Doug Kass: Time to Rethink American Exceptionalism

Structural uncertainties, limited fiscal discipline and imprudence around the globe could add up to some big shifts for the future of the nation -- and an end to the free (macro) lunch.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It's time to rethink American Exceptionalism.

I write this statement as political and geopolitical polarization and competition are likely poised to translate into less political centrism and a reduced concern for deficits. This is creating structural uncertainties, limited fiscal discipline and imprudence around the globe; it could also cause the bond markets to "disanchor." At the same time, the cracks in the foundation of the bull market are multiple and are deepening -- and still yet ignored. Even JPMorgan CEO Jamie Dimon's dour comments on complacency and his view that the corporate credit market is "ridiculously over-stretched" are being dismissed. And we continue the creep toward slugflation.

For investors, particularly, looking up to the S&P 500 Index at 5965, the downside risk now dwarfs the upside reward for equities (in a ratio of about 3-1 negative). Valuations and (consensus) expectations for economic and corporate profit growth are all inflated.

"In investing, there are no called strikes. People can throw any stock at me and I don't have to swing - and nobody is going to call me out on called strikes... It's an enormously advantageous game."

- Warren Buffett

High Expectations

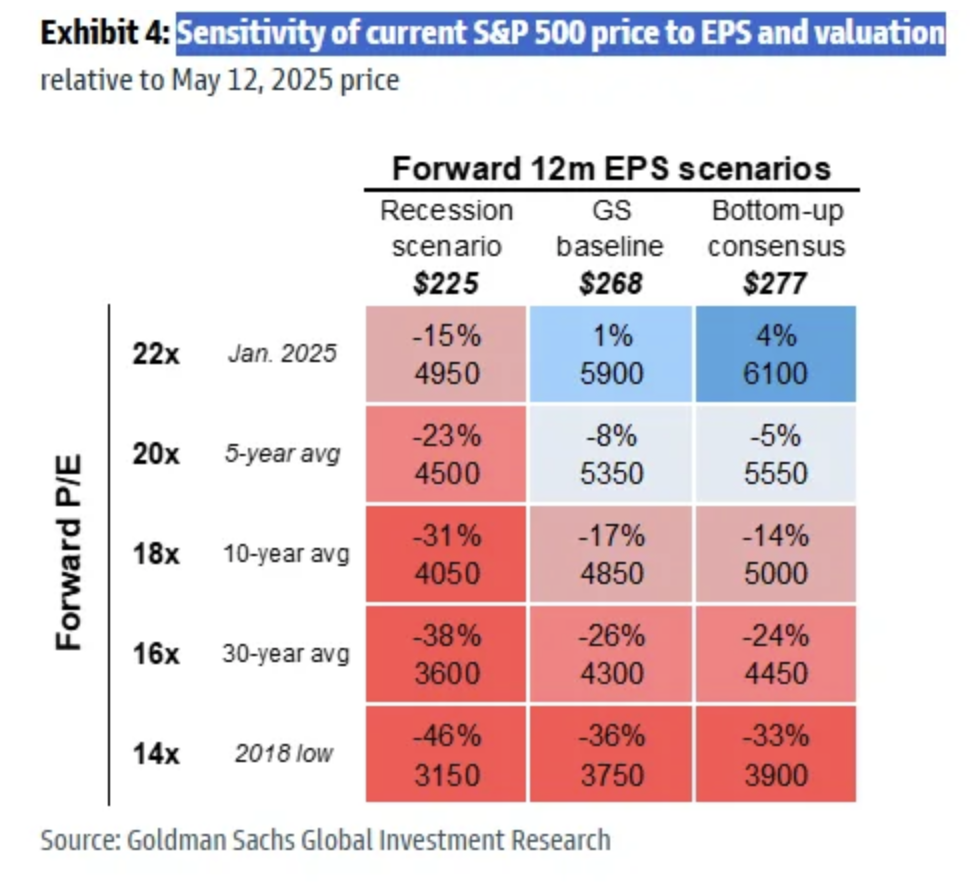

At the core of my ursine market view, as I've said in my posts and at my hedge fund Seabreeze Partners, is that consensus profit expectations are too high. I remain defensively positioned in the belief that consensus S&P 2025-2026 earnings per share expectations of $270/share are too ambitious (and likely to fall closer to $250/share).

