Doug Kass: We Rallied, But It's Still a Bear Market

The bad news is we're likely in a protracted bear market and recession risk is high. The good news: the best daily returns are achieved during bear markets.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Despite the rally yesterday, we are likely in the early stages of a protracted bear market that started in late January. In fact, recession risks are probably still close to 50% as the Federal Reserve has dug itself into a policy box and the China-tariff war is only getting hotter. We continue to view January as an important market and Magnificent 7 top -- similar to the major market and Nifty Fifty tops experienced in January, 1974 -- and we would not be surprised by a possible retest of the recent lows

Yet, remember that over history, the best daily returns are achieved during bear markets (see chart below) -- yesterday was probably no different than the previous bear market rallies. We sold out most of our trading long rentals in the spectacular rally late on Wednesday.

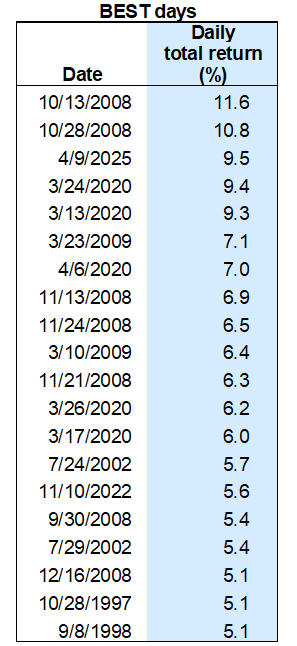

Most of The Best Daily Returns Since 1990 Have Occurred in Bear Markets

"A bull market tends to bail you out of all your mistakes. Conversely, bear markets make you pay for your mistakes."

- Richard Russell

Before you continue reading this, please consider my comments within the context of Warren Buffett's teachings: "Market forecasters will fill your ear but will never fill your wallets."

I am not being humble, I am being honest. As I always write, I often make mistakes (I have the scares to prove it!) and I am always in doubt. No hubris here -- as, unlike some (who are trying to sell a service) I don't have exaggerated pride or self confidence. I know, after all these decades, that Mr. Market exists to embarrass us all.

Certainty Is the Death of Wisdom, Thought and Creativity

Over the last year I have claimed that we have unjustifiably been in A Bull Market in Certainty -- arguing that certainty of bullish outcomes (incorporated by the consensus and in a 23-times price earnings multiple) was unwise. Resultingly, up to late last week I maintained an ursine market view.

That began to change four days ago, as in the teeth of the vicious market decline I materially expanded my long exposure.

I got lucky on Tuesday (the day before Wednesday's "face ripper") in which I outlined the case ("A Bear Turns Short-Term Bullish") for a sharp and imminent rally within the context of a Bear Market.

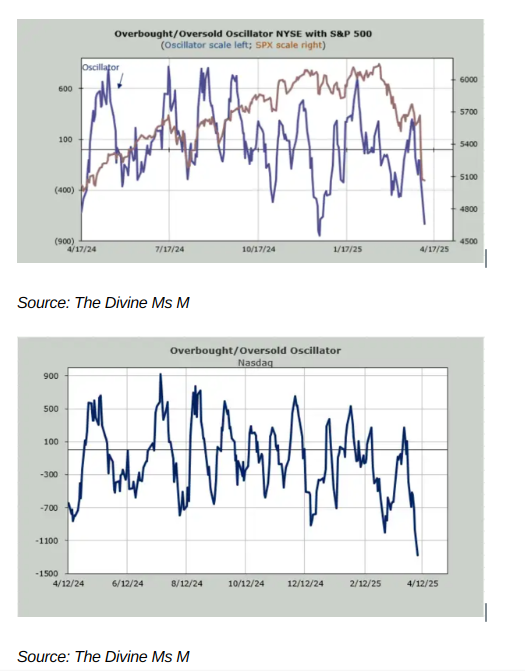

Besides a meaningful oversold and bearish sentiment extreme (manifested in the spike to 60 in the VIX, an oversold Oscillator, low relative strength index, prepondernce/unprecedented Bear/Bulls ratio and fearful sentiment surveys (CNN Fear & Greed etc.) -- the fast (and scary) weekend climb in interest rates and the rapid and deep capital destruction in our capital markets (over the last six weeks) were instrumental to our view of expecting a market rally.

