Fuel to the Fire: Crude & Natural Gas Heat Up, Credit Worries Grow

Let's look at the big question marks hanging over the market as the war on Iran continues, private credit uncertainty and banking fragility fears extend, and the chart of the S&P ... growls.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Market_Recon_TSP1_KL

Market_Recon_TSP1_KL

Monday, Monday

Monday, Monday, can't trust that day

Monday, Monday, sometimes it just turns out that way

Oh Monday mornin'

You gave me no warnin' of what was to be

Oh Monday, Monday, how could you leave and not take me?

- John Phillips (The Mamas & The Papas (1966)

Trouble Behind...

Trouble ahead. Trouble behind. You know the rest of the song. First came fears of agentic AI having a negative impact upon a number of traditionally high paying industries, most notably software, but also the banking and legal fields. The reduced demand for white collar labor would ultimately tamp down consumer-level demand as well, making it more difficult to sell goods and services across the U.S. and eventually, global economies. Those fears, though realistic, in my opinion, have faded of late.

Why is that? We, the investing and trading public, have bigger fish to fry, or should I say simply, we have more immediate concerns. The war in the Middle East, or specifically, the ability of Iranian military forces to threaten and close the Strait of Hormuz, despite being unable to defend themselves, has driven prices for crude and natural gas through the roof. Front month WTI Crude futures traded above $101 per barrel on Sunday night and are still trading above $100 as I work through the zero-dark hours on Monday morning. This came after core personal consumption expenditure prices for January hit the tape on Friday, at their highest level since March 2024.

Then there have been the growing concerns over private credit and the potential frailty of the entire banking system. Those fears grew last week as JP Morgan (JPM) marked down a number of loans to private credit types and announced an intention to cut lending to those funds going forward. Morgan Stanley (MS) later in the week, limited redemptions at one of its private credit funds as other, similar funds at other institutions did the same.

The problem there is that none of us know quite what we are dealing with or how large aggregate industry exposure is. There is a real chance that Wall Street will decide that this threat has been overstated, if not in the news, then at least through the process of price discovery. Should Wall Street decide that this market has been oversold, and that there is no systemic risk present, despite some cracks in the private credit space, then risk assets to include equities and maybe even debt securities, will rally from here, even if energy commodity prices remain elevated for a time.

Trouble Ahead?

I wouldn't call it "trouble" per se. I think that there are a number of high-profile events set for the coming week that will impact the trajectory of asset prices that traders and investors will have to adjust to in real-time. As always, our ability to maintain our field of vision, identify both targets of opportunity and perceived threats as they enter the playing field and adapt to changed environments, will determine our level of success.

Of course, the unfolding private credit concern, as I do not want to refer to that as a crisis (For I do not want to be an alarmist, or intentionally sensationalist as are certain members of the financial media), will continue to drive algorithmic traffic. Of course, the ability of seaborne cargo to pass through the Strait of Hormuz will continue to move markets. We now expect that, and quite frankly, those forces could act as upside catalysts in the not-too-distant future.

They all said, there are two new "forces of nature" that could and probably will impact financial markets this week....

1) Nvidia's (NVDA) four-day GTC conference in San Diego kicks off later today with a keynote address to be made by CEO Jensen Huang. Agentic AI and the growing abilities of graphics processing units, as well as central processing units will be front and center. Microsoft (MSFT) , Meta Platforms (META) and Tesla (TSLA) are all expected to participate in the event. We would also like to hear something granular in regards to Nvidia's order backlog and learn anything more there is to learn on expected shipments into 2027.

2) Wednesday of this week is Fed Day. The Federal Open Market Committee's next two-day policy meeting will conclude on Wednesday afternoon with a 2 p.m. ET statement. More important than the statement, as futures markets trading in Chicago are now pricing in a 99% probability for no change to be made to short-term interest rates, will be two items.

Released along with that statement will be the FOMC's quarterly update to the group economic forecasts for both unemployment and inflation. A half hour later, Fed Chair Jerome Powell will hold his penultimate press conference at the helm of the nation's central bank. Those futures markets are not pricing in a rate cut until December, but Powell-s term as Chair is up on May 15, so we shall see about that.