The S&P 500 Index currently stands at about 5965. Here is a reasonable sensitivity matrix of S&P profit, valuation and price expectations; it identifies the degree of risk to stock prices should, as we expect, corporate profits disappoint and price earnings multiple decline:

There are numerous potential and deepening cracks in the foundation of economic and profit growth, setting the stage for an unattractive upside reward vs. downside risk for the U.S. stock market over the remainder of the year.

Most importantly, the excess stock market valuations (greater than 21-times), partly associated with the acceptance of the notion of American Exceptionalism, is likely to unwind as U.S. dominance is increasingly questioned by other countries.

As in the 1947 play, A Streetcar Named Desire, the U.S. has begun to resemble Blanche DuBois, the aging Southern belle who lives in a perpetual panic about her fading beauty and concerns about how others perceive her looks -- "relying on the kindness of strangers" to fund our twin deficits.

In the case of the U.S., those strangers (other countries) are investing in their own undervalued equity markets, stimulating their home economies and bringing their savings home.

If this continues -- and it likely will -- the centerpieces of globalization (a strong U.S. dollar and highly valued U.S. equities and Treasuries) will continue to suffer in a regime change.

Moreover, current price earnings multiples demand near perfection of economic and profit outcomes. Unfortunately, there has rarely been so many possible outcomes (many of them adverse) as there exists today.

As in late 2021, there are numerous fundamental concerns that immediately confront investors today (and are being ignored):

It is our continued expectation that interest rates (and inflation) will likely stay high and valuations are back to being inflated (after the recent market rally).

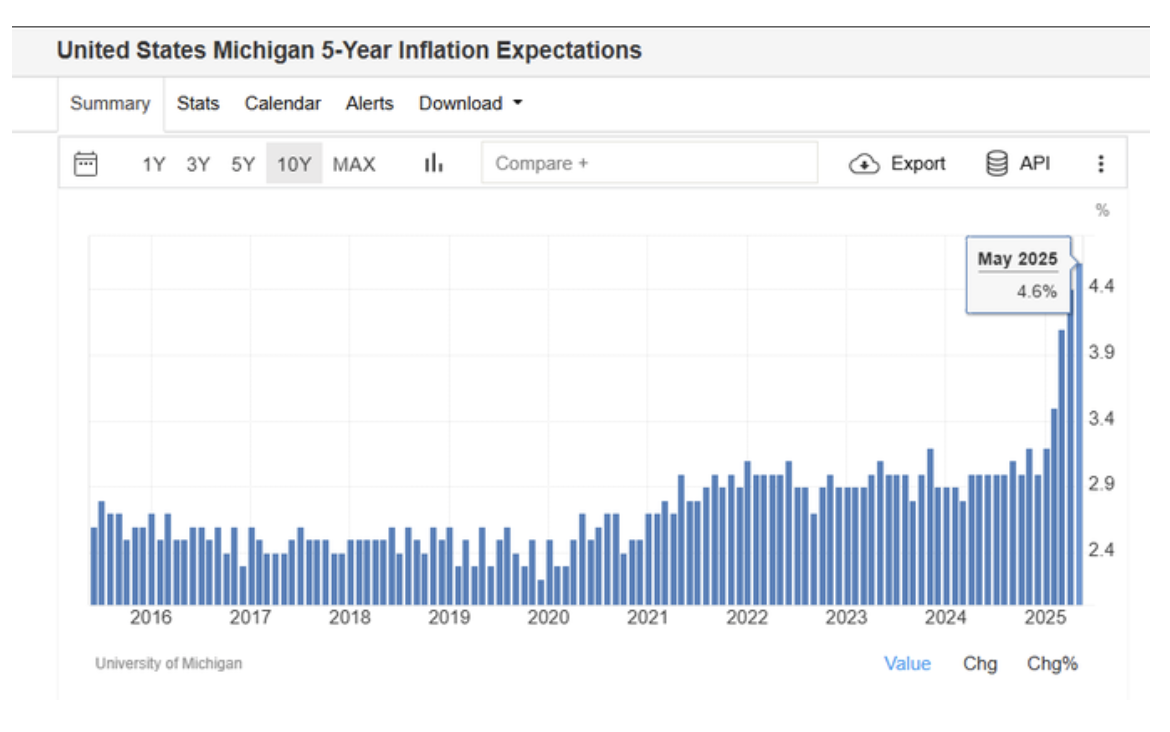

Rising Inflation

Inflation expectations are climbing:

