Giving Tuesday

'Sarge stocks' like Rocket Lab, SoFi, and Quantum Computing were on a roll Tuesday; also, let's check the market, the charts of Nasdaq and the S&P and the Stargate Project.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

You've Got Another Thing Coming

One life, I'm gonna live it up

I'm taking flight, I said I'll never get enough.

Stand tall, I'm young and kinda proud

I'm on top as long as the music's loud.

If you think I'll sit around as the world goes by

You're thinking like a fool 'cause it's a case of do or die.

Out there is a fortune waitin' to be had

If you think I'll let it go, you're mad

You've got another thing comin'.

- Downing, Tipton, Halford (Judas Priest), 1982

Oh ... Tuesday!?!

Hard to remember for sure. I am not really sure if Tuesday was the best day of my career in terms of one-day profit/loss performance, but it must have been close if it wasn't. I mean, I'm relatively sure that in dollar terms it must have been, and I've been doing this since I was 13 years old and professionally since I was 23. With large long-term long positions in Rocket Lab USA RKLB, and SoFi Technologies SOFI that were up 30.3% and 8.5% respectively and trade-sized long positions in Quantum Computing QUBT, up 16.9% as well as D-Wave Quantum QBTS, up 19.4%, not much was required of the rest of my book.

That said, my defense contractors all pitched in as well, after in some cases, having had tough 2024s. Kratos Defense & Security KTOS, Northrop Grumman NOC, RTX RTX, Lockheed Martin LMT, General Dynamics GD, and Palantir Technologies PLTR ran 4.8%, 4.6%, 3.9%, 3.3%, 1.9% and 1.8% in that order. A gift from Donald? Oh, I know that there will be give and take as tariff-related rumors and news start to push high-speed keyword-reading algorithms sound, but on Tuesday, with potential tariffs on Canada, Mexico, and China not making immediate news in the wake of the inauguration, but potentially being pushed out to Feb. 1, these algos were lined up as was I and so it was.

On That Note...

The new president made off the cuff remarks on Monday, the day of his inauguration, about imposing 25% tariffs on both Canada and Mexico, the two closest U.S. trading partners, instead of actually taking immediate action. He did instead, sign an executive order assigning both the Department of Commerce and the Department of Homeland Security to assess illegal migration and flows of illicit drugs, notably fentanyl, from these two nations as well as from China.

Does this mean that the president is trying to create room to negotiate some kind of agreement that would improve the trade environment for the U.S. without going as far on tariffs as feared by some? Wall Street appeared to latch on to that idea on Tuesday. In addition to the informal threats of 25% tariffs on Canadian and Mexican imports, on his second day (first full day) in office, President Trump spoke of placing a 10% tariff on Chinese imports and mentioned placing tariffs on imports from the European Union.

In all cases, the president seems to be targeting Feb. 1 as a big day of decision for what will come, at least for starters as far as international trade is concerned.

Markets

Tuesday was a day made for a huge rally. The U.S. Dollar Index showed some weakness, as the long end of the Treasury yield curve showed strength (sending yields lower). Gold, silver and Bitcoin all rallied on Tuesday after getting off to slow starts. Overnight, Bitcoin is off a little overnight, but as we cruise through the zero-dark hours, US equity index futures are warm yet again.

For the day on Tuesday, the S&P 500 gained 0.88% as the Nasdaq Composite gained 0.64%. More impressively, the small to midcap indexes all ran at least 1.6% for the session as the Dow Transports popped for 1.24% and the Philly Semiconductors climbed 1.29%.

Turning to the market internals, ten of the eleven S&P sector SPDR ETFs shaded into the green on Tuesday, with the defense sector-led industrials XLI gaining 2.05%. Among these 11, four other funds gained at least 1%, while only Energy XLE closed in the red. Interest rate sensitive defensives such as the REITs XLRE and the Utilities XLU were among the strong for the day.

On breadth, winners beat losers by a rough 5 to 3 at the NYSE and by about 7 to 4 at the Nasdaq. Advancing volume took a 57.1% share of composite NYSE-listed trade and a 67.3% share of Nasdaq-listed activity. Reinforcing our day of confirmation on Friday, aggregate trading volume popped for day over day growth of 1.9% and a truly impressive 12.9% across securities listed at the NYSE and Nasdaq respectively.

