Drama at the Fed, Manic Monday, My Unease With U.S.' Intel Investment

Let's unpack the Trump plan to 'fire' Fed Gov. Lisa Cook, chart the S&P, and see why I'm a little skeptical over the INTC deal.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Fired? Maybe. I don't know. On Monday evening, Pres. Trump posted a letter to his Truth Social account that he had written to Fed Gov. Lisa Cook. After citing his authority to do so under both the Constitution of the United States and the Federal Reserve Act of 1913, the president informed Cook, who was appointed by former Pres. Joe Biden, that she has been removed (for cause) from her position at the central bank's Board of Governors effective immediately.

Pres. Trump writes in the letter that "there is sufficient reason to believe you may have made false statements on one or more mortgage agreements." Later on in the letter, the president writes, "In light of your deceitful and potentially criminal conduct in a financial matter, they (the American people) cannot, and I do not have such confidence in your integrity. At a minimum the conduct at issue exhibits the sort of gross negligence in financial transactions that calls into question your competence and trustworthiness as a financial regulator."

So, has Lisa Cook been fired from her position? That answer is way above my pay grade. The letter from the president came four days after the Department of Justice had informed Cook that it was investigating claims made by Federal Housing Finance Agency Director Bill Pulte. Pulte had made allegations that Cook had made false statements on mortgage applications in two locales that would land her lower interest rates on at least one of those mortgages than she should have received.

In response to those allegations, Cook had said that she would not resign and has retained well-known attorney Abbe Lowell to represent her. Yields and U.S. dollar valuations both moved lower on Monday evening in response to this news but have worked their way back up to approximately where they had been overnight.

Meanwhile...

French stocks have led European equities and U.S. equity index futures lower overnight as the possibility arose that Pres. Emmanuel Macron's government could collapse. French Prime Minister Francois Bayrou, who does not appear to have the votes, has said that he would seek parliamentary approval to move ahead with his austerity plans for the French fiscal policy on Sept. 8. Should this ultimately lead to a successful vote of confidence in the government, Macron could appoint a new prime minister or call for new parliamentary elections that would then likely take place in October.