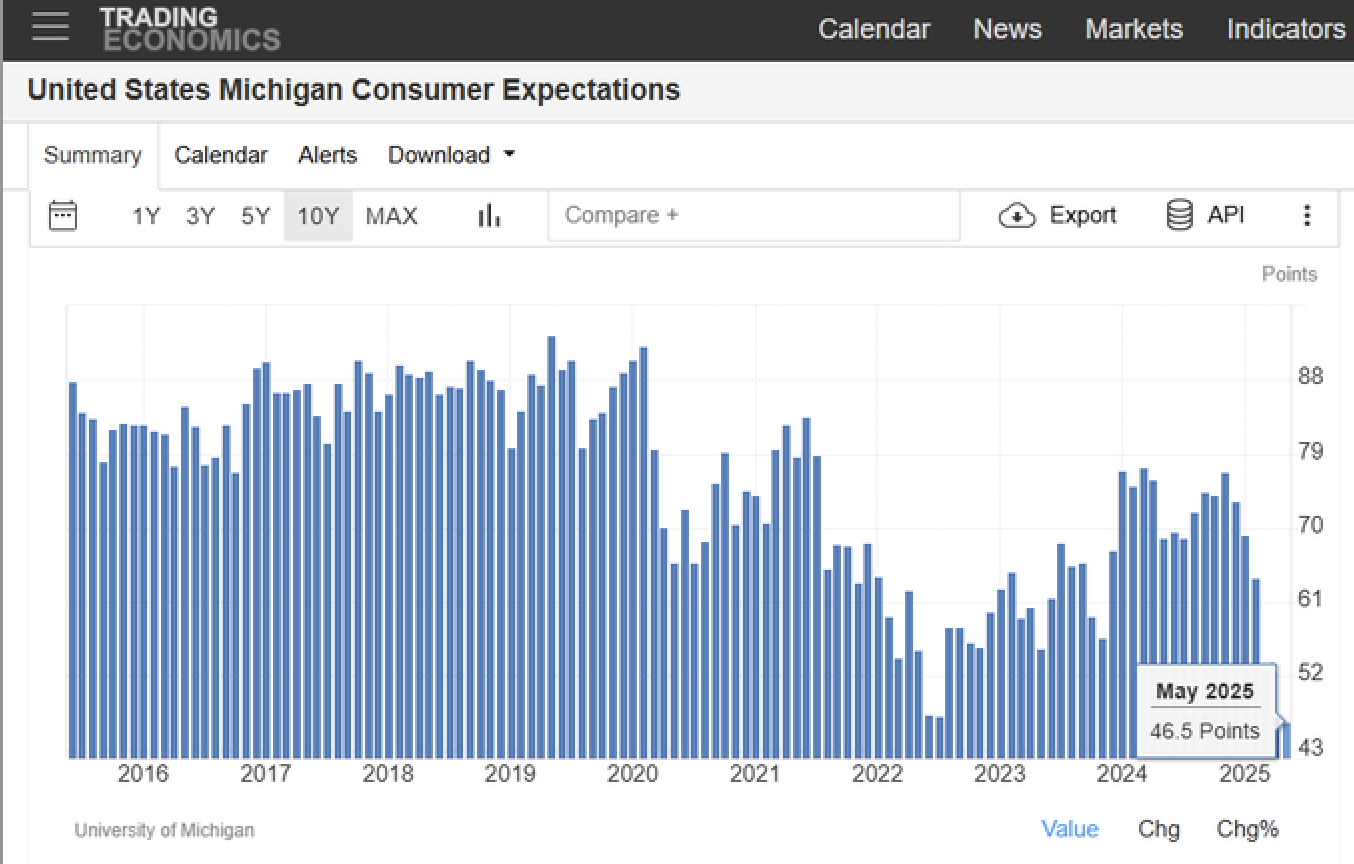

Fiscal Imprudence, Rising Interest Rates and Souring Sentiment

Recent proposals point to even greater federal budget deficits than are currently in place.

