Fed's Friday Flip and Tightrope Walk Ahead

The road ahead will not be easy for the Fed, and it may not be easy for investors, especially as we enter September trading.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Fed Chair Jerome Powell's speech from Jackson Hole, Wyoming has come and gone. The leader of the U.S. central bank used the opportunity, which was very likely his last annual keynote address from that location, to signal a coming shift in monetary policy. Powell tried to be vague and tried to just open the door to the possibility that the Fed would be reducing short-term rates, but that's not how markets took the signal.

When Powell flipped the probable trajectory for monetary policy here in the U.S. from moderately restrictive to something almost certainly less so, he also flipped financial markets. Yields across the curve, after a tough week, started moving lower. On top of that, a bevy of domestic equity indices flipped their weeks from negative to positive just on the one huge "green arrow day" created by Powell's comment heard around the world.

I quoted that comment in my post-speech piece here at TheStreet Pro on Friday morning, as "Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance."

As stated in that piece, Powell did make an effort to sound balanced. He did acknowledge that there is some renewed upside risk to consumer level inflation and as we have been made so rudely aware, by an inaccurate Bureau of Labor Statistics, some increased downside risk to employment.

Not Easy

The road ahead will not be easy for the Fed, and it may not be easy for investors. Tis the season for trouble, mind you. September has long been the worst month of the year for U.S. financial markets from a seasonal perspective. Additionally, October might not be the worst month of the year on average, but investors of a certain age have often experienced their very worst months in October. There's a reason that the old "Sell in May" crowd always redeployed their capital in time for November.

Powell himself referred to the place that the central bank now finds itself in, whether by its own hand or not, as a "challenging situation." Consumer-level inflation had neared the Fed's 2% target, bottoming out at 2.3% in April. The headline consumer price index has now printed at year-over-year growth of 2.7% for two months running. Both the Cleveland Fed and Hedgeye models have headline CPI running above 2.8% and below 2.85% for August.

The unemployment rate has not really gone anywhere of late. We'll hear new employment survey data for August a week from this Friday, but anything heard from the Bureau of Labor Statistics, as it has been for at least two years now, has to be treated as suspect, even with the removal of Erika McEntarfer from her leadership role at the Bureau. Though she oversaw the Bureau during an extremely sloppy couple of years, it will take more than merely a change in leadership to clean up that shop. All of the models used and the methods used for data collection very likely have to be reworked.

As things stand now, if current BLS data is correct, the unemployment rate has held firm at 4.2% for about a year, but job creation has dwindled down to just 93,000 in total for the three months covered by the May through July period. Underemployment has moved up to 7.9% in July from 7.5% this past December, while participation has dropped from 62.6% to 62.2% over that same time frame.

The central bank will almost certainly have to sacrifice focusing on one side of its dual mandate in order to prioritize the other. For several years now, since the federal government's "worse than reckless" fiscal policies coming out of the pandemic era, the Fed has prioritized their fight against inflation as employment had not been an issue. Powell's speech transitioned the Fed away from that fight to focus on slowing down a potential deterioration of labor market demand. Let's hope that "they" are not too late. Let's also hope that "they" do not somehow accidentally open Pandora's Box.

Ain't it a Hoot?

I find it incredible that all along, I had been calling for a large reduction (of a full percentage point or more) to be made by the FOMC to the target range of the Fed Funds Rate. I had been aggressive and somewhat sharp-tongued in my delivery. The hot producer price index print for July put me in my place a bit. I had to eat some humble pie. Did that July PPI heat make me uncomfortable? Of course it did. I think it has to.

I still believe that the Fed should be cutting rates, but I no longer believe it should be aggressive in doing so. The slope of the yield curve needs to be corrected and reducing short-term rates is the proper way to get there if one believes that prices at the long end of the curve are the result of free market price discovery.

That said, several of these economists that appear to be auditioning for the role of Fed Chair as Powell's term at the top ends in May, have been lining up and calling for rate cuts of a full percentage point or more. Former St. Louis Fed Pres. James Bullard is just the latest. I am on board with moving in the direction that Powell signaled on Friday.

Powell has made some significant mistakes. Real doozies, actually. On that we agree. The Fed funds Rate is too high. On that, I think we also agree, Given where we are in the here and now, unless next week's labor market report looks like something out of a cheap horror movie, I don't think Powell is in error to take a cautious approach toward easier monetary policy in this climate.

About That Flip...

What the major to mid-major U.S. equity indexes did last week markets, as the nation focused on Powell's Friday morning speech from Jackson Hole:

- The S&P 500 gained 1.52% on Friday to gain 0.27% for the week.

