Gold and Oil Have Followed Very Different Paths. But Here's What Could Be Next.

Unlike black gold, which has broken down in light of recent events, the yellow gold market has taken off to the upside. But parabolic gold should scare the bulls as much as the bears.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

While the crude oil market has fallen into obscurity, the gold market is shining brightly. Ironically, both could be in the process of reversals, but things could get even wilder from here. This is particularly true of crude oil, which has only experienced moderate volatility thus far relative to other big trend reversals.

Oil Is on a Slippery Slope

The oil market recently fell below $65.00, a price point that has found dip buyers for years. In our view, OPEC production cuts artificially supported the oil market, but with the oil cartel opting to stop doing the heavy lifting to keep prices afloat, we will see what the true fundamentals are. We suspect this is a very well-supplied market at a time when demand is questionable.

We had been noting that the oil market was giving us 2014 and 2020 vibes, and that view appears to be correct, but we won’t know for sure for another week or two. In both 2014 and 2020, the market traded for years in a low-volatility range with reliable trendline support levels bought into by speculators until that support failed and dramatically lower pricing ensued.

The recent break below $65.00 marked a technical failure at a trendline that dates back to the 2016 commodity bear market. The only other time we saw prices penetrate this support level was in 2020, and we all know how that ended. In 2014, a similarly stable trendline broke, leading to an oil collapse from about $100 to $30! We aren’t suggesting oil goes negative again, but we would caution against buying dips with naked risk.

The monthly chart reveals three distinct trading support levels spanning the last 25 years. The original started in 2004, holding prices above $40.00 (except the financial crisis), but by the time it failed to hold, oil (and the trendline) was much higher (around $90.00). We call this the “pre-fracking” era. Fracking allowed the market to take a stop down into the next trading range, which we call “post-fracking.”

Finally, this month’s penetration of the uptrend line that contained prices for a decade (except the pandemic fallout) leaves us wondering where the new trendline will be. If we have, in fact, taken a step lower into a lower for longer trading range, $65.00 will be the resistance, but support is yet to be determined. We suspect it might be near $50.00/$45.00.

Unless the market finds a reason to go back into a bull market, we expect prices to trade between $65.00 and $45.00 for now. It is relatively rare for significant trend changes in oil to occur in calm markets. Despite what it might feel like, this month’s volatility is child’s play relative to what we have seen (and felt, ouch) in the past. Thus, we encourage low or limited risk plays in either direction.

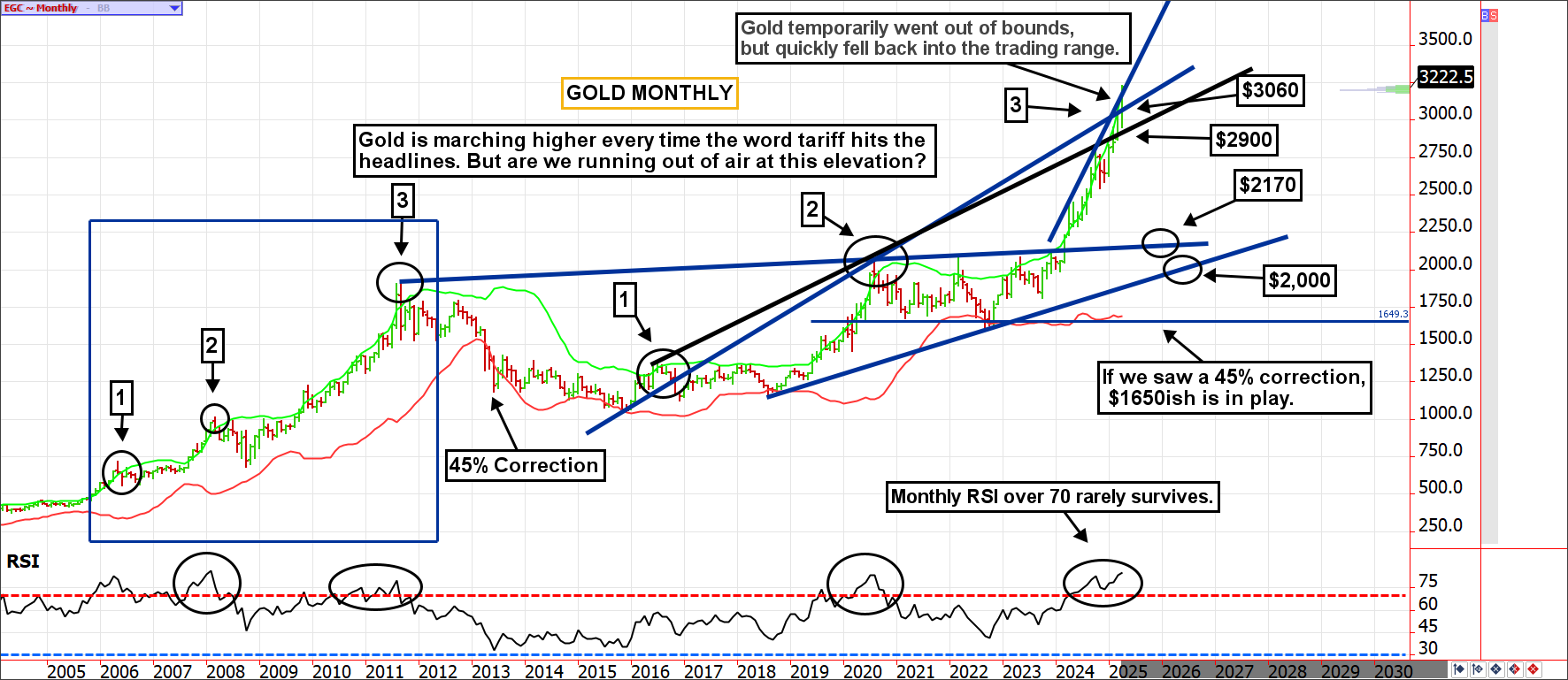

Parabolic Gold Should Scare the Bulls as Much as It Does the Bears

Unlike oil, which has broken down in light of recent events, the gold market has taken off to the upside. Despite the $250+ rally in recent sessions, the initial reaction to the stock market selloff was selling in gold, but those who liquidated want back in, and the rest of the world appears to have FOMO.