- Barron's

The failure of either party to address federal budget deficits is giving the bond market, charged with funding those deficits, a darkening mood.

The yield on the 10-year benchmark Treasury note has risen by 30-basis points recently (to 4.50%) while the 30-year long bond yield has climbed by 40-basis points (to 5.00%) -- levels that provide equity -- like returns with little risk and volatility.

This climb in interest rates is occurring even as consumer sentiment is eroding:'

Rethinking American Exceptionalism

"You can ignore reality, but you cannot ignore the consequences of ignoring reality."

- Ayn Rand

In this morning's missive we will begin to look longer term and consider the consequences of the economic and profit cycle, the turn away from globalism and towards reshoring (and its deleterious impact on profit margins) and other factors that could result (much like the Pharaoh's prophecy) of substandard stock market returns over the next few years:

In the Bible, 'lean years' refer to a period of famine that follows a time of abundance, particularly in the story of Joseph in Genesis 41. The prophecy, revealed through dreams to Pharaoh, foretold seven years of great plenty in Egypt, followed by seven years of severe famine. Joseph, interpreting the dream, advised Pharaoh to prepare for the lean years by storing grain during the period of abundance. This preparation allowed Egypt to survive the famine while other surrounding lands suffered greatly.

The post Cold War era of endless credit, inexpensive labor, military neglect, product (supply) reliance on our political adversaries, energy dependence, unchecked migration, and the illusion of high margins was never unsustainable; it was always brittle.

The illusion of prosperity was elongated with the $5 trillion Covid stimulus packages and a $20 trillion rise in our country's debt load. Wall Street and our capital markets thrived (with only one or two temporary pauses) even though Main Street suffered from stagnating real wage growth, the disconnect and schism between headline prosperity and lived experience grew ever wider.

But, all the while, reality was catching up as the foundation was cracking.

It was the system that aged and inevitably buckled under its own contradictions.

Change, especially of the political-kind that we are see today, was inevitable.

The recalibration or realignment that we are likely to begin witnessing may be violent or gradual - the course is currently uncertain - but is bound to be messy and has only started.

To us, the likely adverse impact of valuations seems more certain.

The subject is broad and spending a couple of thousand words expressing my views doesn't do justice to the topic.

Let's call this... Rethinking American Exceptionalism.

We all recognize that the America's Exceptionalism and our country's safe haven status will likely continue. Our "system" is superior and the most trusted in the world -- whether ranked economically or legally.

Nonetheless, we are concerned, at the margin, that our Exceptionalism is "less so" -- and, as such, will likely hurt stock market valuations. result in equity diversification away from the U.S. and lead to further increases in domestic interest rates.

Let's very briefly summarize the major foundational cracks:

* The Reversal of Globalization Will Become an Expensive Truth for Corporations and Consumers: Tariffs proposed are leading to ever higher inflation and lower S&P profits. As to the tariff "pause," investors appear to be convinced that a 30% tariff rate on China and a 13% average tariff rate on the world (compared to 2.5% in 2025) are both normal and manageable. (Nothing like a 10-percentage point levy on this $30 trillion beast called "Global Trade.") This will lead to higher inflation over the balance of the year, serve as a consumption tax on the U.S. consumer and lead, according to Strategas' David Clifton, a 1% reduction in GDP.

* Our Trade Deficit and Debt Load Is Not Being Addressed by Either Political Party: The Administration's Department of Government Efficiency (DOGE) effort has failed to save taxpayers much and the Democrats are unwilling to approach our deficit and borrowings in a serious manner. We are of the view that our country's pristine debt rating could be subject to downgrades in the months ahead.

