Hands-Free Investing: Let the Pros Take Over

By outsourcing some financial decisions, you may even see a higher return.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This is the sixth of ten articles in the Filthy Rich Animal Investing Basics Series.

If you like what you see, are not yet subscribed, or would like to share with a friend, please visit this link to join us. It's free!

Starting soon, we'll shift over to providing actionable advice and weekly educational content.

Not Everybody Has the Time or Interest to Be an Investor. You can Still Be Successful.

Some people love diving into the details of investing. Analyzing balance sheets or studying stock charts might be your jam.

But what if it isn’t? What if you simply don’t have the time or interest to get into the weeds of portfolio construction?

In addition to work, family, hobbies and the undisputed priority of binge-watching “The Bear,” managing a portfolio can feel like one more overwhelming task.

But, thanks to technologies and a growing financial services industry, you can still be a successful investor without doing it all yourself.

Think of it this way: Most of the time, to get where you’re going, you’ll drive. But sometimes, it’s just easier to get an Uber. Similarly, outsourcing your investment management is a smart way to stay on track without stressing over every decision.

What Does Outsourcing Your Portfolio Look Like?

Don’t misunderstand: You can’t outsource all your financial decisions. You’re the one who has to understand your goals and ability to withstand portfolio risk. You’ve also got to commit to regularly putting money into your investment account.

But outsourcing some aspects of your financial life may have benefits you haven’t considered.

Here are some ways to take some investing tasks off your plate, while still remaining involved with your own financial decisions.

Financial Advisors

If you’ve built a substantial nest egg, hiring a financial advisor could be a great decision. Advisors create personalized investment plans, and perhaps more important, guidance on estate planning, tax strategies, charitable giving, cash flow management and retirement readiness.

Today’s advisors aren’t like your grandfather’s stock broker, though. Rather than spending all day picking stocks, the 21st-century advisor serves as a behavioral coach and expert resource on a range of money-related decisions.

Think of a good advisor as a "financial concierge" who can help give advice and access to products and services you wouldn't have even known to consider.

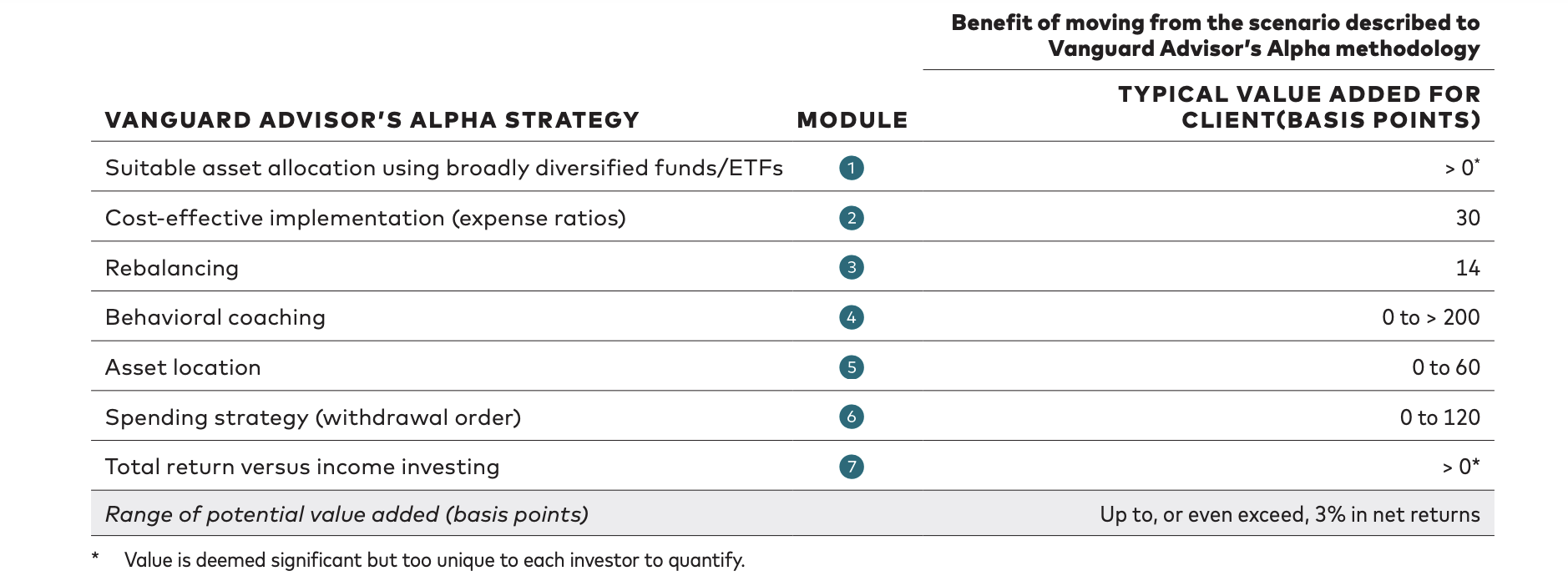

Vanguard's Advisor Alpha study quantified the value of working with a financial advisor. Many investors worry that an advisor’s fee will erode their returns. That’s a ridiculous assumption, as the industry wouldn’t exist at all if it made clients poorer!

Vanguard found that advisors can add about 3% in net returns annually for clients through strategies like cost-effective investment selection, tax efficiency, portfolio rebalancing and stopping clients from buying into market hype or panicking during downturns.

Robo Advisors

Robo-advisors use algorithms to allocate and rebalance your portfolio. Generally, robo-advisors use low-cost exchange-traded funds to diversify across various asset classes.