- The Nasdaq Composite gained 1.88% on Friday but still lost 0.58% for the week.

- The Nasdaq 100 gained 1.54% on Friday but still lost 0.9% for the week.

- The Russell 2000 soared 3.86% on Friday to gain 3.3% for the week.

- The S&P Smallcap 600 popped for 3.8% on Friday to gain 3.45% for the week.

- The S&P Midcap 400 ran 2.74% on Friday to gain 2.63% for the week.

- The Dow Transports gained 3.29% on Friday to add 2.8% for the week.

- The Philly Semis ran 2.7% on Friday to end up just 0.03% for the week.

- The KBW Bank Index gained 3.22% on Friday, closing up 3.51% for the week.

On Friday, ten of the 11 S&P sector SPDR ETFs closed out the session in the green, led higher by all five cyclical sectors. Discretionaries XLY and Energy XLE led the way. Defensive sectors took the bottom three slots on the daily performance tables. The Staples XLP manages to close unchanged for the day.

For the week, nine of the 11 S&P sector SPDR ETFs traded higher, led in a northerly direction by Energy, the REITs XLRE and the Materials XLB. The two growth sectors, Communication Services XLC and Technology XLK both closed in the red for the week.

Breadth

Now, Friday's run may have been aided by some short covering, so keep that in mind, but there was some technical change on Friday. Winners beat losers by better than 9 to 1 at the NYSE on Friday and by almost 5 to 1 at the Nasdaq. Advancing volume took a jaw-dropping 95.1% share of composite NYSE-listed trade for the regular session and a still commanding 85.3% share of composite Nasdaq-listed activity. Now, for the licker... aggregate trade was up a ridiculous 44% on a day over day basis across Nasdaq-listings and up a still somewhat ridiculous 25.7% across NYSE-listed securities. Is that meaningful? You bet your tail it is.

