Greed Is Overlooking a Rare Opportunity in Risk-Off Assets

The last time there was such a significant disparity between stock and bond valuations was in the late stages of the dot-com euphoria. Don't discount these simple rules from Warren Buffett.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Five, or even ten years ago, if you had asked someone if they would accept 4.5% annually relatively risk-free (if held to expiration) for the next decade or longer, the response would have likely been skepticism. Such a deal would have sounded too good to be true. The knee-jerk rebuttal would have been: “Is this a Ponzi scheme?”

Ten years ago, and even five years ago at specific points, the focus was on the return of capital, rather than the return on capital. Accepting a nearly zero return for the safety of U.S. Treasuries was not only an acceptable “investment,” it was a popular and preferred investment! With the benefit of hindsight, we know following the mantra would have been a bad life decision.

In the current environment, the tables have turned to a stunning extreme. Ironically, investors are being presented with the reality of the aforementioned deal (4.5% return over a long period without undue concern over the outcome). Yet, they are shunning it due to the lack of return on capital.

To summarize, in 2020, everyone wanted to invest in these securities, which paid almost nothing at the time, but now they have little interest in investing in the same securities that pay ten-fold. You may notice some similarities between the 2020 peak in the 30-year bond and the current sentiment in the gold market. Five years ago, the long bond was a parabolic asset that provided no yield and exposed buyers to significant downside price risk. Today, the gold market is receiving favorable treatment.

Investors with fresh cash to put to work have a choice between stocks, bonds, real estate, gold, crypto, and a few other fringe assets. Of each of those asset classes, there is only one near a two-decade low in valuation: Treasuries. Furthermore, except for some forms of real estate, it is the only asset that yields an attractive income stream. Lastly, Treasuries are the least risky asset class in the world but the market is treating the securities as anything but.

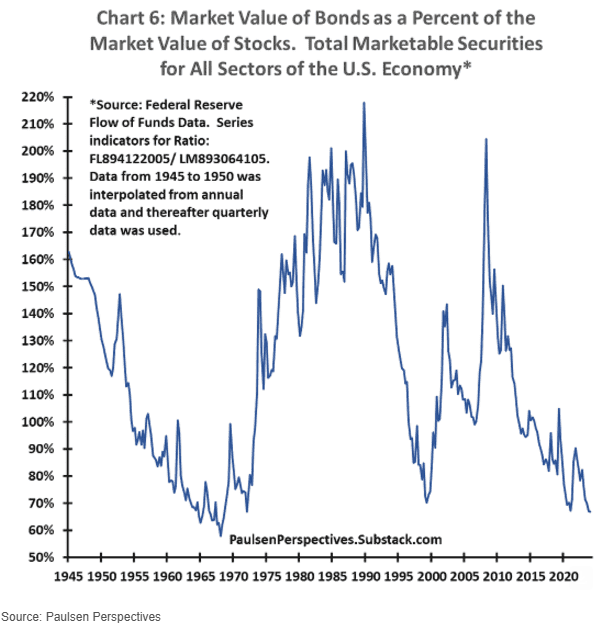

Investors have been opting for stocks, more specifically a handful of ticker symbols, but that isn’t guaranteed to continue indefinitely. Historically, there have been two other instances in history when stocks were as overvalued as they are now relative to bonds. Or, alternatively, bonds were this undervalued relative to stocks.

Regardless of how you view it, such opportunities have only arisen once every two decades, and they have proven to be significant inflection points in both stocks (the beginning of prolonged underperformance) and bonds (the start of a period of capital gains to enhance interest earned). This metric has been similarly favoring bonds since the initial collapse in 2023, so instant satisfaction shouldn’t be expected, but patience will likely pay off.

