Hassett's 'Shadow' Appointment Brings Fed Put Back to Full Force

We can all sleep a little easier following the market's reaction to news that Kevin Hassett would get the nod as the next Federal Reserve chair.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The performance for almost every asset class was impressive from November 21 until November 28:

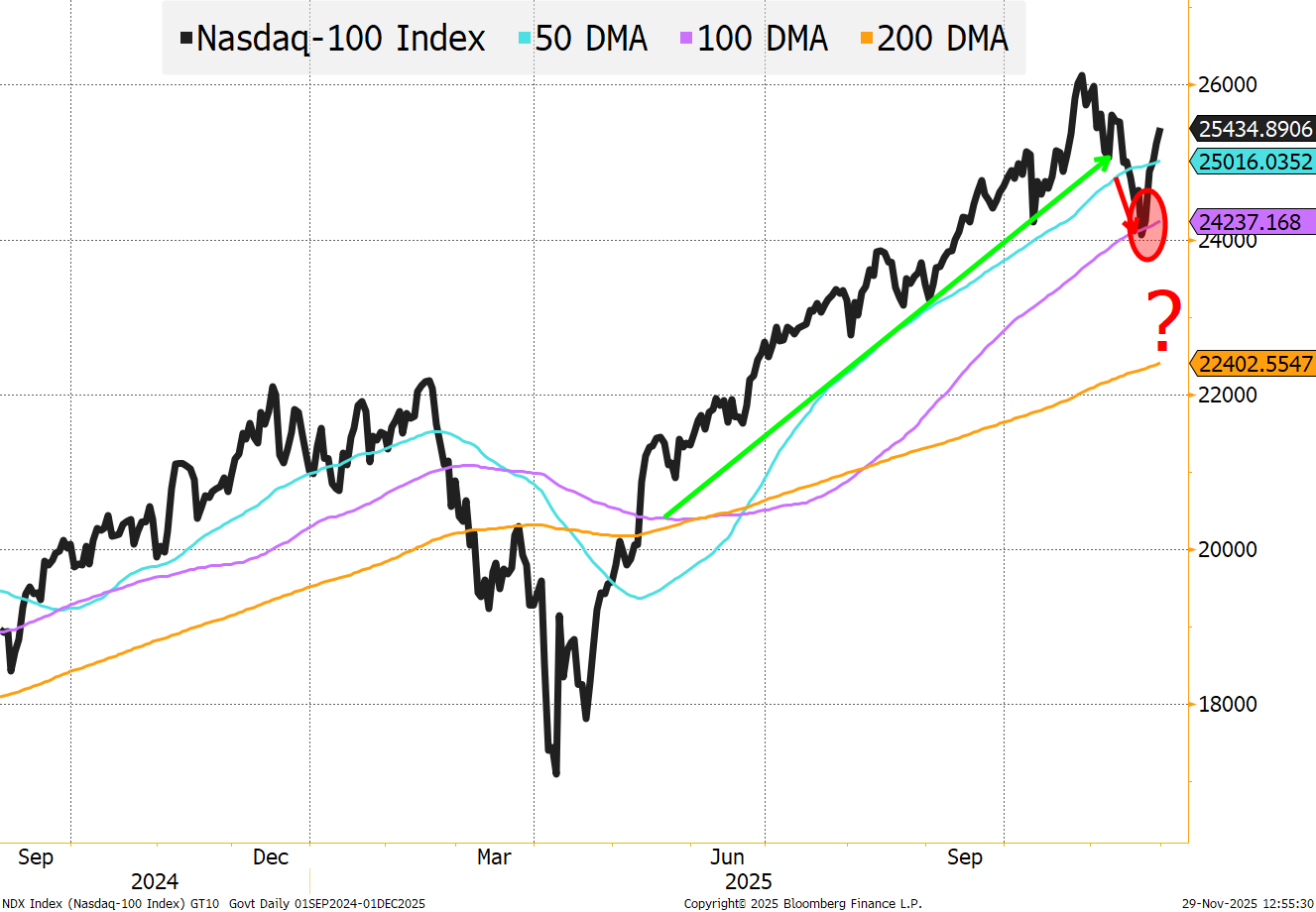

- The Nasdaq 100 is up 5.7% (outpacing the “rotation” trade of the S&P 500 equal weight, which is up 3% in those same trading days).

- The probability of a Federal Reserve rate cut at the December meeting spiked to 83% from 35% (which is well within the range where the Fed would be unlikely to disappoint). Ten-year treasuries rallied as well, though “only” from 4.07% to 4.02%.

- Bitcoin, which traded below $82,000 on the November 21, reclaimed the $90,000 threshold over the weekend.

- Credit spreads did well, too.

There were a couple of other “events” during the week that created some interesting movements (at least briefly). First — and possibly most interesting in the longer-term — was the sudden need to understand a TPU versus a GPU.

We were able to talk about this, the Fed and risks to the economy in the first segment of last week’s Bloomberg TV interview. The second segment focuses more on geopolitical issues.

The Fed Put Is in Full Force

You may not believe in Santa, or the Santa rally, but the Fed put might be the strongest it has been in some time.

The recognition that the Fed put is in full effect started last Friday, with New York Fed president John C. Williams coming across more dovish than most supposed he would in recent comments.

It continued over the weekend as more Fed speakers seemed to shift to the dovish side of the ledger.

Then, finally, it was reported that Kevin Hassett would get the nod to be the next Fed chair.

The market, correctly, interpreted this as a signal that the U.S Treasury, the Fed and the administration would work more closely together — helping pave the way for lower yields and easier monetary conditions.

There is also “chatter” that Hassett will act as a “shadow chair' at the December meeting, ensuring a cut.

I do think the tone in the Fed was driven by concerns about the equity market, hence my argument that this really is the Fed put rather than data dependent.

The Nasdaq 100 had not broken below its 50-Day moving average since the this past spring, and that seems to have triggered the sudden onslaught of dovish takes. The administration has continued to point to stocks as a benchmark (which is not truly unique to this administration, but this administration seems to have a better understanding of markets, and the machinations that can help markets, than prior administrations).

Chips for Everyone

While the questions surrounding TPUs versus GPUs were interesting, they did little for markets. Just like DeepSeek was quickly brushed off as some “one-off” type of thing, the market continues to see demand for high-end chips as “virtually” insatiable.

While some questions remain about the longer-term risk of selling chips to competitors (like China) or even some countries that we don’t fully align with (like some parts of the Middle East), we seem to be set to sell those high-quality chips to those countries.

This will:

- Substantially change the trade balance with many countries

- Allow for growth

- Highlight the competitive advantage that other countries have in electron production

The production of electricity is increasingly recognized as a potential roadblock to the planned growth of AI and data centers. Countries like Saudi Arabia and China are better prepared for this need for electricity than we are (once again, highlighting the need for "production for security"). China has been growing its electricity production through any and all means possible, including, but not limited to, coal, solar, nuclear and aggressive development work on fusion. We will likely have to do the same to compete.

Bottom Line

We can all sleep more comfortably and enjoy the holidays a little more with the Fed put on full display, but the risks to growth are real.

I do not like how “fickle” this market is. On Sunday night, a big drop in bitcoin seemed to drag risk assets lower — this was weird and concerning, as I could easily see bitcoin taking another leg down.

I’m kind of neutral here, watching for the Santa rally, but wary that spending and valuation concerns will take center stage again.

Hope you all had an amazing Thanksgiving!