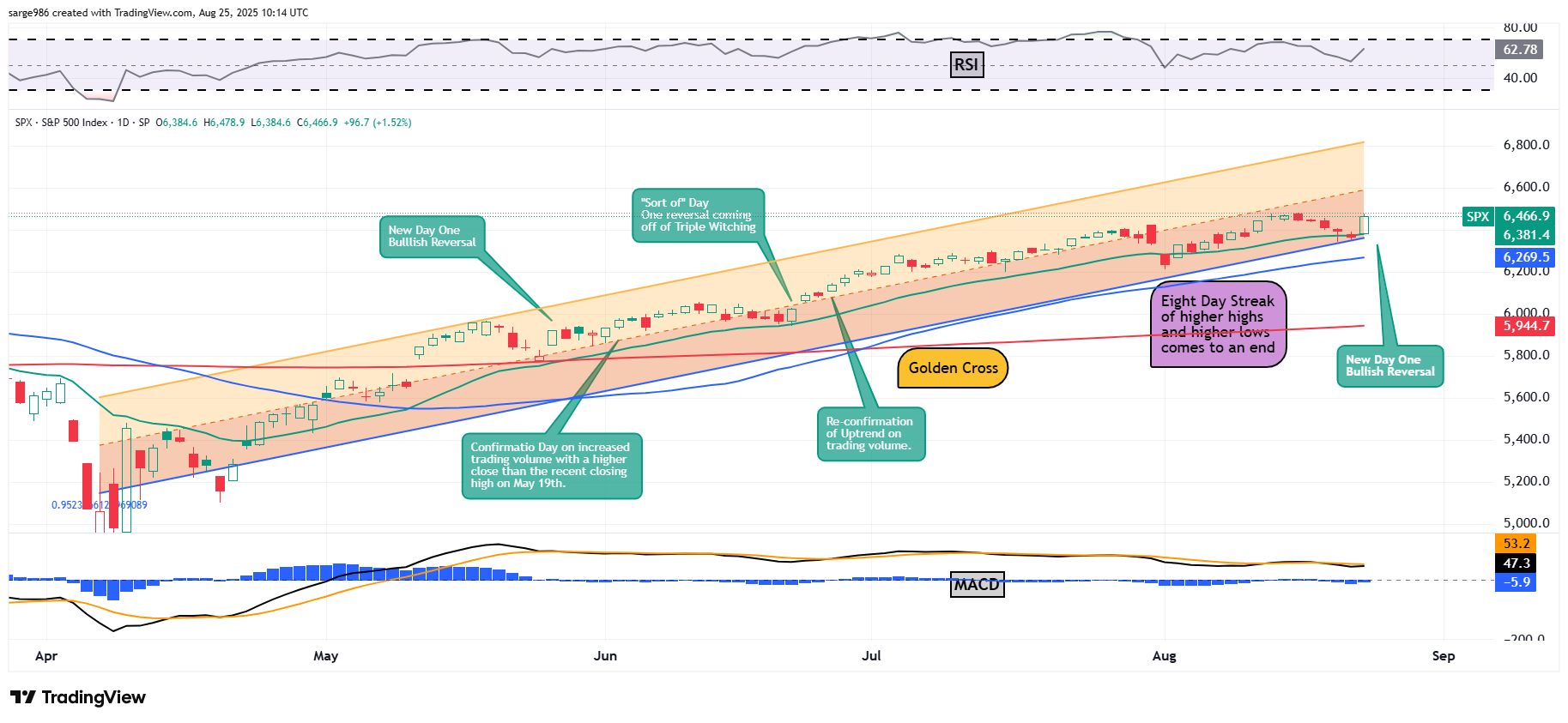

The Chart...

Now, readers need to understand that there could be some "give-back" or profit taking on Monday morning, especially if traders feel that the short-covering is over. That said, there is no denying that unified, sharp movement in a northerly direction on significantly increased trading volume. Friday, coming on the heels of five consecutive "down day's was not a reconfirmation of a bullish trend, but a new 'Day One" bullish reversal. Now, we need to see a pause and then a follow-up rally also on good volume. That would be a confirmation of Friday's move.

Readers will note that support for the S&P 500 has been found at the 21-day Exponential Moving Average, indicating good appetite (or short-covering) by the swing crowd. The 50-day Simple Moving Average was never tested, so neither were the "pros." Professionally managed money never went anywhere and largely remains invested.

Relative Strength, above the chart, has gained some momentum over the past week and is now once again, better than neutral. The daily Moving Average Convergence Divergence, below the chart, still paints a murky picture, but is looking better than it did. The histogram of the 9-day EMA is still in negative territory, though it has moved back toward the zero-bound. That could be short-term bearish, which could be helpful if the bulls need to see a pause.

The 12-day EMA is still below the 26-day EMA, which is not positive, but it has curled up toward that line which is. Additionally, both of those lines are in positive territory. Should the 12-day EMA cross above the 26-day EMA with both of those lines above zero, it will be "game on" for the bulls.

On The Docket...

On to the next catalyst, gang. As we gear up for the three-day Labor Day weekend, this becomes Nvidia NVDA week. There's plenty going on this week, but Nvidia earnings on Wednesday evening will be the sword by which the markets will live or die with this week.

......The domestic macroeconomic calendar will have a couple of very busy days this week. On Tuesday, July Durable Goods Orders will be followed up by Case-Shiller June home prices. After that, the Conference Board will release their survey for August Consumer Confidence. Then, we skip to Thursday. That day, the BEA will revise their estimate for Q2 GDP. On Friday, traders thinking of half-tailing it into the weekend had better think again. On Friday, PCE consumer prices for July will hit the tape alongside Personal Income and Personal Spending, both also for July. After that, the University of Michigan will revise its August survey results for Consumer Sentiment and Inflation Expectations.

..... The Fed will not be out in force this week. Heck, it's almost a three-day weekend, coming off of their weekend shindig in Jackson Hole and this crew is not exactly known for their kick-tail work ethic. That said, "Lightning" John Williams of the New York Fed will speak tonight and Fed Gov. Christopher Waller, who is still the betting man's favorite to replace Powell in May, will speak on Thursday evening.

..... There are not a lot of earnings releases this week. There are, however, a lot of firm's reporting that retail investors like to trade and that John and Jane Average have both heard of. On Tuesday evening, the juice starts flowing when MongoDB MDB and Okta OKTA both report. On Wednesday morning, we'll hear from Abercrombie and Fitch ANF and JM Smucker SJM ahead of the opening bell. Then we'll hear from CrowdStrike Holdings CRWD, Nvidia NVDA and Snowflake SNOW after the close.

Thursday will bring numbers posted by Best Buy BBY, Burlington Stores BURL and Dick's Sporting Goods (in the morning. That afternoon, Dell DELL, Marvell Technology MRVL, SentinelOne S and Ulta Beauty ULTA all will report as well.

Economics

(All Times Eastern)

10:00 - New Home Sales (Jul): Expecting 631K, Last 627K SAAR.

10:30 - Dallas Fed Manufacturing Index (Aug): Expecting 0.9, Last 0.2.

The Fed

(All Times Eastern)

3:15 - Speaker: Dallas Fed Pres. Lorie Logan.

7:15 - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights

(Consensus EPS Expectations)

After the Close: HEI (1.14)

At the time of publication, Guilfoyle was long CRWD, NVDA, S equity.