Here's Why I'm Bullish, and Why I Think We Should Cut Rates

Let's look back at the week that was, what's ahead, the market chart, and a word on ... October.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Treasury markets appeared to sell off a bit last week. That said, the longer end of the curve remains stuck in a range for about half a year now and is trading toward the high end (low end for yields) of that range. The AI trade seemed a bit tired, as the major equity indexes experienced a "down" week, even if the AI trade did not seem that tired and the down week was down small.

What happened? The U.S. economy crawled out its hole and gave us a taste of its potential. That's what. Second-quarter gross domestic product growth was revised much higher from 3.3% to 3.8% (q/q, SAAR) and not just because of the impact from a drop in imports either. From the first estimate made by the Bureau of Economic Analysis in late July, to the final estimate last week, second-quarter GDP growth moved from an even 3% to 3.8% as personal consumption expenditures moved from growth of 1.4% to 2.5%, signaling a much stronger U.S. consumer than most economists had even dreamed of.

Even better, final sales to domestic purchasers improved over the two revisions from an initial 1.2% print to 2.9%. That number, gang, is organic economic activity. This strips out the impacts of exports and imports and measures exactly what it says it measures. Simply put, economic activity is not dying on the vine. Even for Q1 2025, when headline GDP printed at -0.6% (q/q, SAAR), this line printed at +1.9%. Is that strong? No. Is that the picture of an economy rolling off of a table? Not even close.

On top of that, both the New York and Atlanta Fed's revised their estimates for Q3 GDP growth significantly higher last week. It had been just a week earlier that economic activity had appeared to be stumbling forward, and economists were talking about things like "stagflation." You won't hear such silliness this week. Not after August new home sales, August durable goods orders, and August core capital goods orders all shocked to the upside. Not after August personal income and August personal spending both beat expectations.

August was, very quietly, a very strong month for the U.S. economy. The second quarter, was quite covertly, a better than solid quarter for the U.S. economy. Remember, what's good is bad and what's bad is good for financial markets over the short-term when markets are pricing in a dovish Fed posture concerning forward-looking monetary policy. Those aggressively dovish expectations faded, at least what is visibly being priced in by futures markets trading in Chicago, last week. That's what last week was really all about. Despite the pleadings of Michelle Bowman and Stephen Miran. I am not saying that they are wrong. I am just saying that there is less urgency to cut rates when the economy appears to be stronger than any of us had thought it was.

The Next Step?

There are three items that stand out for investors as we attempt to traverse the week ahead. First and foremost will be avoiding a government shutdown. Second will be the slope of the Treasury debt yield curve and third will be this Friday's September labor market report. Of course, should the U.S. government shutdown as September fades into the annals of history, that also means that the various non-essential government agencies will have to delay the release of their economic data.

The cold hard truth is that a kid carrying an M-16 for a living while digging holes in the ground is an essential government worker, an economist going back and forth between a calculator and an abacus while using badly outdated and grotesquely inaccurate formulas most certainly is not. A total of 900,000 (or so) government employees are facing potential furlough this week. Historically, equity markets yawn at the start of government shutdowns, but there will likely be some reaction in both dollar valuations and across Treasury markets.

It is important to remember that this is political. There will be a budget. I don't know when, but at least there is no debt limit involved this time around. The "Big, Beautiful Bill" took the debt ceiling up above $41 trillion. The current U.S. federal debt currently stands a little north of $37.5 trillion or slightly less than 124% of GDP.

My Thoughts

Honestly, though I know that there will be some bumps in the road, I am becoming more and more bullish as I travel this long and winding road. I know: Labor markets have been cooling off. They may continue to do so. That said, as witnessed over the past two weeks, these markets are stable. Job creation has slowed, but there is no broad gutting out of the national demand for labor going on at this time.

For U.S. financial markets, over the longer term, I will take a stronger economy over a more aggressively dovish Fed anytime. This recent economic strength, investors, traders and economists need to understand is ahead of the still coming impacts of deregulation across many industries including financial services and also ahead of the coming impacts of a number of tax cuts.

We are talking about larger standard deductions, increased child tax credits, additional senior deductions, no or less taxes on tips and overtime, new auto loan interest deductions and greatly increased state and local tax deductions. That's off the top of my head. I probably missed something. On the business side, more generous deductions for depreciation and amortization have been restored as have full bonus depreciation for new equipment and machinery.