Manic Monday

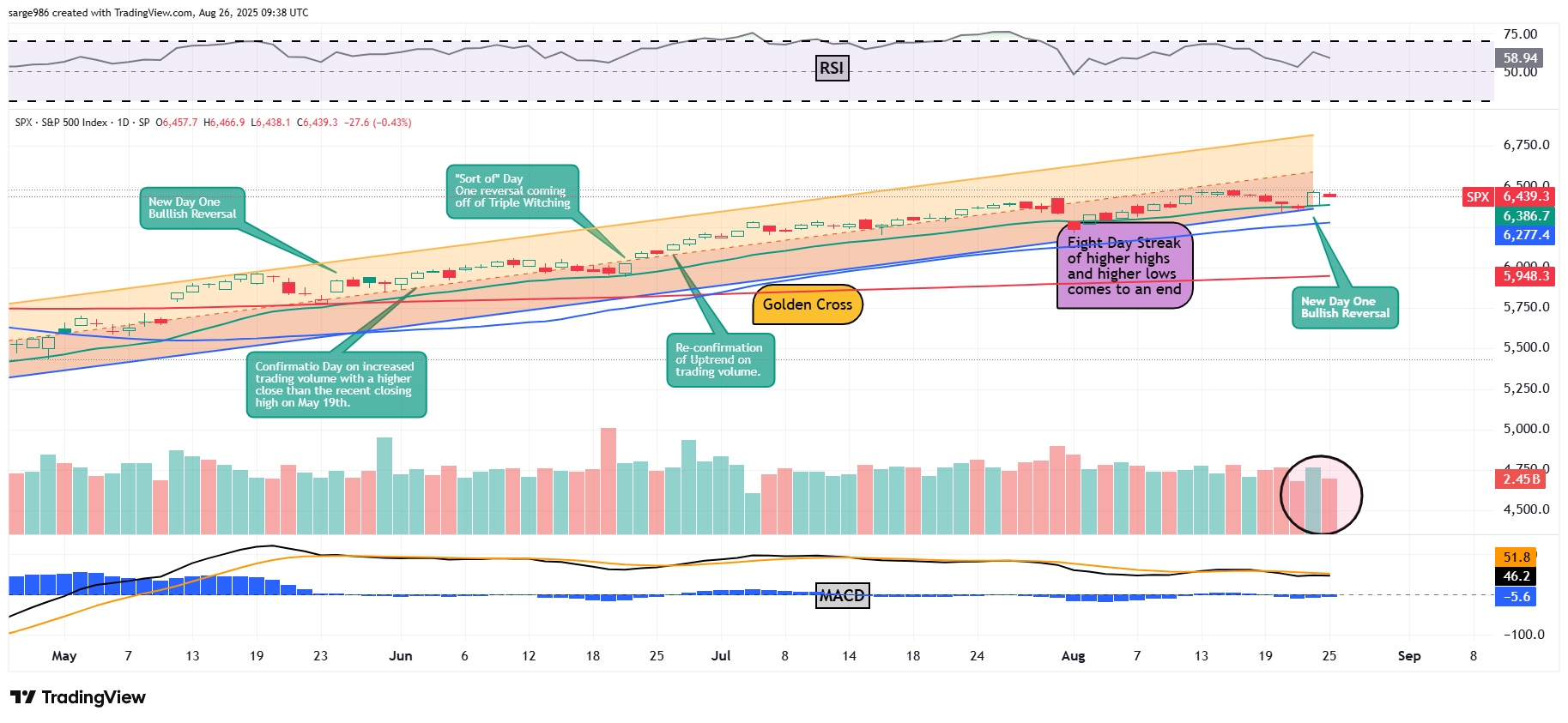

U.S. Stock prices moved lower on Monday as yields inched slightly higher across the slope of the curve. Is this the pause we called for after the Friday set-up? Perhaps. The pause could go on for more than one day, but within a few days we would need to see a day of bullish confirmation. Make no mistake, though. It may not have felt like it, but Monday's market weakness coming off of Friday's powerful rally is more of a positive from a technical perspective than it is a negative.

On Monday, the S&P 500 gave up 0.43%, while the Nasdaq Composite gave back just 0.22%. The Dow Transports took a 1.79% beating after Warren Buffet reportedly showed no interest in acquiring CSX Corp CSX and as JB Hunt JBHT led the truckers lower. All of the small to mid-cap indexes closed down more than a half but less than a full percentage point for the session. Among the mid-majors, only the Philly Semiconductors closed in the green and that was by just a smidgen.

Breadth

Nine of the 11 S&P sector SPDR exchange-traded funds closed in the red on Monday, led lower by the Staples XLP and Health Care XLV. That's key right there. If Monday's selloff were actually meaningful, defensive sectors would not have led the league in liquidation. In fact, defensives placed in the bottom the slots on the daily performance tables. Energy XLE and Communication Services XLC were the only funds among these eleven that closed out the day in the green.

Losers beat winners by a rough 2-to-1 margin both down at 11 Wall St. and up at Times Square. Advancing volume took a 47.1% share of Nasdaq-listed trade and a 35.8% share of NYSE-listed activity. Here's where it gets fun. Aggregate trading volume was lower by 19.6% on a day-over-day basis across NYSE-listed securities and 10.2% lower across Nasdaq-listings. Volume also returned to last Thursday's paltry levels across the membership of the S&P 500.

In short, technically, due to the light trading volume, Monday was not meaningful. Fundamentally, due to the outperformance of cyclical and growth stocks versus defensive types, there also was not much meaning to be found in Monday's "profit taking."

Within the black circle at the lower right hand on the chart, I have highlighted for readers, the higher trading volume on Friday's green candle day and the lower trading volumes on Thursday's and Monday's red candle days. This is bullish, as long as investors do see a second "up" day on increased trading volume. While the set-up is positive, the volume will be more difficult to achieve as the three-day weekend draws closer.

