulars, but last week, I had suggested that perhaps the USS George H W Bush carrier strike group off of Virginia's coast that was just coming off of training exercises might be best suited for a potentially hot deployment. We don't know if certain ships within the Bush group need to be refitted after those exercises. That's a distinct possibility.

We do know that the Ford group has been on task for 238 days and that number will be over 250 once the group is positioned with the USS Abraham Lincoln carrier strike group in the CENTCOM region. I'm no naval tactician, but I do know that sailors get tired and extended periods of combat readiness do weigh upon readiness both in terms of human response and in the wear and tear on equipment. The post-Vietnam War record length for remaining "on task" for a carrier strike group is 285 days.

Pay Close Attention

The past week closed on a somewhat dour note as an attempted rally across equity markets fizzled out on Friday, despite a weaker-than-expected report on January consumer-level inflation released that morning. Of course this came just two days after a stronger-than-expected January labor market report that these markets, which had started the week out on some strength, fall back into their current AI-inspired abyss.

One thing is certain, bond traders and investors are not falling for last week's labor market "head-fake." The U.S. Ten-Year Note paid just 4.05% by Friday evening after having paid more than 4.2% as recently as Wednesday morning. This morning, coming off of a market holiday on Monday, I see the yield for U.S. Ten-Year paper at less than 4.03%.

I think it is key to remember that as investors seek safe haven in the more defensive sectors of our equity marketplace and in U.S. Treasury debt securities, that lower yields equal lower interest rates and lower interest rates, in turn support not only labor markets, but riskier behavior both at the household and business to business levels.

Financial markets will, in my opinion, respond to these present conditions over the medium to long-term with a potentially aggressive stock market rally. Perhaps, once Kevin Warsh succeeds Jerome Powell as Fed Chair this May, and short-term rates can be permitted to approach levels less restrictive, that rally could accelerate. So, is the present market weakness, a warning or is this opportunity?

My instincts tell me that at least for investors who do not keep their eyes on the markets on a minute-by-minute basis, that this is a time to start accumulating risk assets. For traders who are more focused on the short-term, you already know the answer. Volatility is your friend, but you kids are more than capable of defending yourselves. It's the folks who do something else occupationally that I am concerned for. Some of those folks are trying to manage their own dough and others are subject to financial advice designed to benefit the adviser or the adviser's employer more so than the client. "Fiduciary" can be a funny word and funny words can be twisted.

The Week That Was...

Late in the past week, equities disappointingly gave up gains made earlier in the week. This came partially in response to the strong January jobs report and the weak retail sales numbers for December. Not even a softer-than-expected print for consumer-level inflation in January could do much to turn the late weak tide. This is how equity markets performed over the past week:

- The S&P 500 gained just 0.05% on Friday but still gave up 1.39% for the week.

- The Nasdaq Composite gave up 0.22% on Friday, and an ugly 2.1% for the week.

- The Nasdaq 100 added 0.18% on Friday but lost 1.37% for the week.

- The Russell 2000 gained 1.18% on Friday but surrendered 0.89% for the week.

- The S&P Small Cap 600 popped for 1.14% on Friday but gave back 0.82% for the week.

- The S&P Midcap 400 gained 0.89% on Friday but lost 0.82% for the week.

- The Dow Transports gained 1.67% on Friday but lost a tough 2.76% for the week.

- The Philly Semis gained 0.66% on Friday and 1.11% for the week.

- The KBW Bank Index added 0.29% on Friday but was down 5.53% for the week.

On Friday, nine of the 11 S&P sector SPDR exchange-traded funds closed out the session in the green, led, unfortunately, by sectors with defensive characteristics. The Utilities (XLU) , the REITs (XLRE) and Health Care (XLV) were the winners, while Communication Services (XLC) and the Financials (XLF) were the losers.

For the week, six of the eleven S&P sector SPDR ETFs traded higher, with the Utilities and REITs again way out in front. Again, the Financials were the most significant victims of capital outflows.