Related: Looking for a Short-Term Rally, While Lowering the Panic Point for Nvidia

The Week That Was...

U.S. financial markets were pummeled yet again, last week. The S&P 500 has now posted three consecutive red-candle weeks and five losing weeks in six. The Nasdaq Composite has also posted three-straight losing weeks and eight losing weeks in nine. Yikes. Think small-caps have done better? Think again. The Russell 2000 has also posted three-straight red-candle weeks and has posted six losing weeks in eight. Last week...

- The S&P 500 gave up 0.61% on Friday and 1.6% for the week.

- The Nasdaq Composite lost 0.93% on Friday, and 1.26% for the week.

- The Nasdaq 100 gave back 0.62% on Friday and 1.06% for the week.

- The Russell 2000 surrendered 0.36% on Friday and a nasty 1.79% for the week.

- The S&P Small Cap 600 lost just 0.13% on Friday but a gnarly 2.25% for the week.

- The S&P Midcap 400 gave up just 0.2% on Friday, but an ugly 2.03% for the week.

- The Dow Transports gained 0.12% on Friday but was pasted for 3.95% for the week.

- The Philly Semis gained just 0.05% on Friday, but a more impressive 1.76% for the week.

- The KBW Bank Index lost 0.77% on Friday and a very nasty 4.17% for the week.

On Friday, six of the 11 S&P sector SPDR exchange-traded funds closed out the session in the red, led lower by the Materials (XLB) and Technology (XLK) . The defensives led the winners, and the defensives were left by the Utilities (XLU) .

For the week, nine of the 11 S&P sector SPDR exchange-traded funds traded lower. Financials (XLF) , discretionaries (XLY) and industrials (XLI) all taking a pounding in response to the downward revision to fourth-quarter gross domestic product. Energy (XLE) , not surprisingly, was the market's standout winner.