But even more importantly, we saw the need and likelihood of a quick adjustment in tariff policy by the President. As we wrote on Tuesday:

Peak Tariff Concerns: We are almost certain that the hard line in the Trump administration apparent tariff's policies will be softened. As always, President Trump starts big in his threats. Any pause, easing or softening in policy (very likely) could reverse the recent downturn in sentiment in a backdrop of rising shorts, liquidation, emotional selling and near panic selling in certain individual stock prices (some of which have gotten back to great upside/downside opportunities for the first time in several years)

Here is our complete post (two days ago) which anticipated an imminent rally:

A Bear Turns Short-Term Bullish

In the last two days I have shifted to the largest net long exposure I have had since the last half of 2023.As of the close, the S&P Index is -14% and the Nasdaq Index is -19% in 2025.At the worst levels Monday the S&P Index was -19%A (year to date), worse than the downside of about -15%E (vs. expected upside of only +5%E) that I projected at the beginning of this year.

Extreme Sentiment: With sentiment at a bearish extreme (as measured by the CNN Fear and Greed Index at "3"), the AAII bears/bulls, the VIX spiked to 60 (it's now back down to a still-elevated 43) and the extremely oversold S&P Short Range Oscillator (-8.7%) I was confident that the sentiment factors had turned extremely negative, perhaps providing a backdrop for taking on more long exposure.I can't lie, Jim Cramer's panicky expectation on Sunday of a "Black Monday" had some impact on my new-founded buying strategy! It was a manifestation of the market's pessimism.

Still Weak Technicals: While the technicals continue weak and somewhat ambiguous, the fundamentals were finally accepted to be deteriorating (as we have warned and feared).

Better Reaction to Bad News: And, Monday, equities rallied, even in the face of continued and stern tariff warnings from the president.

Peak Tariff Concerns: We are almost certain that the hard line in the Trump administration apparent tariff's policies will be softened. As always, President Trump starts big in his threats. Any pause, easing or softening in policy (very likely) could reverse the recent downturn in sentiment in a backdrop of rising shorts, liquidation, emotional selling and near panic selling in certain individual stock prices (some of which have gotten back to great upside/downside opportunities for the first time in several years). (Note: I added a number of new longs to my Watch List over the weekend.) As a consequence, we were very active on the buy side — throughout the entire morning weakness, adding further to the indices on each pullback...

Bear Market Rallies

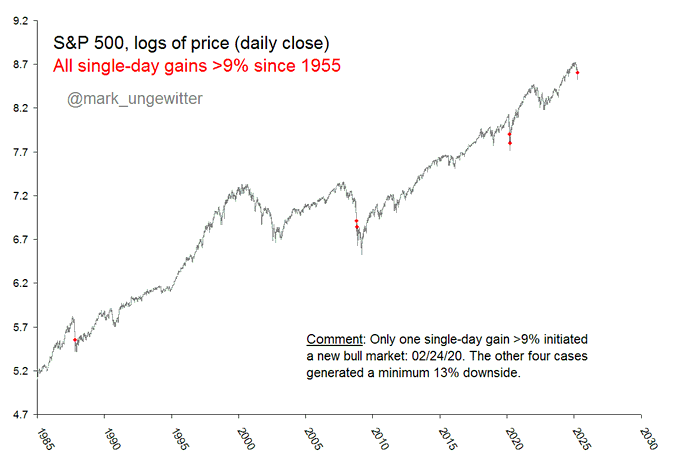

As seen the chart I started this column with (above) and the chart that follows (note the large daily gains in red), the best rallies occur in bear markets and during crises -- in fact, bear market rallies of the order of magnitude that occurred on Wednesday (+9.5%) are more of a signpost of emerging economic and liquidity problems than indicative of a healthy stress-free global economy or capital market:

Here are some thoughtful observations from Dan Niles:

Just for fun, I looked at the two big up days during The Financial Crisis -- October 13, 2008 (+11.6%) and October 28, 2008 (+10.8%). From the Oct. 13 close to the Oct. 14 intra-day peak was around +4%, then the market reversed and closed down. Unlike today so far, it opened strong that day.

From the 10/28 close the market moved up another +7.5% over the next 5 trading days before the bear resumed.

