If You Expect Smooth Sailing in 2026, You May Be In for a Surprise

Following a strong 2025, are investors positioned for perfection?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The VIX inched up, maybe it was more like centimetered up. I want a spike. I want jumpy. And even the type of reversal we got on Wednesday hasn’t given me that spike I so desire.

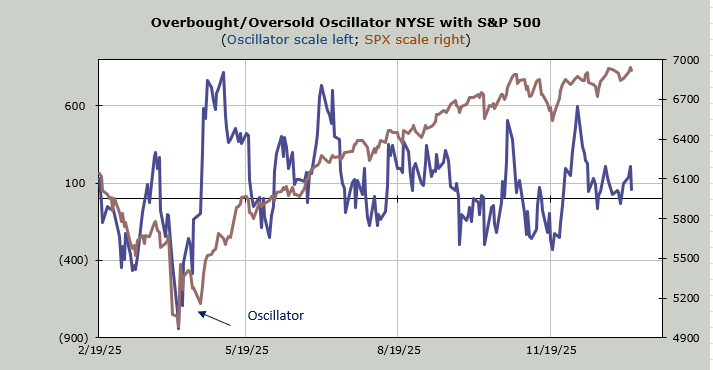

Yes, breadth was poor all day. Remember when NVDA rallies, it tends to do so at the expense of the 493, so it should come as no surprise that breadth was the exact inverse from Tuesday’s market. Tuesday saw net breadth at +800, and Wednesday’s net breadth at -750. But it did not change the McClellan Summation Index. Not yet, at least. It will require some follow-through with a net differential of -200 advancers minus decliners on the NYSE to turn it back down.

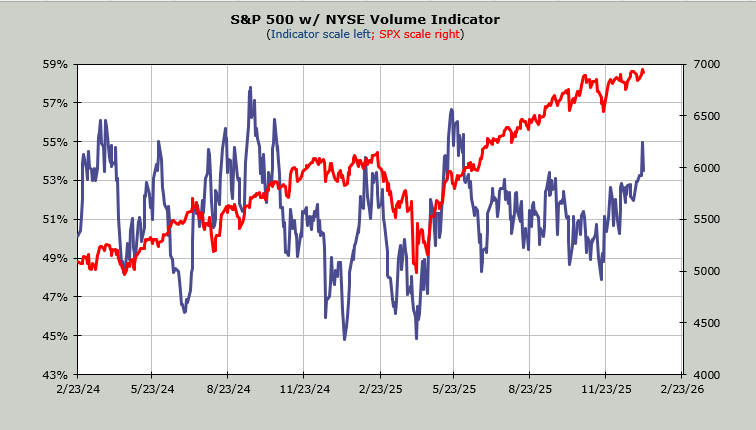

Very few of the indicators changed. As noted here yesterday, the intermediate term (30-day moving average of the advance/decline line) got overbought yesterday. The Volume Indicator got to 55% (overbought) as well. It now stands just over 53%.

There has been no change in the ratio charts we looked at Monday, so there is no need to update them, but we should revisit the chart of the Small Cap 600 (profitable stocks) relative to the IWM (unprofitable stocks) because that shows us that the non-profitable names are outperforming. In fact, the ratio couldn’t even make a higher high than it did in November.

Ah, what the heck, who needs profits?

In terms of sentiment, I saw a headline earlier this week that said Wells Fargo expects the market to rally on short covering. Whoa. Do they really think there are shorts out there? What proof do they have of that?

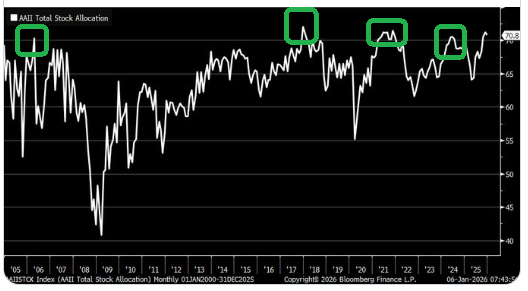

Because you see, the folks at the American Association of Individual Investors (AAII) not only vote each week where they think the market will be six months from now, once a month, they share their allocation to stocks with us.

As of the end of December, their allocation to stocks was fractionally over 70%. So the first thing we should note is that they might say they are bearish, but they are bearish but invested.

In any event, I note here on the chart the last four times they saw their allocation to stocks get over 70%. Each time, they were several months early. I have boxed it off on green. In 2006, they got over 70% but the high in the S&P did not come until about a year later. Of course, the market started swooning about nine months before the actual high (it swooned, rallied back, swooned, rallied back, swooned, and rallied back to the ultimate high).

Their exposure got just over 70% in late 2017, and the market did not peak until September/October 2018 (we had a 20% decline in the fourth quarter), although we did see a few swoons earlier in the year. In 2021, they got over 70% with SPAC-mania in the first quarter, and although the S&P did not peak until November that year, we all know the majority of stocks peaked in that first quarter.

Finally, they got over 70% in December last year, and we did not swoon until March/April. So the timing on a trading basis isn’t brilliant, but it does tell us that it is unlikely this year will be a smooth ride. At least using this metric.