Intel's New Investor

The federal government's investment in chip designer / manufacturer Intel INTC will come over two to three tranches. The first tranche will close later today (Tuesday). That tranche will involve 275 million shares issued to the Department of Commerce at $20.74 per share of $5.7 billion. The second tranche is less well-defined and involves a $3.2 billion disbursement already allocated under the Chips Act. That would be good for 159 million shares at an even $20 per share.

The third tranche is even messier. That tranche leaves the government with 241 million warrants that would convert into common stock at $20 per share should Intel's stake in its own foundry business fall below 51%. Those first two tranches would leave the U.S. government with a 9% stake in Intel. I had previously seen this stake stated in the media at 10% or at 9.9% in Intel's corporate press release. The math says it's 9%. I am a math guy. I'll go with the math for now.

For those interested in such things, the government will be free to sell these shares in broadly syndicated offerings as soon as Aug. 26 of next year. So, does a huge investment by the federal government in a publicly traded U.S. company at below market prices really help the share price? Not necessarily in my opinion. I mean I guess investors can be reassured that there will be good support at the $20 level should the price remain above that price. That said, should the federal government choose to sell its shares, that could happen as soon as one year from now. Not that the government necessarily would, but selling 9% of the company would surely ding the stock.

To Be Honest...

Pres. Trump posted to social media, "I will make deals like that for our Country all day long." The president added "I will also help those companies that make such lucrative deals with the United States." ... and he wrote, "More jobs for America!!! Who would not want to make deals like that?"

I am not so sure I like this one. I am, as most readers probably can see, though I try not to be political, an Austrian-style economist at heart and a purist when it comes to free-market capitalism. I believe that capitalism, with all of its warts, is the only economic system that over time has ever lifted entire classes of people out of poverty, and for the most part, done so without leading to the mass violence that other economic systems are so well-known for.

Heck, I have lived below the poverty line more than once in my life. I know that capitalism works in microcosm because I never could have risen from poverty to where I run my own business and become what most people would call "successful" in any other system. Is it hard work? Of course it is.

Maybe some folks need to keep their hours down to fifty or sixty hours a week. I will work until the work is done. I am in my early 60s and still work more than 80 hours a week. That's not bragging. I know what it's like to have to support a family of four with two young kids with little income and no safety net, while throwing 80-pound bags of dry cement around all day. I don't ever want to go back there.

That said, this move, despite the president's executive order from back in February that enabled the nation to start a sovereign wealth fund, does scare me a little. That means that there will be more of these deals. While it makes some sense, especially if it does support domestic job creation, it does come too close to socialism for me to become truly comfortable with the idea. I would have to worry about the government having the ability to pick winners and losers. Almost as if he heard me, on CNBC on Monday morning, Kevin Hassett said, "We're absolutely not in the business of picking winners and losers." I guess we'll find out. Color me less than enthusiastic.

Economics

(All Times Eastern)

08:30 - Durable Goods Orders (Jul): Expecting -3.9% m/m, Last -9.3% m/m.

08:30 - ex-Transports (Jul): Expecting 0.2% m/m, Last 0.2% m/m.

08:30 - ex-Defense (Jul): Expecting -2.1% m/m, Last -9.4% m/m.

08:30 - Core Capital Goods (Jul): Expecting 0.2% m/m, Last -0.7% m/m.

08:55 - Redbook (Weekly): Last 5.9% y/y.

09:00 - Case-Shiller HPI (Jun): Expecting 2.9% y/y, Last 2.8% y/y.

09:00 - FHFA HPI (Jun): Expecting 0.0% m/m, Last -0.2% m/m.

10:00 - CB Consumer Confidence (Aug): Expecting 97.2, Last 97.2.

10:00 - Richmond Fed Manufacturing Index (Aug): Expecting -17, Last -20.

4:30 p.m. - API Oil Inventories (Weekly): Last -2.4M.

The Fed

(All Times Eastern)

08:30 - Speaker: Richmond Fed Pres. Tom Barkin.

Today's Earnings Highlights

(Consensus EPS Expectations)

After the close: BOX (.31), MDB (.66), OKTA (.85), PVH (2.00)

At the time of publication, Guilfoyle had no position in any security mentioned.