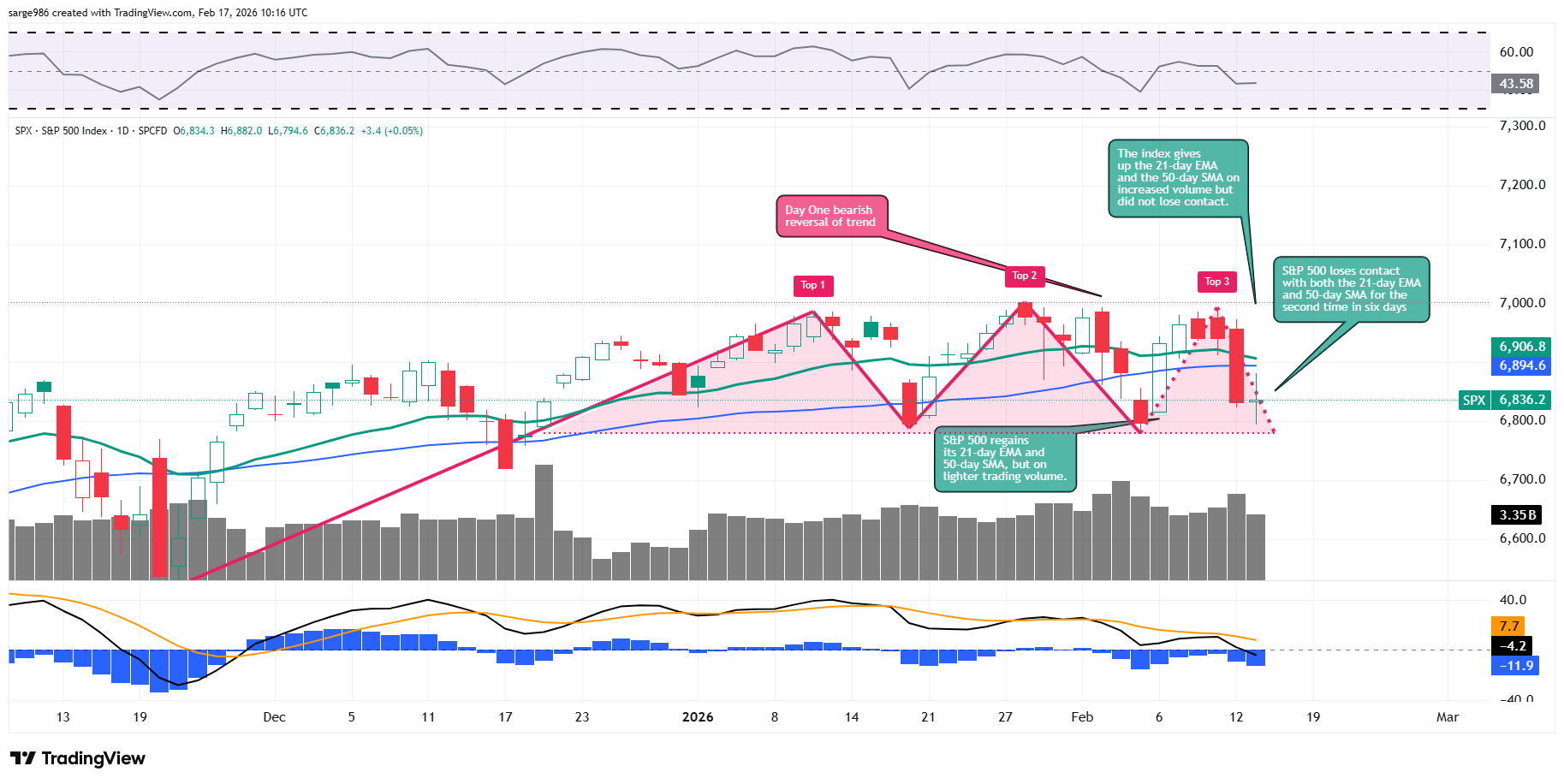

The Charts

Readers will see that last week, the S&P 500 developed what looks like a third top since the start of the new year. The bad news, at least for the time being, would be that triple tops, though less common than double tops, are also patterns of bearish reversal. Readers also need to note that on Friday, the S&P 500 lost contact with both its 21-day exponential moving average and 50-day simple moving average. This could force professional traders out of member stocks on Tuesday morning with the swing crowd taking a powder.

That said, relative strength has hung in there pretty well and the daily moving average convergence divergence, though mildly bearish in posture, is not in as awful a condition as one might expect. Does this suggest a more shallow or less severe selloff? I think it might. The downside pivot is currently 6,780. That is the level to watch. Should support be found at or above that level, this "potential" triple top will turn into nothing more than a basing period of consolidation, also known as a "flat base." Markets can break out of these patterns in either direction. I know you bulls just caught that line.

Earnings

As of Feb. 13, according to FactSet, for the fourth quarter, Wall Street sees a year-over-year blended (results and projections) earnings growth for the S&P 500 of 13.2%, up from 13% last week and up sharply from 8.2% just three weeks prior. Wall Street also sees revenue growth of 9%, up from 8.2% two weeks ago. Simply put, as mentioned here last week, despite the stock market volatility, corporate execution has been excellent.

With 74% of the S&P 500 having reported, 74% of S&P 500 member firms have reported earnings beats while 73% have beaten consensus for revenue generation. For the full year (2025), the street now sees earnings growth of 13.3% on revenue growth of 7.5%. For the full year 2026, Wall Street now sees earnings growth of 14.4% on revenue growth of 7.5%.

At the moment, technology, at earnings growth of 30.7%, and the industrials, at growth of 26%, as well as communication services (+13.6%) are the only sectors projected to experience double-digit bottom-line growth for the fourth quarter. Just two sectors (discretionaries and energy) are projected to suffer a year-over-year earnings contraction, as health care has escaped that grouping.