Ladies and gentlemen... I may not be correct. Sometimes I am not. Most times I am, though I am never sure. That said, I am of the opinion that this economy may be standing at the precipice of something that could be described as an experience in explosive economic growth. Let's repeat those last three words... "explosive economic growth." Won't that wake up inflation? It might. Then again, there is the coming awakening of artificial intelligence. Not just large language models and chat-bots. I speak of generative and agentic artificial intelligence. I speak of inference development. I speak of autonomous robots and vehicles. Then, eventually, the advent of quantum computing.

These coming technologies, again in my opinion, will produce an unprecedented bust in labor productivity. This will have a powerful disinflationary, perhaps even deflationary, impact on the economy as a whole. It won't all be gummy bears and candy canes. Ultimately, there is a doomsday horizon for U.S. and global labor markets. As these technologies progress toward what will become known as an actual industrial revolution, some new jobs will be created. Many old jobs will go the way of the blacksmith. That's inevitable. It's not going to happen today or next month, but it's coming and each and every one of us will once again have to adapt.

Should We Cut Rates?

Simply put, yes. A thousand times, yes. Sarge, you just told us that the economy is strong and maybe getting stronger. I sure did. The slope of the yield curve is warped right now and has been for a long time. It's as simple as that. If short-term rates are artificial and long-term rates are the product of free-market price discovery, and there are inversions throughout the curve, then either short-term or long-term rates are incorrect.

Where is the neutral rate? Not here. Who is incorrect? Not the free-market, cowboy. I'll tell you that. If short-term rates are incorrectly priced through artificial means, long-term rates will have to react in order for the slope (shape) of the curve to correct itself. In a healthy economy, there are no inversions. Every single maturity should yield at least slightly more than the immediately subordinate maturity.

Correcting the curve, while potentially unfriendly to mortgage seekers, is more conducive to economic growth than what we have now and allows for proper risk assessment across credit markets by borrowers and lenders alike. What do we have right now? We have a 30-day T-Bill that is inverted against everything through the Seven-Year Note. Same for the 9)-day T-Bill. This sound right to you? Actually, from the Three-Year Note through the 30-Year Long Bond, there are no inversions. Hence, we know the error is at the short end of said curve.

The Target range for the Fed Funds Rate stands at 4% to 4.25%. Thirty-day U.S. paper pays 4.124%. Seven-Year U.S. paper pays 3.925%. It doesn't take a genius, gang. The Fed Funds Rate has to be taken below 3.5% and that's being conservative. It probably needs to be closer to 3% and it probably needed to be there the better part of a year ago.

Red October

Should we discuss October? I've been through a few of those. Many of you are too young to remember what can happen in October. The rest of you remember all too well. We'll discuss October in a couple of days. Let's see if anything gets done in D.C.

The Week That Was...

What the mid-major to major U.S. equity indexes did last week, as for both the S&P 500 and Nasdaq Composite, matching three-week winning streaks came to an end. That said, the Nasdaq Composite is likely to mark a six-month winning streak this Tuesday, while the S&P 500 makes it five up months in a row....

- The S&P 500 gained 0.59% on Friday but lost 0.31% for the week.

- The Nasdaq Composite gained 0.44% on Friday but gave back 0.65% for the week.

- The Nasdaq 100 also added 0.44% on Friday, surrendering 0.5% for the week.

- The Russell 2000 rallied 0.97% on Friday but still lost 0.59% for the week.

- The S&P Smallcap 600 popped for 1.08% on Friday but gave up 0.64% for the week.

- The S&P Midcap 400 ran 1.02% on Friday, still giving up 0.5% for the week.

- The Dow Transports gained 0.42% on Friday and 0.77% for the week.

- The Philly Semis added 0.32% on Friday and 1.17% for the week.

- The KBW Bank Index gained 0.74% on Friday but lost 0.31% for the week.

There were winners and losers last week, but Friday's rally was quite broad. On Friday, all eleven S&P sector SPDR ETFs closed out the session in the green, led by the Utilities (XLU) followed by the Discretionaries (XLY) and the Materials (XLB) . The Staples (XLP) brought up the rear but still managed to close up on the day.

For the week, just five of the eleven S&P sector SPDR ETFs traded higher. Energy (XLE) easily led the winners, gaining 4.81% over the five day period, followed again by the Utilities. The Materials and Staples closed the week down more than a full percentage point from where they closed a week earlier.

Note To Readers...

Ladies and gentlemen, your very best pal, and all-time favorite markets pundit / trader / investor / economist / college ice hockey player / U.S. Marine / infantry guy / certified jungle expert / certified small arms master gunner and all-round great guy will end his self-imposed exile from cable television this afternoon. I will appear on The Claman Countdown (3 p.m. ET) on Fox Business later today starring the one and only Liz Claman. She's the "awesomest." I expect to steal your hearts and minds later during the show.

