Feeling Like Michael Burry — Is the Market Finally Ready to Listen?

Early… or right? Here's my case for patience in a market where my bearish view has diverged from the herd.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"The Big Short" New York Premiere - Outside Arrivals

"The Big Short" New York Premiere - Outside Arrivals

In anticipation of a market correction/bear market I have substantially bolstered my cash position recently in order to take advantage of the possible developing long opportunities. Meanwhile, I am trading more aggressively from the short side than I have in a while.

A Story of Patience

Most people know that Michael Burry bet and profited against subprime in 2008. It became known as the Big Short (and a movie was even made out of his experience). But fewer people know what happened before the payoff.

For two years, Burry's Scion Capital was bleeding — as his trade/investment was under water. His Limited Partners threatened lawsuits. His founding backer, Joel Greenblatt, flew across the country to call him a liar. Burry was forced to "side-pocket" his subprime trades, locking up withdrawals in order to survive. He refused to let anyone leave even as the fund's losses mounted. His partners stopped speaking to him. Then the market broke.

Scion ultimately made about $725 million and his investors saw +489% total return. Burry was a genius, but six months earlier, he was nearly out of business. The lesson is the cost to hold. Being early and being wrong feel exactly the same; until they don't.

Most people don't survive the "until." (Ultimately Burry shut down his Fund because managing human emotion during the wait was too painful).

I have felt like Michael Burry over the last 18-20 months as our ursine market outlook did not match the market participants' enthusiasm and robust investment returns. The difference, of course, between my hedge fund Seabreeze Partners and Scion Capital is that while being negative in view, we have managed risk well (as for 25 of the last 26 months our Partnership has delivered a positive investment return).

My Negative Market View Remains Unchanged

Over the last two years I have made the case that the markets have materially underpriced risk — that there is a broad and growing list of possible market and economic outcomes that are market unfriendly. I continue to hold to this view. Fundamentally, our concerns continue to be justified:

* Geopolitical risks are multiplying. (The recent attack on Iran is illustrative of this concern as the most immutable rule of war is the law of unintended consequences.)

* A period of disappointing economic growth and persistent inflation lie ahead: As you all know by now I call this "slugflation." (Recent hot inflation coupled with the rise in crude oil are supportive of this view.)

* I remain skeptical about the circular financing of massive AI projects as well as the likelihood of generating adequate returns on that capital investment. (The Mag 7 and peripheral companies represent a large portion of the S&P Index.)

* The private equity and debt markets are deteriorating. (See my Surprise List where I highlighted the risk in Apollo (APO) , KKR (KKR) , Blackstone (BX) and the others.)

* Consensus forecasts for 2026-7 S&P profits are likely too optimistic.

* Neither political party seems to have any fiscal discipline — as measured by our country's growing deficit and ever-expanding debt load.

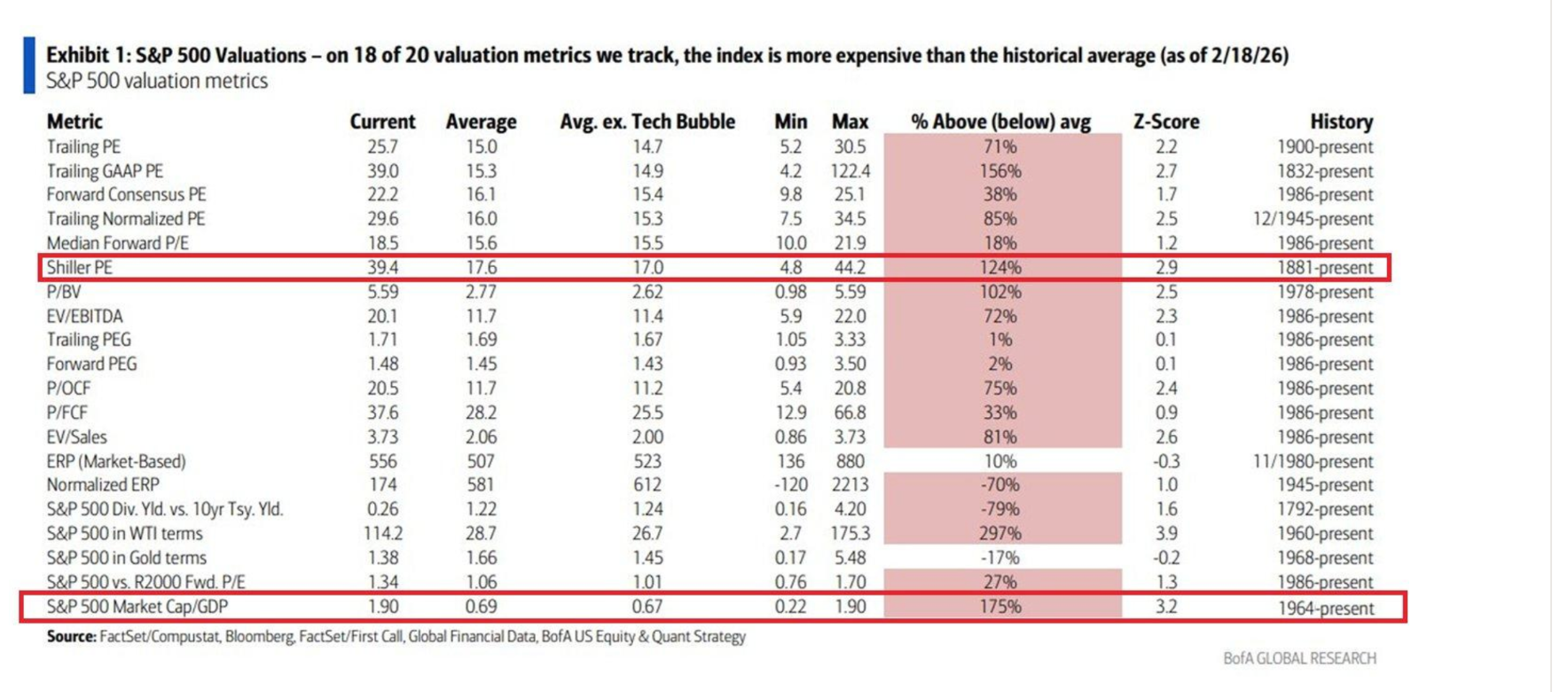

* The equity risk premium has become, for the first time in almost three decades, an equity risk discount. Historically, this is an indicator that current valuations provide a poor launching pad for future returns. It also means that investors believe there is more risk in owning bonds than stocks — truly a foolish (and dangerous) notion. From a valuation standpoint stocks remain somewhere between highly overvalued and pornographically overvalued. Most traditional valuation metrics support this view:

Bottom Line

I continue to expect at least a small double-digit decline in the S&P Index this year.

Based on recent events and price action, the correction of the multi-year bull market may come sooner than later.

Related: As War Rages on in Iran, Oil Itself Takes Back Burner to These Concerns

Note: This article was a summary of recent commentary to my Seabreeze Partners (hedge fund) investors and other observations made in my Daily Diary on TheStreet Pro.

At the time of publication, Kass was long SPY common (s/m), QQQ common (s/m); short SPY calls (s/m), QQQ calls (s/m).