Is Nvidia Just Too Good for Its Own Good?

Earnings beat and so did sales growth, but the report is getting somewhat muted reaction overnight. Also, Snowflake and Salesforce report, and we chart the markets.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

High profile U.S. chip designer Nvidia NVDA reported fiscal fourth-quarter financial results on Wednesday evening, revealing an unadjusted earnings per share of $0.89 (beating expectations) on revenue of $39.33 billion (crushing expectations). Forward sales guidance was strong. The numbers within the numbers still impressed as data center (cloud)-driven revenue grew some 93% year over year with the large cloud computing providers accounting for about 50% of those sales.

Oh, and at least according to CEO Jensen "The Fonz" Huang, he's "more enthusiastic today" in regard to demand for Blackwell architecture products than he was back at the CES consumer electronics show in Las Vegas in early January. Still, the stock, while up small as we work our way through the zero-dark hours, has experienced a rather muted response. Did investors need more? Maybe. The company has a history of simply shocking Wall Street with blowout results. I am not sure that Wall Street is still "shockable" with numbers of any kind.

Sales growth, which was up 78% across the company, would be incredible for literally every other large company on the planet. For Nvidia, however, this pace of growth is a deceleration from 94% for the quarter prior and 122% for the quarter before that. This can't be helped. Call it the law of large numbers. Call it what you want. This pace of growth will continue to reflect a year-over-year deceleration for the rest of this fiscal year, ending up in the mid 40% range. Just remember that most of the S&P 500 would lust after sales growth that even approaches 20%.

Other Sarge Names Reporting...

Big-data numbers cruncher and AI-software platform provider Snowflake SNOW beat Wall Street's expectations for both earnings and revenue, while sales grew 27% year over year. That stock is up more than 11% overnight as the company provided slightly better than expected guidance. Snowflake is a potential competitor at least on some levels to Sarge fave Palantir Technologies PLTR.

However, Salesforce CRM beat Wall Street's consensus view for its adjusted bottom-line performance, but failed to meet expectations for its top-line number as sales grew just 7.5% from the year-ago comparison. The stock is down almost 5% overnight as the guidance provided was also disappointing.

Marketplace

Equity markets were more or less quiet on Wednesday ahead of the Nvidia release, as capital continued to pour into Treasury Debt securities. By day's end, the U.S. Ten Year Note paid 4.26% (-4 basis points), as the Two-Year Note went home with a yield of 4.08% 9-2 bps). Very interestingly, the Treasury Department held a very strong auction of $44 billion worth of Seven Year Notes on Wednesday where there was a surge in demand from direct bidders (domestic accounts) as dealers were stuck with only a small portion (8.8%) of the issuance.

But it has to be noted that there was a notable lack of demand from indirect bidders or foreign accounts. Is that meaningful? I'm not sure. The yield spread between the U.S. Ten Year Note and the U.S. Three Month T-Bill inverted on Wednesday for the first time in roughly three months. That spread stands at -1 basis point as night melts into morning.

Readers must understand that the spread between the yields paid by U.S. Ten Year and Three-Month paper is the most accurate predictor we have in economics for the possibility of an oncoming recession. While it's true that this spread was inverted for most of the past two-plus years and gross domestic product in that time never showed a sustained outright contraction, that this was accomplished largely through greatly accelerated levels of deficit spending during and coming out of the pandemic era and that gross domestic income (which is supposed to equal and be a check on GDP) badly underperformed GDP throughout that period making GDP results over that period suspect.

On That Note...

We've been quite sure for some time that consumer inflation for February would slow on a year-over-year basis from January. January consumer price index ran at growth of 3%. Currently, the Cleveland Fed's model shows February CPI at 2.83%, while my friends at Hedgeye (a service I pay for) show February at growth of 2.86%.

Now, without giving away the store, it's impossible to not notice that Hedgeye Macro is now projecting considerably reduced levels of inflation going forward into the second quarter. Disinflation is now expected to last from February through April. You know what this means. When inflation and growth decelerate side by side that changes the investment landscape.

This environment, were it to come to pass, would be where safe-haven assets such as Treasuries and gold continue to flourish, and defensive stock sectors continue to lead. Stock sectors (cyclicals, transports, small caps) more reliant upon economic activity and most industrial commodities would be in danger of underperformance this spring. Hedgeye Macro has never given me reason to doubt their models in the past.

On Stocks

On Wednesday, the S&P 500 essentially closed unchanged (+0.01%) as the Nasdaq Composite gained 0.26%. The Dow Transports gave up 0.3% for the session, as the small-cap Russell 2000 gained 0.19% and the S&P Mid-cap 400 gained 0.16%. The Philadelphia Semiconductor Index was the star of the day, up 2.09% ahead of those earnings last night.

Eight of the 11 S&P sector SPDR exchange-traded funds closed in the green on Wednesday, obviously led by Tech XLK, while investors took profits in the Staples XLP that had led markets during the four-day sell-off. Breadth was OK. Losers beat winners by just a smidgen at the NYSE, but winners beat losers by a rough 4-to-3 margin at the Nasdaq. Advancing volume took a majority share of composite trade for the listings of both exchanges as aggregate trade contracted not only across those listings but also across the membership of the S&P 500.