Companies like Betterment and Wealthfront pioneered the robo-advisor service, but now all the major brokerages, such as Schwab and Fidelity, offer robo services.

Using a robo-advisor might mean growth-focused strategies for younger investors, while retirees could use conservative allocations.

The biggest perk? Robo advisors are cost-effective. However, while you can call a robo-advisor and get a human on the phone for customer service or tech support, they can’t guide you through emotional challenges like fear and greed, or help you make investment decisions.

Hybrid Advisors

Looking for a middle ground?

Hybrid advisors blend the personal touch of human advisors with the efficiency of robo strategies.

For a modest fee, you get both a financial plan and automated portfolio management, making it a budget-friendly way to access professional guidance.

You can find this service at brokerages such as Betterment, Schwab, Fidelity, Vanguard and Personal Capital.

One-Fund Solutions

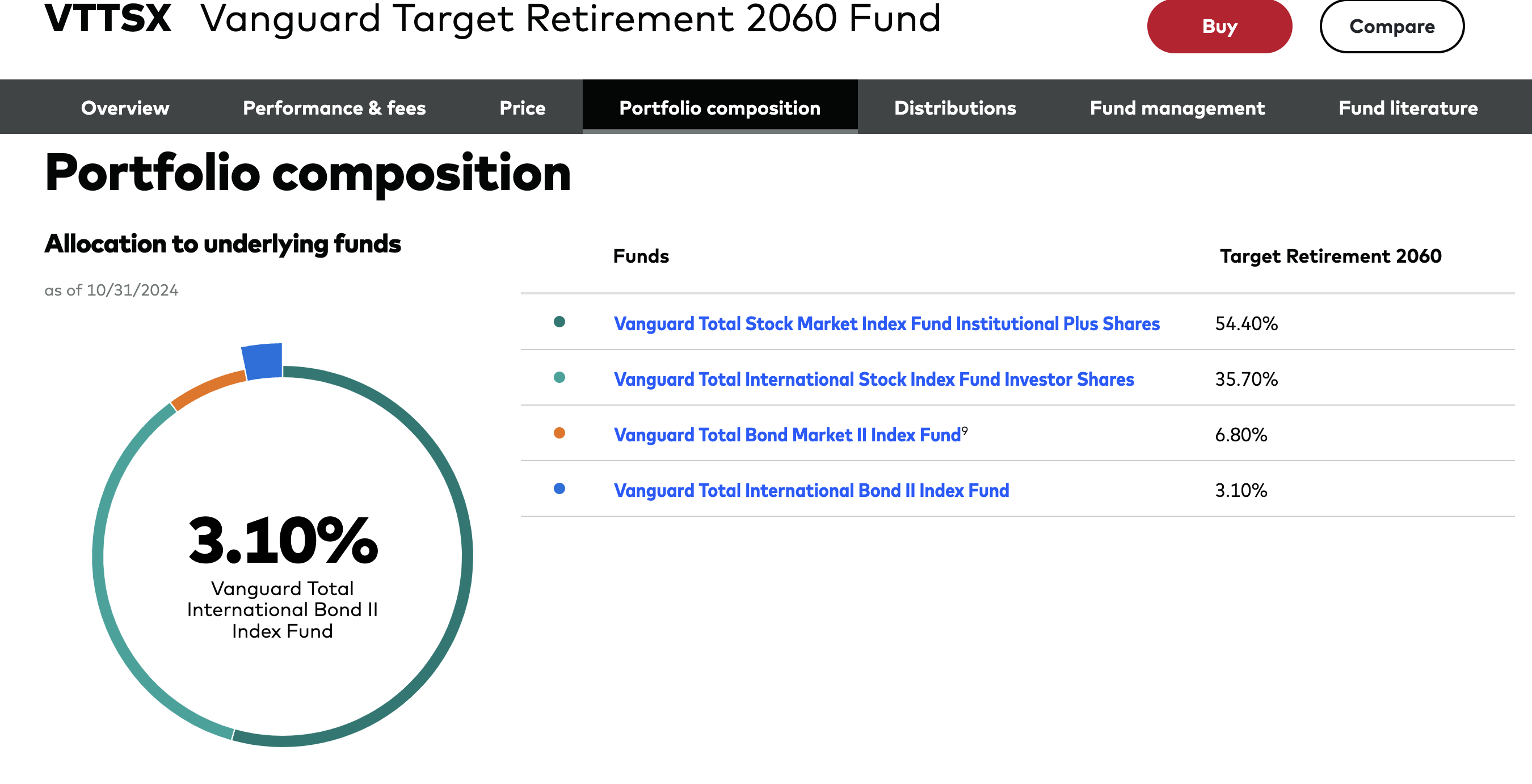

For ultimate simplicity, consider target-date or target-risk mutual funds. Target-date funds automatically adjust their allocation as you near retirement. That means more stocks when you’re younger, more bonds as you approach your goal.

For instance, Vanguard’s Target Retirement 2065 Fund is 90% stocks and 10% bonds, while the 2030 version is 63% stocks and 37% bonds.

These funds take the guesswork out of diversification, but you’ll still need to manage your emotional responses to market swings.

Investing Doesn’t Have to Be Tough

Whether you choose an advisor, a robo or a one-fund solution, outsourcing can substantially reduce your investing-induced stress levels.

Let someone else take the wheel while you focus on what matters most to you.

You can even use these strategies as the core of your portfolio and then make some opportunistic trades when the time is right.

Just like using Uber when it’s more convenient, it’s okay to let others handle your investments when it’s the smart choice. You can still grow your wealth without going it alone.