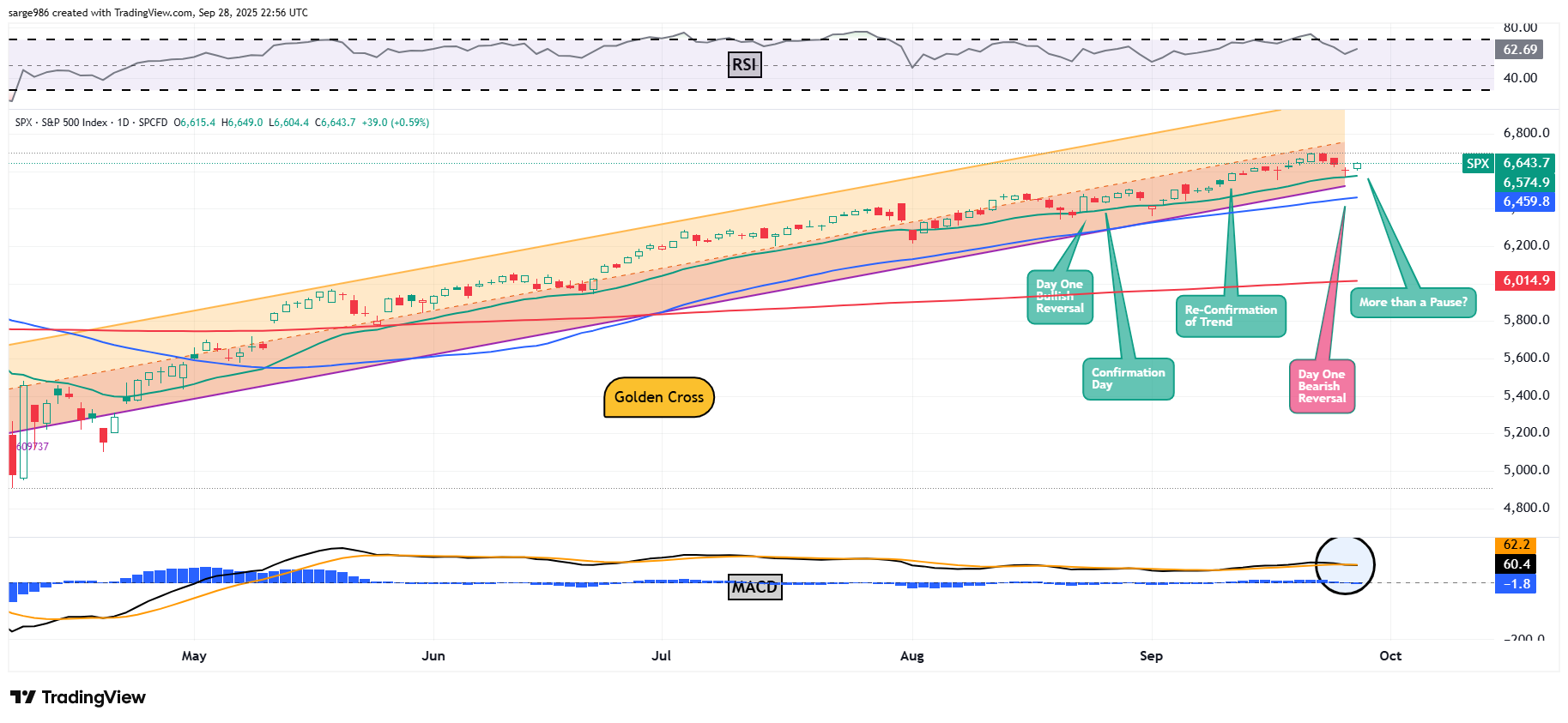

The Chart...

On Friday, I pointed out the possibility that the S&P 500 had potentially just suffered a Day One bearish reversal of trend. As always, I cautioned investors that a pause is necessary between any Day One reversal and any Day of Confirmation for said reversal. Yes, I know that Thursday was the third day of a three day selloff, but it was the first day that breadth and trading volume both went along with that sell-off. Hence, technically, Thursday was the "Day One" of that potential reversal.

Now, what to make of Friday. No, Friday was not a Day One bullish reversal. While the rally was quite broad and quite robust, it was not supported by increased trading volume. Not even close. Trade on a day over day basis was 13.1% lighter across NYSE-listed names and down 14.8% across Nasdaq-listings. But the rally on Friday still took out the Thursday high and the close on Wednesday. Does that price discovery on Friday negate the Day One bearish reversal last week? It really might. What's difficult to discern is what impact the possibility of a government shutdown this week and the labor market data expected this Friday are having on financial markets. I hate to do this to you, but we're in limbo in a way until we see some new activity and how developing news impacts the flow of capital.