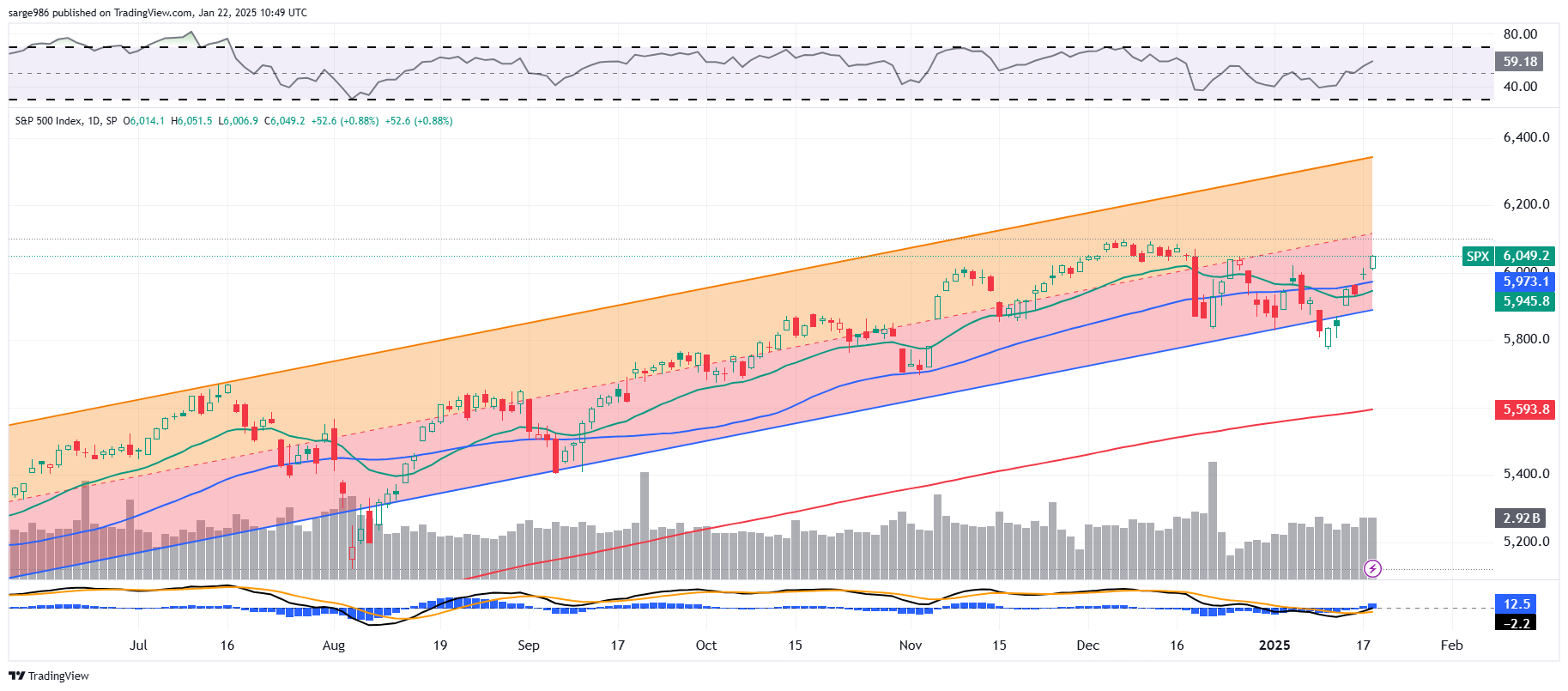

The Charts

Forget about the head-and-shoulders pattern that had been built from October into December. That pattern has been obscured as the S&P 500 has returned to trend, after surviving a little bit of a scare in early to mid-January. Let's zoom in a little:

Note that as trading volume has increased of late, that Relative Strength (above the chart) has improved and that within the daily Moving Average Convergence Divergence (below the chart), with the histogram of the 9-day exponential moving average noticeably above the zero-bound, the 12-day EMA appears to be breaking away from the 26-day EMA.

This, as the last sale for the index appears to be breaking away from its own 50-day SMA. The Nasdaq Composite is also showing signs of pulling away, though it cannot yet be said to have returned to trend.

Completely Off the Radar...

A big LOL goes out to the all but forgotten World Economic Forum shindig at Davos, Switzerland. Enjoy patting yourselves on the back.

Stargate

OpenAI CEO Sam Altman, Softbank CEO Masayoshi Son and Oracle ORCL Chair Larry Ellison stood with President Trump on Tuesday to announce the official launch of the Stargate Project, which will be a $500 billion, four-year initiative to build out the infrastructure that will be required for generative artificial intelligence to truly flourish. Arm Holdings ARM, Nvidia NVDA and Microsoft MSFT were also mentioned as key partners in this program.

The announcement states "The buildout is currently underway, starting in Texas, and we are evaluating potential sites across the country for more campuses as we finalize definitive agreements." OpenAI tweeted out (posted on X) "We will begin deploying $100B immediately. This infrastructure will secure American leadership in AI, create hundreds of thousands of American jobs, and generate economic benefit for the entire world."

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 7.09%.

07:00 - MBA Mortgage Applications (Weekly): Last 33.3% w/w.

08:55 - Redbook (Weekly): Last 4.0% y/y.

10:00 - CB Leading Indicators (Dec): Expecting 0.0% m/m, Last 0.3% m/m.

1:00 p.m. - Twenty Year Bond Auction: $13B.

4:30 - API Oil Inventories (Weekly): Last -2.6M.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ABT (1.34), CMA (1.26), GEV (2.37), HAL (.69), JNJ (2.05), PG (1.86)

After the Close: DFS (3.36)

At the time of publication, Guilfoyle was long RKLB, SOFI. QUBT, QBTS, KTOS, NOC, LMT, GD, RTX, PLTR, NVDA, MSFT equity.