Improvising Tariff (and Fiscal) Policy Bodes Poorly for Our Markets and Economy

* A comprehensive, well thought out global tariff policy is far different than a transactional NYC real estate deal

* The U.S. has become, increasingly, an unreliable and undependable partner

* Global economic growth will suffer

A real estate deal in New York City is dissimilar to establishing global tariff policy.

The improvisational manner in which the President appeared to create and then alter tariff policy is disarming -- for our markets and for consumer and corporate sentiment and spending.

It is unclear that President Trump actually understands how international trade actually works:

Justin Wolfers posted on X: "It's an extraordinary question to have to ask you, but do you think Donald Trump actually understands how international trade actually works."

Finally, the rationale for tariff policy keeps changing. Remember when it was all about bringing manufacturing home? (That was two days ago!). Now its about negotiating deals.

Those two objectives are in tension. ("Is a company willing to build a factory in the U.S. if tariffs are likely to persist?")

The 90-Day Tariff Pause Will Likely Stall the Global Economy

Why would any company proceed with capital and spending plans in the face of the continued uncertainties of policy?

More domestic and global economic concerns:

* The odds of a recession are still about 50%

.* The Administration is not going to get "big" wins: Tariffs were low before this and if the President negotiates competently, they will be low again. Basically there is no gain. (We have seen this before when NAFTA got relabeled by the President in 2020, but the agreement really didn't change much).

* During the 90-day pause, the U.S. will still have the highest tariffs in the world, perhaps more than 10-times - 20-times that of most of our trading partners and roughly 10-times higher than it was before. These are still at or above the Depression-era Smoot-Hawley tariffs.

The Rest of the World Suffers From Rising Volatility

Execution risk is always challenged with rapidly rising volatility. Many leveraged players (think Long Term Capital, etc.), in particular, will not be able to navigate the journey and there will be casualties along the way:

Still More Questions and Uncertainties

Here are some questions I do not have the answer to, but, boy, I would love to know:

* What caused them to cave on the tariffs? Was it the equity markets, the Treasury (basis trade unwind)/debt markets and financial plumbing issues, or other?

* Are we in a better position now than we would have been in if we started with a more measured and negotiated approach to all of these issues? Or are we now worse off that we went down this path, and backed off, and now leverage has been lost as it shows we don’t have the stomach for a big and protracted fight?

* It was also amusing watching a 10-year auction at 4.43 being celebrated when it was sub 4.00% last week...

* Make America Scammy Again? (MASA) Was there foul play? Who knew about the 90- day pause in tariffs announcement?

Once again, it seems more than one person trading stocks knew. The Nasdaq was up about +1.5% at about 10 a.m., when one would think it should have been pretty soft in the morning based on what went on overnight. Same guys in the basis trade (per first dash) would be the same people most likely to have the direct line to those dealing with the financial plumbing issues. Who knows, but the open Wednesday morning being pretty firm was interesting.

Take a closer look at the options market, with the calls that expired on Wednesday! Those that are wiser were probably buying straight equities (albeit on a levered basis):

There are a lot of other issues at play with the equity markets still, that have nothing to do with tariffs.

The AI/Mag 7 unwind, softer consumer, sticky inflation, credit markets (and rates still did not back off with the massive equity rally), valuation, still a general lack of confidence and confusion among consumers and company executives (who will still have no idea how the tariff thing will resolve and what to do in the interim), global instability, and a broken and self destructive political system that has more interest in destroying the other side than productive solutions.

Who's Your Money On?

Then there is the continuing tariff saga between the U.S. and China, which will likely remain unresolved for some time:

Bottom Line

"We sail within a vast sphere, ever drifting in uncertainty, driven from end to end."

- Blaise Pascal

The events of this week are not growth or valuation friendly. Rather, they could trigger even greater instability.

The events of this week uncovered some of the market structure concerns (in a leveraged capital market system) that we have opined about over the last twelve months.

The events of this week underscore the risks of improvisational fiscal policy.

There remain downside risks to economic growth and upside risks to inflation.

We believe that a protracted Bear Market began two months ago. Similar to the top in The Nifty Fifty in January 1974 a seminal rotation out of Mag7 began in late January, 2025.

Wednesday's rise in the S&P Index of +9.5% was the third best daily rise in history. Unfortunately and over history, most of the largest daily market rises occurred during bear markets.

Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected.

The unexpected would be a retest of the recent market lows.

I would sell all rallies.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.