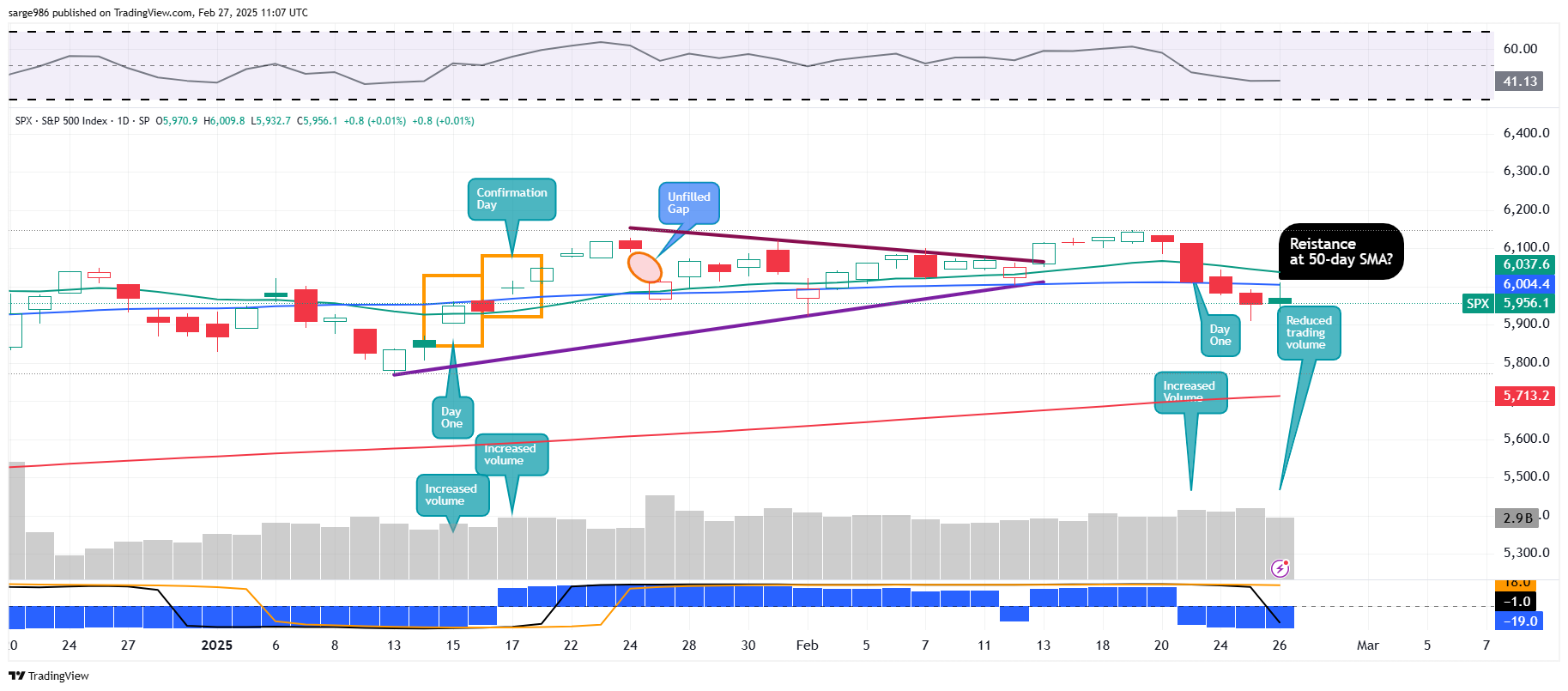

The end of the four-day beatdown means one of two things: Stocks either rally from here and all is well -- I have my doubts -- or, this is the break that markets needed (post that "day one") in order to confirm the bearish change in trend which so far remains unconfirmed.

Note, too, the resistance that the S&P 500 met at its 50-day simple moving averge on Wednesday. Equity index futures are trading higher overnight. We shall find out within hours if this level is going to be an issue or not.

Readers should also be wary that the Nasdaq Composite is nowhere near retaking its 50-day simple moving average and that Wednesday's close fell well short of Monday's close as I would not yet consider anything I see in this chart as clearly constructive.

Note Below...

A lot of key macro is due this morning and the Fed clown car looks to be loaded up with a plethora of grossly under-qualified PhD. economists set to make public appearances. High-speed, keyword reading algorithms will try to control Thursday's market narrative from the "get-go."

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 220K, Last 219K.

08:30 - Continuing Claims (Weekly): Last 1.869M.

08:30 - Durable Goods Orders (Jan): Expecting 1.6% m/m, Last -2.2% m/m.

08:30 - ex-Transportation (Jan): Expecting 0.4% m/m, Last 0.3% m/m.

08:30 - ex-Defense (Jan): Expecting 1.4% m/m, Last -2.4% m/m.

08:30 - Core Capital Goods (Jan): Expecting 0.4% m/m, Last 0.5% m/m.

08:30 - GDP Growth Rate (Q2-rev): Flashed 2.3% q/q SAAR.

10:00 - Pending Home Sales (Jan): Expecting -1.3% m/m, Last -5.5% m/m.

10:30 - Natural Gas Inventories (Weekly): Last -196B cf.

11:00 - Kansas City Manufacturing Index (Feb): Expecting -3, Last -9.

The Fed (All Times Eastern)

10:00 - Speaker: Reserve Board Gov. Michael Barr.

11:45 - Speaker: Reserve Board Gov. Michelle Bowman.

1:15 p.m. - Speaker: Cleveland Fed Pres. Beth Hammack.

3:15 - Speaker: Philadelphia Fed Pres. Patrick Harker.

10:15 - Speaker: Chicago Fed Pres. Austan Goolsbee.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: SJM (2.37), WBD (.15)

After the Close: DELL (2.51), HPQ (.74), RKLB (-.07), SOUN (-.10)

At the time of publication, Guilfoyle was long RKLB, NVDA, SNOW, CRM equity.