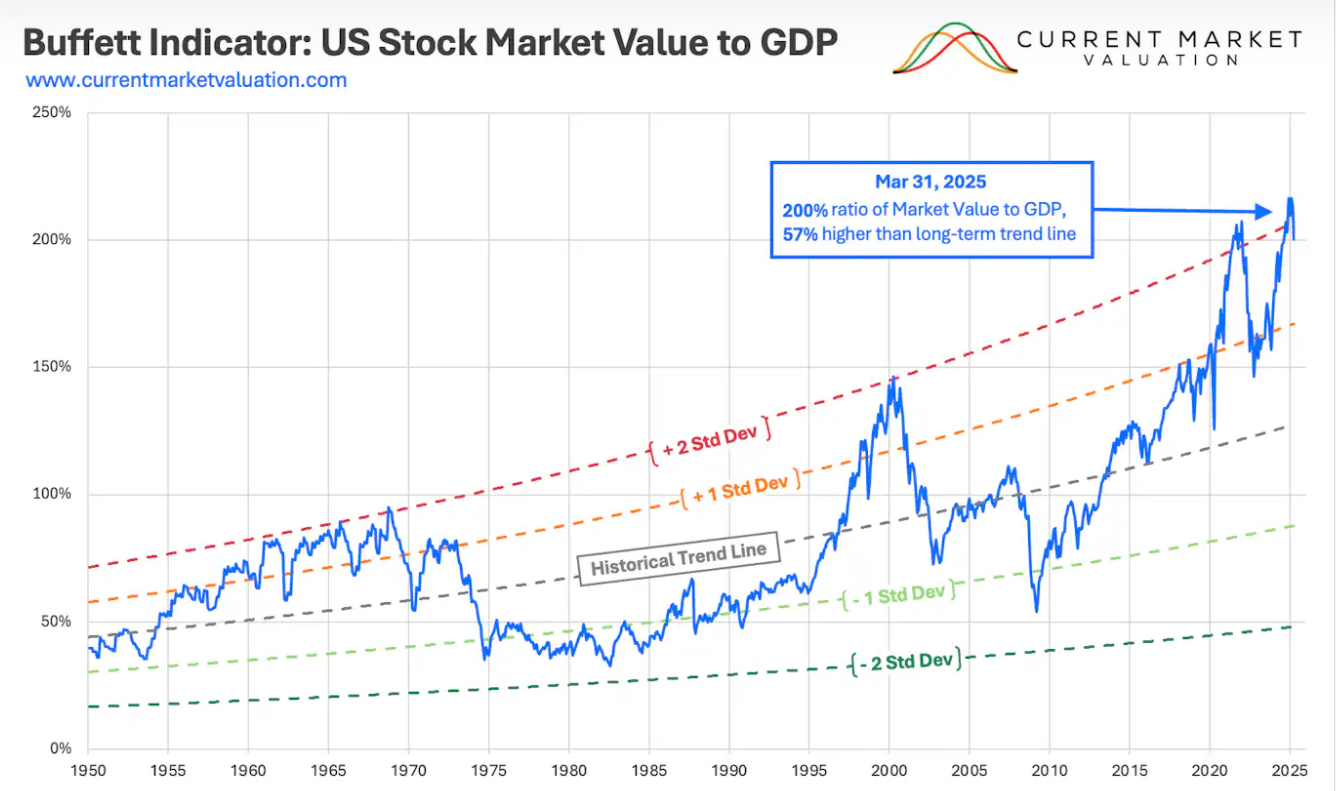

The Warren Buffett Indicator measures the total stock market value vs. the GDP. Since 1950, the stock market has only been this overstretched a few other times. Not surprisingly, the dot-com bubble was one of those times. Historically, this indicator has not been the time to hit the gas on risk assets. It has been the opposite.

Not coincidentally, the last time we saw such a significant disparity between stock and bond valuations was in the late stages of the dot-com euphoria, when investors flocked to high-flying tech stocks, leaving safety assets in the dust. Sound familiar? I’ll never forget the friends, family, and acquaintances who amassed unfathomable net worths in the late-90s only to give it all back. Like today, the real money back then was made with concentration, but it was the lack of diversification that eventually caught up to them.

While it is true that the S&P 500 has consistently increased over time, it is also true that there are periods of five to ten years during which the return is either zero or negative. For example, if you bought the hype in 2000, at the end of 2008, you would have yielded an annualized return of -1.4%. If you had bought the exact high at 1,527 in 2000, by March 2009, when the low was under 800, you would have been down nearly 50% from the peak nearly a decade prior. Further, those concentrated in a handful of stocks rather than a broad-based index likely suffered complete wipeouts. When everything is going well, we must remind ourselves that stock market wealth is just a number on a screen unless we keep it.

While younger market participants who are convinced that Warren Buffett is washed up count their riches, they are discounting a few simple rules the GOAT has left for us:

1. Be fearful when others are greedy and greedy when others are fearful.

2. Never bet against America (in this cycle, that likely means being overweight Treasuries and underweight momentum stocks).

Final Thoughts on Risk

To be clear, if the U.S. defaults on its debt obligations, holders of Treasury securities will bear the brunt of the consequences. However, unless the world is coming to an end, this is a low-probability event.

A more likely scenario would be a government or Federal Reserve program in which the government creates money out of thin air to purchase its own bonds. We’ve done this in the past; it is a cheat code that has been habitually abused. I am not saying this is the best solution, I am saying this is what would happen as opposed to bondholders taking a massive haircut. Then again, anything is possible, so the risk of a black swan event should be acknowledged.

Even so, unruly spending and budgets are a worldwide issue, not a domestic one. Thus, if you opt to invest elsewhere, the reality is that you are accepting a smaller reward for a similar or greater risk.

