How Much Upside Can Remain for a Market That's Afraid to Sell?

Headlines about the ongoing conflict between the U.S. and Iran are having a "magical" effect on the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Time and again the market has been trained to buy the dip. That has never been more true than during the Iran conflict.

Scary sounding headlines gradually pull stocks down which are quickly reversed. The “usual” behavior is elevator (fast) down, followed by stairs (grind) higher. The opposite has been the case lately, with last week’s performance bordering on “magical” (and certainly, at least somewhat, mechanical).

The news over the weekend did not seem good, but stocks refuse to go down by much.

Even if There Is a Peace Deal, How Much Upside Is Left?

Last week’s rally not only “solved” the Iran conflict (that isn’t solved), but it “solved” the AI/software fears.

(IGV) , a software ETF, rose 14% on the week. (ARKK) , which I use as a “proxy” for disruption, also rallied by 15%.

(INTC) (one of the few individual tickers I’ve been vocal about, in reports and the media, and which was my top pick for both 2025 and 2026 on TheStreet Pro.com and remains my largest single stock, as opposed to an ETF holding) said “hold my beer” as it rallied 35% in less than two weeks.

I will be trimming my INTC position up here.

(QTUM) (a quantum computing ETF) was up 25% and didn’t sell off as much in the first place — which makes some sense as investment into this area is only increasing.

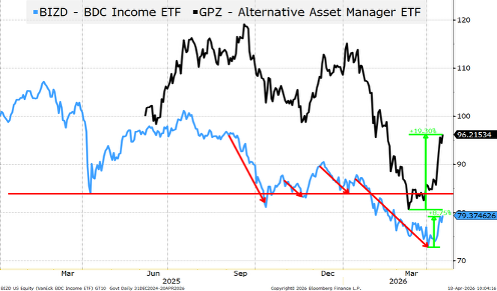

Private Credit Shows Optimism

Private credit also decided to “pretend” like everything was solved, though it has been solid for the past couple of weeks.

We use (BIZD) to reflect BDCs more broadly. It has risen “only” 9% since April 1 and, despite the rally, is still below its post Liberation Day lows.

(GPZ) (which has seen assets under management pop from just over $100 million when we first mentioned it, to over $250 million, predominantly through inflows) is an ETF that I use to track the performance of “alternative asset managers,” which includes companies with heavy exposure to private credit. It hit the low back on March 12, and is up almost 20% since then.

(OWL) which has arguably been at the epicenter of the private Credit discussion, rose 20% in just a week as it put its low in just last Friday.

I own some (PGZ) and BIZD (am debating selling more or adding, depending on how markets trade early this week).

What's Next for the Market

Rare earths, critical minerals and uranium stocks all rebounded. I think that should continue as the administration regains focus.

With 10-year treasury yields at 4.25% I think they should go lower, but this is more or less the “midpoint” of my current range on 10s.

The market should get back to pricing in at least one rate cut this year, so the front end of the bond market can do better as well.

I cannot help but watch this price action on Monday morning, relative to the news flow, and think that this rally is running out of steam, as too much good has been priced in too quickly.

Related: China’s Surprise Growth Shows Silence on Iran, U.S. Trade Can Be Golden

At the time of publication, Tchir was long BIZD, PGZ, INTC and GPZ.