By the way, if the annual growth rate for Q4 corporate revenue generation holds at 9% or greater, that would be the strongest pace for this metric since the third quarter of 2022. This is up from an initial consensus view for growth of just 6.5% as that quarter began.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 21.5-times 12 months' forward-looking earnings, flat from the week prior. This is well above the five-year average of 20.0-times for the index as well as well above its ten-year average of 18.8-times.

The S&P 500 also ended last week trading at 28 times trailing 12 months' earnings, up from 27.9 times. That also stands well above the five-year (24.9 times) and 10-year (23.1 times) averages for the index.

Ten of the 11 sectors are now trading above their five-year average valuations, led by Consumer Discretionaries (27.1 times), the Industrials (26.2 times) and Tech (24.3 times). Only the real estate investment trusts (at 18.3 times) are not historically overvalued relative to their five-year averages. The utilities escaped this distinction just last week.

The GDP Game

Last week, the Atlanta Fed revised its GDPNow model estimate for Q4 economic growth down to 3.7% from growth of 4.2% (q/q, SAAR). Among other regional central bank district branches running close to real-time Q4 GDP models, the New York Fed revised its Q4 model higher to growth of 2.71% from 2.69%.

The Cleveland Fed left their model unrevised, at growth of 3.08%. Lastly, the St. Louis Fed, which has been highly inaccurate throughout 2025, revised its estimate down to -0.17% from growth of 0.1%. St. Louis remains the outlier.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in just a 10% probability for a quarter percentage point rate cut at the next Federal Open Market Committee policy meeting on March 18, down from 15.8% a week ago. The next rate cut is priced in for June 17 at this point (66% likelihood). At present, there is still a half percentage point worth of additional rate cuts fully priced in (70% chance, down from 72%) for all of calendar 2026.

On The Docket...

The holiday-shortened week ahead will likely be a little difficult to traverse. Though earnings season, at least at the headline level will let up a bit, there will be Fed speakers and there will be some macro. Let's not forget that there will also be pressure.

Short weeks and short months, of which we are currently engaged in both, present challenges to those without base salaries. Every trader, every broker and most managers are surviving without a safety net.

These folks survive either on commission or their own skill (and luck) to produce income. They have to average a certain number per day to meet their financial obligations and when there are less trading days to work with, that number rises. Hence, as the week and month wind down, the pressure will rise and very likely so will the risk-taking.

.... Our central bankers will be moderately active this week. We'll hear from Fed Gov. Michelle Bowman on both Wednesday and Thursday. Minneapolis Fed Pres Neel Kashkari will speak on Thursday. Minneapolis does hold policy voting rights for 2026, so keyword reading algorithms will focus on his words. On Wednesday afternoon, the Fed will also publish the FOMC Minutes of the January meeting. With a lame duck Fed Chair, I don't really know if markets will react all that much to this release.

.... The macroeconomic calendar will also be "moderately active" this week. There will be regional manufacturing-focused survey results for February released by both the New York and Philadelphia Feds. December Durable Goods Orders will hit the tape on Wednesday morning. As the week winds down, the Bureau of Economic Analysis will publish the agency's first estimate for Q4 gross domestic product on Friday morning alongside its data concerning December personal income, personal spending and inflation.

.... The earnings calendar will be active again this week, but there will be a real lack of headline-quality names reporting. Among the more well-known names that will post results will be Palo Alto Networks (PANW) this evening, as well as Booking Holdings (BKNG) , Carvana (CVNA) and DoorDash (DASH) on Wednesday. Thursday morning will bring us Walmart (WMT) and Wayfair (W) in the morning followed by Dropbox (DBX) that afternoon.

Need to Know

- The Chinese Lunar New Year kicks off today (Tuesday). One would think that consumer-focused stocks could be impacted.

- India is hosting one of the largest artificial intelligence focused events ever this week. French Pres. Emmanuel Macron will deliver the keynote address this Thursday. Participation in the event will include corporate leaders from Alphabet (GOOGL) , OpenAI, Anthropic, Meta Platforms (META) , Microsoft (MSFT) and Advanced Micro Devices (AMD) . Very interesting, Nvidia (NVDA) will be absent from India this week.

Economics

(All Times Eastern)

08:15 - ADP Employment Change (weekly): Last 6.5K.

08:30 - Empire State Manufacturing Index (Feb): Expecting 5.5, Last 7.7.

10:00 - NAHB Housing Market Index (Feb): Expecting 38, Last 37.

The Fed

(All Times Eastern)

12:45 p.m. - Speaker: Reserve Board Gov. Michael Barr.

2:30 - Speaker: San Francisco Fed Pres. Mary Daly.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (LDOS) (2.61), (MDT) (1.33), (VMC) (2.11)

After the Close: (CDNS) (1.91), (PANW) (.94), (TOL) (2.11)

At the time of publication, Guilfoyle was long AMD, NVDA equity.