Finally, if interest rates continue to rise, it will create a paper loss for Treasury holders; yet, if held to expiration, investors are paid back in full, plus coupon payments, regardless of the fluctuations that occur between purchase and expiration.

Turning the conversation back to stocks, despite what has occurred over the last five years, stockholders are not guaranteed immediate gratification; that is why they are called “risk assets.”

Since 1928, the S&P 500 has returned an average annual rate of 10%; however, in recent years, the average return has been abnormally high, at approximately 14%. There is a good chance that, like the dot-com era, we have pulled forward gains and could be on the verge of a “returnless” market in the coming years.

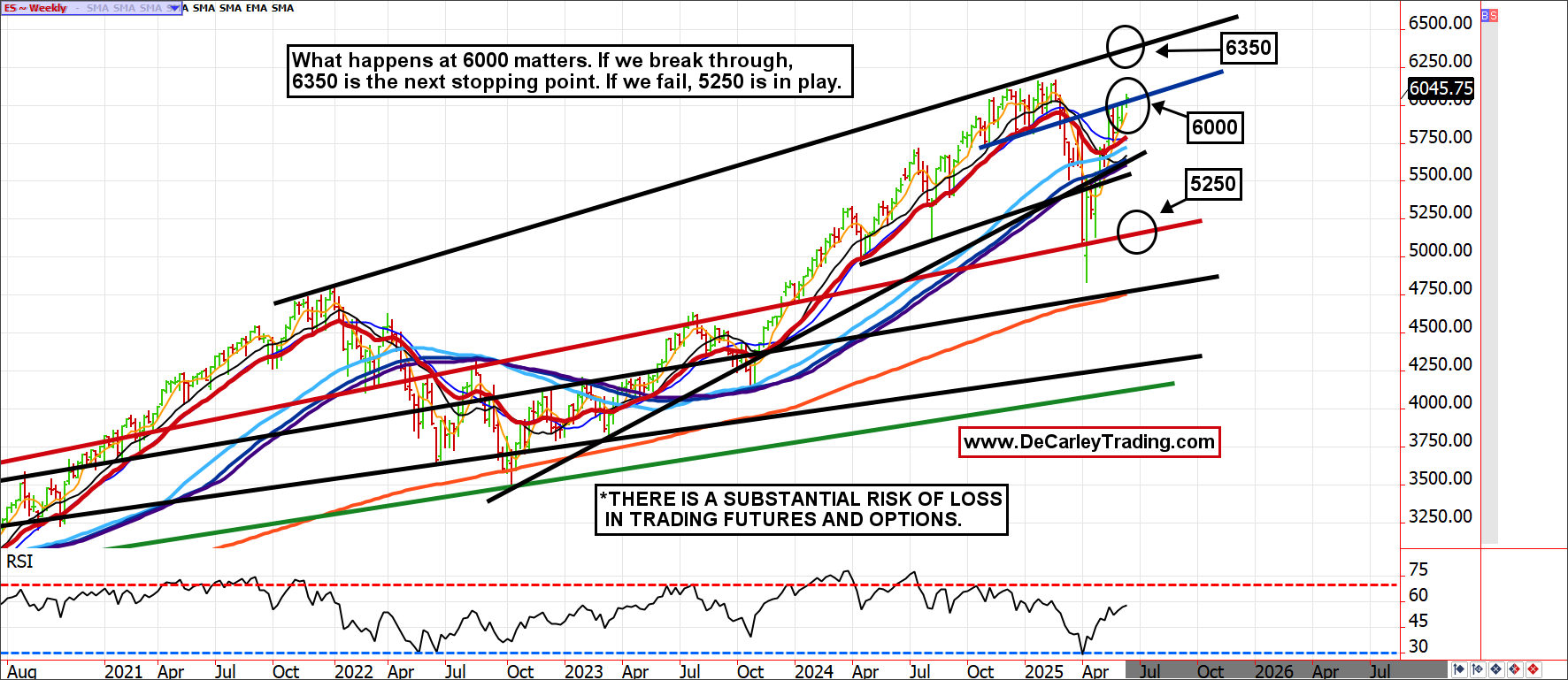

While I believe the S&P 500 can easily reach 6300 to 6400, the downside risk might be outsized relative to the potential reward. Focus on how much you can lose, not how much you can make. Don’t be afraid to venture into less popular markets, such as Treasuries, or execute hedges using the options on futures markets to protect a portfolio, such as risk reversals.

Investing is a mental game; putting yourself in a position to play offense when things are on sale prevents catastrophic panicked liquidation. Imagine what it might have felt like to liquidate equity holdings on the April 2025 lows. Now, imagine what it might have felt like to have the dry powder ready to buy equities into the April lows.

I spoke about this on the Cow Guy Close with Scott Shellady this week. Click here to view the clip.