How Should You Build a Portfolio?

Smart investing starts with crafting a atrategy for success

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This is the fifth of ten articles in the Filthy Rich Animal Investing Basics Series.

If you like what you see and are not yet subscribed or would like to share with a friend, please visit this link to join us. It's free!

Is Your Portfolio Optimized or a Bunch of Random "Stuff"?

When you look at your investment statements, do you see various funds or stocks allocated to optimize return while minimizing risk? Or is it a bunch of “stuff” that’s been accumulated over the years for reasons that you may or may not recall?

In recent articles, we've discussed various asset classes, such as equities (stocks) and fixed income (bonds), and how each comes with its own unique blend of risk and reward.

We’ve also explored the time value of money, which illustrates how consistent investing can lead to long-term wealth accumulation. But now, it’s time to put everything together and build a portfolio.

We can’t do this for you, as we know absolutely nothing about your situation. How old are you? How much retirement income do you need? What’s your tax bracket? What’s your current financial situation?

Those are just a few of the questions a planner would review before recommending an investment portfolio.

But we can offer a framework that will serve as a strong starting point.

Key Principles for Building Your Portfolio

- Risk tolerance typically changes with age. When you're young, you have a longer investment horizon, which means you can afford to take on more risk. In contrast, as you approach retirement, it’s generally advised to reduce your exposure to riskier investments, focusing more on stable and conservative assets. There are a few relatively rare exceptions to this, but without a thorough evaluation of your situation, don’t assume you’re one of them.

- Diversification is crucial. You’ve heard it before: A diversified portfolio, including investments spread across various equity and fixed-income asset classes, aims to maximize your returns while minimizing risk. By investing in different market capitalizations, industries and geographical regions, you reduce the impact of any single underperforming asset.

- Consistency is key. The third principle, though very important, is entirely up to you. You need to decide how much money you can invest each month, but the key takeaway here is to invest consistently. Dollar-cost averaging, or just investing a fixed amount on a regular basis, such as with every paycheck, can help reduce the effects of short-term market volatility.

So how do these principles guide the portfolio-building process?

Age and Ability to Tolerate Risk

When you’re younger and have time on your side to recover from any market downturns, you can afford to invest more heavily in growth assets, which means stocks. They can be volatile in the short term but historically outperform other asset classes over the long run.

But the closer you get to retirement, your financial goals shift. You’ll likely want more stability and less volatility. Bonds and other fixed-income investments become more attractive because they provide a predictable income stream and lower risk compared to stocks.

While the stereotypical retirement portfolio consists mostly of bonds, advisors are seeing something different today. With the stock market in a long-term rally mode, many retirees have too large an allocation in their portfolios. So far, it’s worked out for many of them, but it’s still a risky approach.

Target Date Funds: One-Decision Portfolios

If you participate in a 401(k) at work, you likely have access to target date funds, which automatically adjust their asset allocation based on a specific target retirement date.

They are designed to be an all-in-one investment solution. For example, if you plan to retire in 2030, the fund’s glide path adjusts to be more conservative as that date approaches.

For example, Vanguard offers a series of target date funds that adjust their allocations over time. Let’s look at a couple of examples.

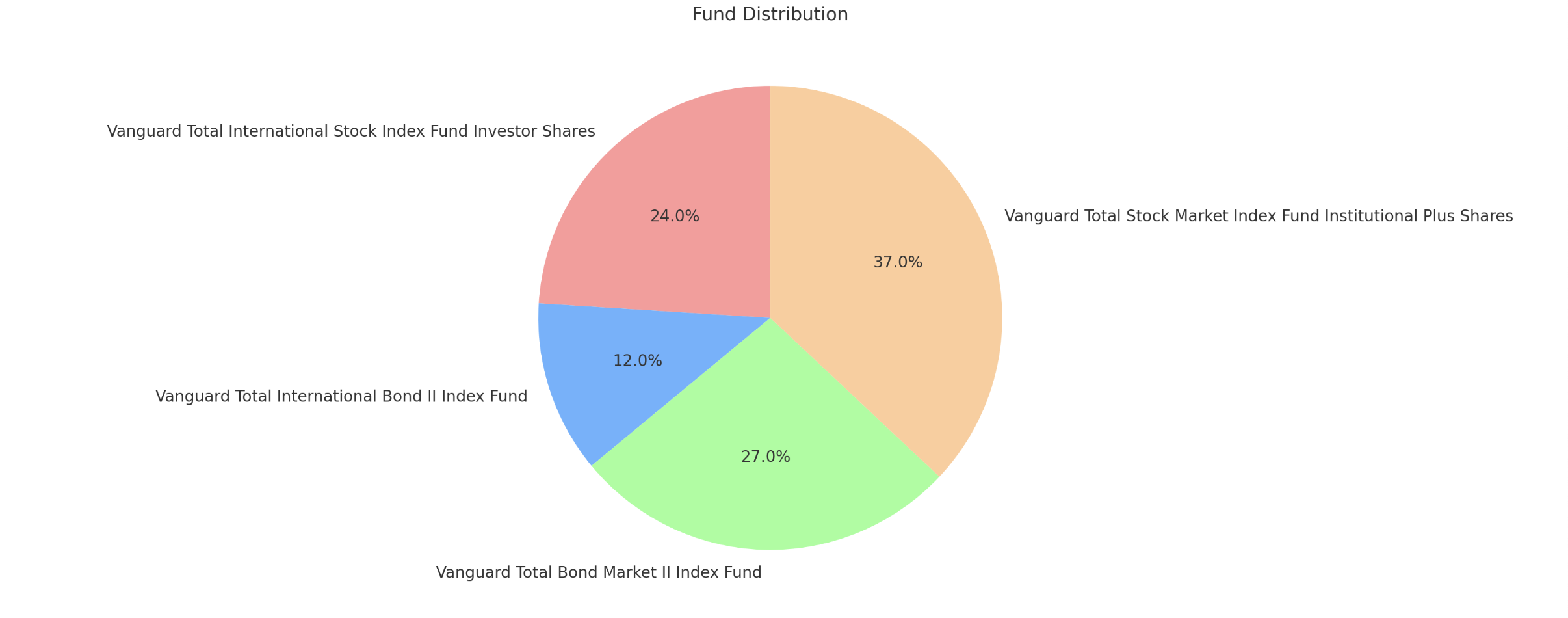

The Vanguard Target Retirement 2030 Fund (VTHRX) has these holdings:

- Vanguard Total Stock Market Index Fund Institutional Plus Shares: 37%

- Vanguard Total Bond Market II Index Fund: 27.20%

- Vanguard Total International Stock Index Fund Investor Shares : 24.20%

- Vanguard Total International Bond II Index Fund 11.60%

The total equity portion is 61.2%, so this is a 60/40 fund that’s drifted a little higher as equity markets have performed well. That’s normal.

A target date fund can help you eliminate decisions about allocating and balancing.

These can be a useful way to invest, but they’re not perfect. In a future column, we’ll discuss some potential pitfalls of target date funds, relative to a do-it-yourself portfolio.

Along those lines, if you prefer a more hands-on approach, many online brokers provide tools and research to help you choose the right asset allocation. In addition, robo-advisors such as Betterment and Wealthfront can allocate taxable and retirement accounts with ETFs,