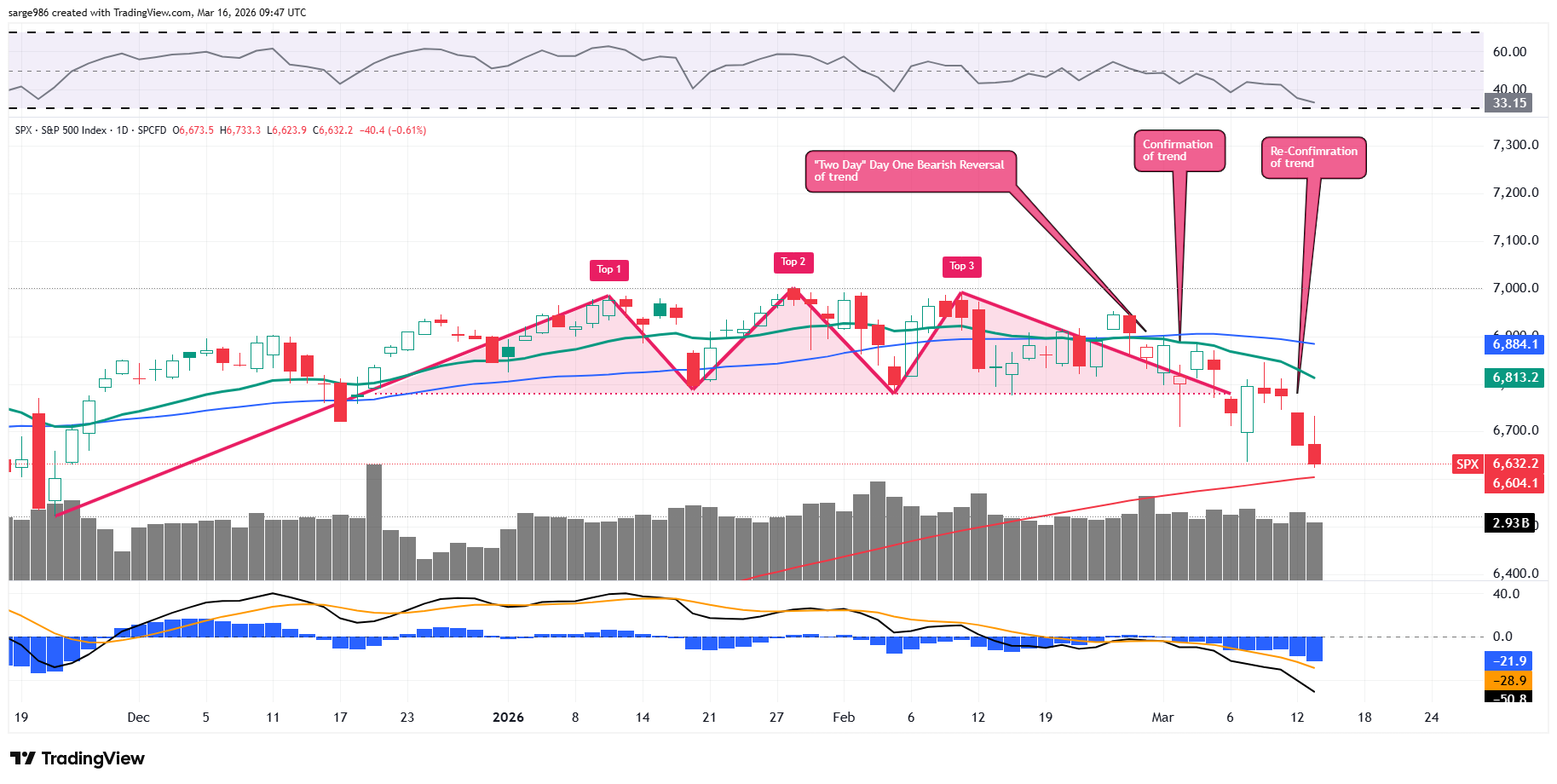

The Chart

Readers will see the triple-top pattern of bearish reversal that we adopted last week, replaced the basing period of consolidation that we had been focused on earlier. Readers will also see the reconfirmation of bearish trend on increased trading volume that appeared this past Thursday. On Friday, the S&P 500 tested its crucial 200-day simple moving average. (The Nasdaq Composite actually closed below its 200-day line on Friday afternoon.)

Should the broadest large cap U.S. equity index lose that key line in the sand, portfolio managers up and down Wall Street will be forced to reduce long-side exposure to the asset class. This could cause a technical rally early this week that either takes or does not ahead of some of the events discussed above.

Looking at the indicators, Relative Strength continues to weaken but is not quite yet at technically oversold levels. The daily moving average convergence divergence is in awful shape. All three components went out on Friday exhibiting an overtly bearish looking posture.

Quote of the Day

"No man deserves to be praised for his goodness, who has it not in his power to be wicked. Goodness without that power is generally nothing more than sloth, or an impotence of will."

- Francois de la Rochefoucauld (1613-1680)

Earnings

As of Feb. 12, according to FactSet, for the first quarter, Wall Street sees year-over-year earnings growth for the S&P 500 of 11.6%, up from 11.5% last week. Wall Street also sees revenue growth of 9.4%, up from 9.2% a week ago. For the full year 2026, the street looks for earnings growth of 15.3%, up from 14.7% two weeks ago, on revenue growth of 8.0%, up from 7.7% last week.

At the moment, the technology sector is projected to have grown earnings a stunning 41.7% for the first quarter with the materials in second place at growth of 24.6%. Three sectors, health care, energy and communication services are projected to have suffered a Q1 earnings contraction.

As we are currently in between seasons, the earnings calendar is not all that active this week. That said, there are several noteworthy firms reporting. Among well-known names expected to post quarterly results this week will be Dollar Tree (DLTR) , Lululemon Athletica (LULU) , Macy's (M) , Micron Technology (MU) , Signet Jewelers (SIG) and Federal Express (FDX) .

Economics

(All Times Eastern)

08:30 - Empire State Manufacturing Index (Mar): Expecting 3.9, Last 7.1.

09:15 - Industrial Production (Feb): Expecting 0.2% m/m, Last 0.7% m/m.

09:15 - Consumer Spending (Feb): Expecting 76.2%, Last 76.2%.

09:00 - NAHB Housing Market Index (Mar): Expecting 37, Last 36.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (DLTR) (2.53)

At the time of publication, Guilfoyle was long JPM, NVDA equity.