A few things are happening. First, retail is piling into ETFs and futures. The lack of stability in the bond market has encouraged safe-haven buying to choose gold. In my opinion, they are vastly underestimating their risk, but I’ve been wrong on this view thus far. We will see what happens.

Second, capital is leaving the U.S. dollar and looking for a place to go. In other words, foreign investors were buying dollars to buy U.S. stocks and bonds, and now they are unwinding that position. Gold is a beneficiary; the lower dollar pushes gold higher, but some prefer holding gold to fiat currency in this environment.

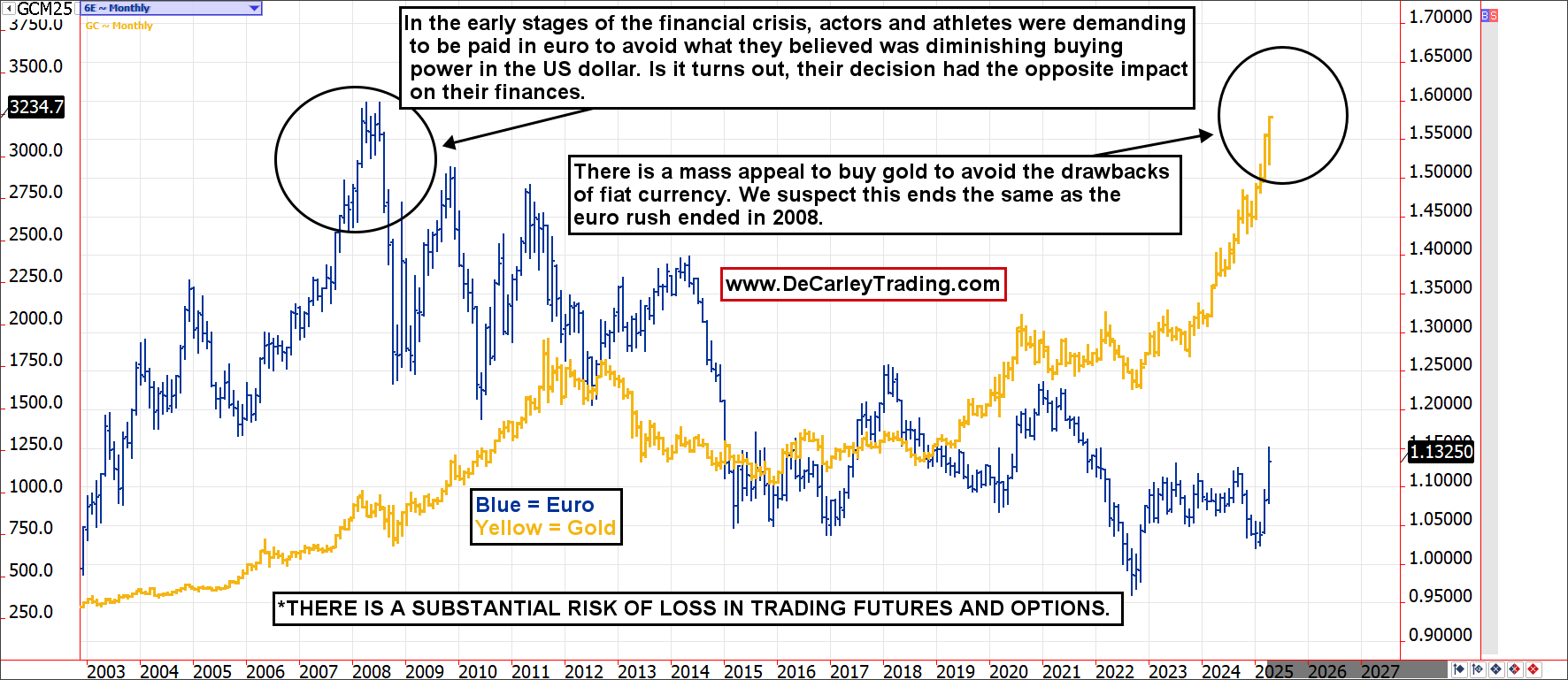

Notably, the world appears to have become dollar-averse. I recall a similar narrative taking the markets by storm in the early stages of the financial crisis. U.S. dollars were so out of favor that investors flocked to the euro to avoid what they believed to be a reduction in their buying power over time. Sounds familiar? The opinion was so overwhelming that pro athletes demanded to be paid in euros rather than the greenback! This is how that group-thinking eventually ended.

Additionally, there is a gamma squeeze in the gold market. Market volatility, particularly in metals, has caused options to explode in value. So, dealers, traders, etc., who are short-call options are forced to buy futures to hedge their risk, a process that feeds on itself. Lastly, margin calls are rampant, taking some time to work itself out. Most buyers at these levels are either FOMO or reluctant buyers (those who have to, not those who want to).

I’ll be the first to admit we turned bearish gold too early, but I wouldn’t advise my worst enemy to buy up here. The metals are a safe haven until they aren’t. This is what the 30-year seasonal chart looks like. Try to stay safe out there!