Earnings

We are now little more than two weeks away from the start of the earnings reporting season for the third quarter. According to FactSet, for the third quarter, the street is looking for earnings growth of 7.9%, up from 7.7% a week ago. Wall Street also expects to see revenue growth of 6.3%, flat from last week. Technology, and utilities are expected to be the outperformers with projected earning growth of 17% or more. Three sectors are predicted to suffer a year over year earnings contraction led by Energy. For the full calendar year of 2025, Wall Street still sees S&P 500 earnings growth at 10.8% (up from 10.7%) on revenue growth of 6.1%.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 22.5-times 12 months' forward-looking earnings, down from 22.6-times a week ago. This stands well above the five-year average of 19.9-times for the index as well as its ten-year average of 18.6-times. The S&P 500 also ended last week trading at 28.3-times trailing 12 months' earnings, flat from the week prior. That also stands well above the five-year (25 times) and ten-year (22.7 times) averages for the index. Nine of the 11 sectors are now trading above their five-year average valuations, led by Tech (30 times) and Consumer Discretionaries (29 times). Only the REITs (17.7 times), and Health Care (16.2 times) remain undervalued relative to their five-year averages.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the third quarter up to growth of 3.9% (q/q, SAAR) from 3.3% the week prior. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth now stands at 2.55%, up sharply from 2.1%. The Cleveland Fed's model for the third quarter has been revised up to growth of 1.99% from 1.94%. I guess there is actually somebody home at the Cleveland Fed. They revise this model so rarely that I sometimes wonder. The St. Louis Fed model now stands at a paltry 0.22%, but that is up from last week's 0.05%. There remains nothing close to a Fed consensus.

Fed Funds Futures

Fed Funds futures trading in Chicago are now pricing in an 89% probability for a quarter-percentage point rate cut on Oct. 29 and just a 65% likelihood for another quarter-point cut on Dec. 10. While still in the affirmative, those probabilities are down significantly from a week ago due to the suddenly stronger economic data that hit the tape over the past week. At present, there is only a half point worth of additional rate cuts fully priced in (67% chance) for all of calendar 2026. There is now just a 37% probability for a third quarter-point cut at any point in 2026.

On The Docket...

The Fed will be out in force early this week and then do something of a disappearing act as the jobs numbers approach. There will, however, be a break from past norms as we have two speakers set to say something on Friday. Most unusual. Not speaking on "Jobs Day" has long been their SOP. This week will be all about avoiding a government shutdown, watching the bond market and what the Bureau of Labor Statistics published this Friday.

.... The Fed comes flying out of the gate this week. Today alone, I see at least five public appearances on the docket, headlined by Fed Gov. Christopher Waller who will speak before the opening bell. There are currently only five appearances on my radar over the balance of the week, including a Friday morning speech by NY Fed John "Lightning" Williams and a Friday afternoon appearance by Fed Vice Chair Philip Jefferson.

.... As far as the macroeconomic calendar is concerned, this is Jobs Week. August JOLTs data on job openings and job quits will cross the tape on Tuesday followed by the ADP Employment Report on private sector job creation for September on Wednesday morning. Thursday brings us the weekly prints for initial and continuing claims for state-level unemployment benefits. Then Friday is the day of the week. The BLS will post the results from their two beleaguered labor market situation surveys that morning. Then, many of us will spend the rest of the morning tearing those numbers apart.

..... The earnings calendar is unbelievably light this week. Among better known firms that will report are Carnival Corp (CCL) and Jefferies (JEF) today, followed by Paychex (PAYX) and Nike (NKE) on Tuesday. Finally, Acuity (AYI) , Conagra (CAG) and RPM International (RPM) will report on Wednesday morning. That's really all I have for you, gang.

.... Let's go Mets. Boooooo....

Economics

(All Times Eastern)

10:00 - Pending Home Sales (Aug): Expecting 0.2% m/m, Last -0.4% m/m.

10:30 - Dallas Fed Manufacturing Index (Sep): Expecting -7, Last -1.8.

The Fed (All Times Eastern)

07:30 - Speaker: Reserve Board Gov. Christopher Waller.

08:00 - Speaker: Cleveland Fed Pres. Beth Hammack.

1:30 p.m. - Speaker: St. Louis Fed Pres. Alberto Musalem.

1:30 - Speaker: New York Fed Pres. John Williams.

6:00 - Speaker: Atlanta Fed Pres. Raphael Bostic.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (CCL) (1.32)

After the Close: JEF (.86)

At the time of publication, Guilfoyle had no position in any security mentioned.