It can be now argued that U.S. debt growth is unsustainable. Already non-U.S. investors are avoiding our debt. This may create a demand shock as other countries begin to disinvest from our Treasuries. Yields will likely rise, which will trigger inflation because the Treasury will have to print more money -- causing a death spiral of debt.

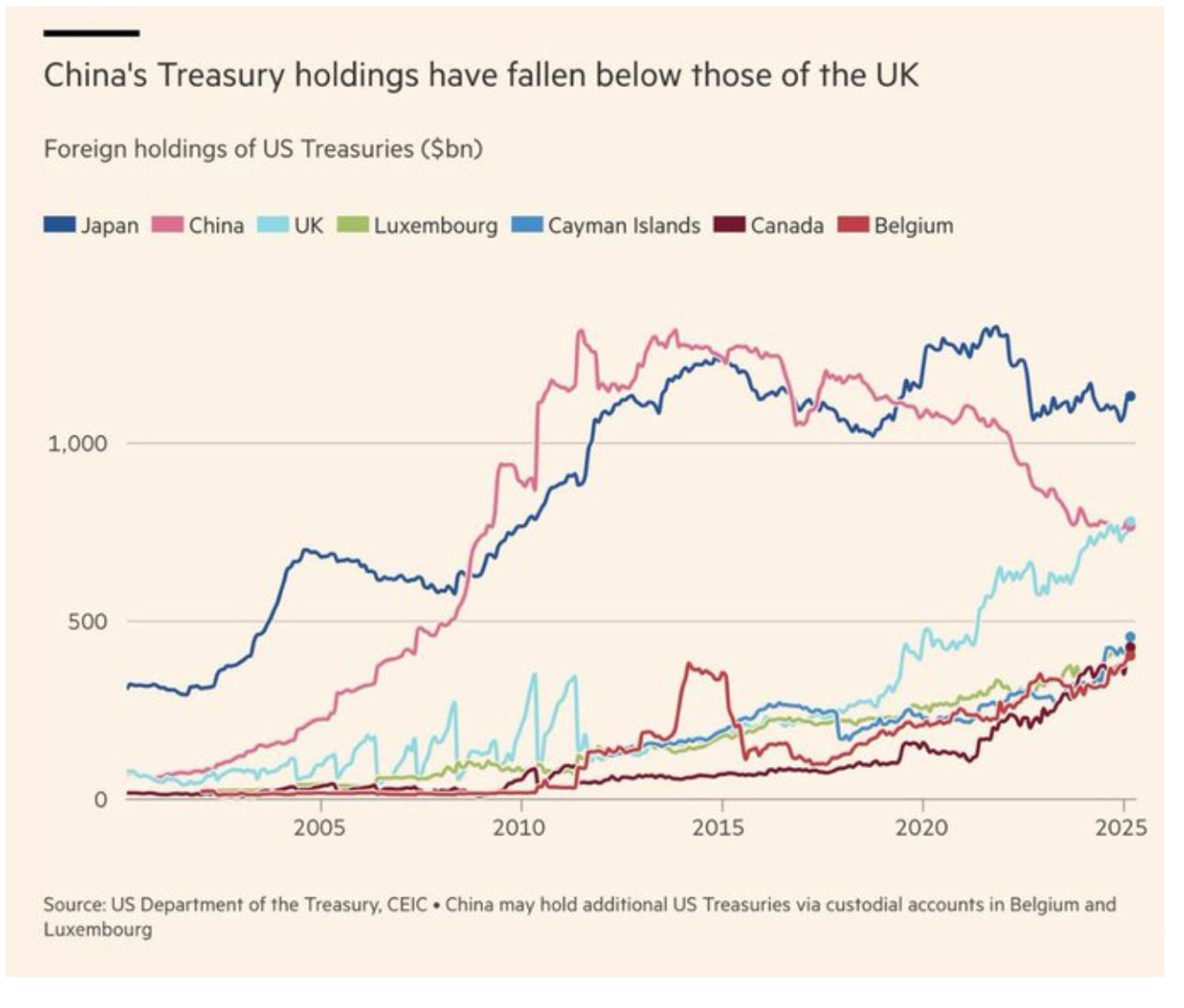

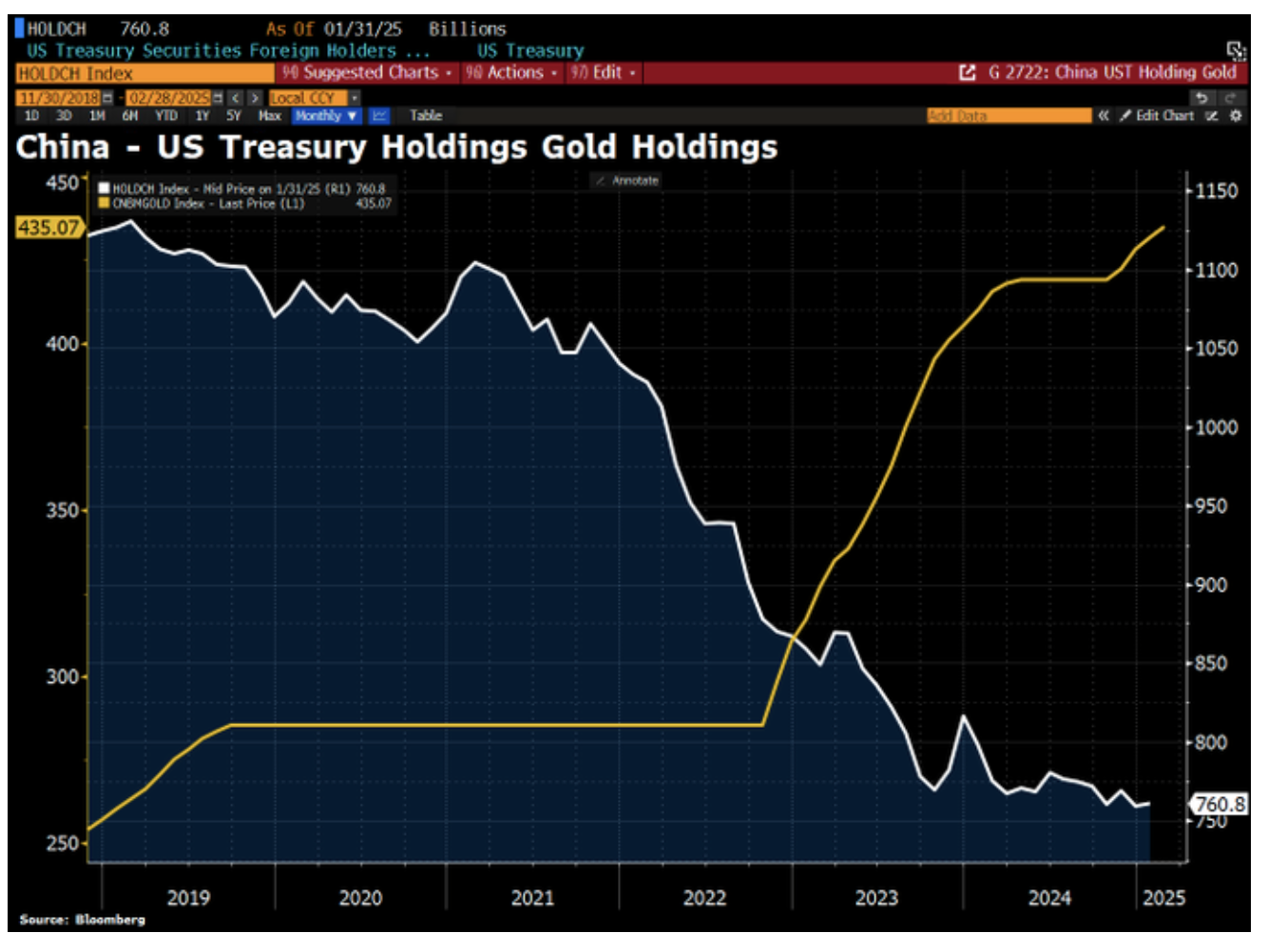

The largest holders of our debt (Japan and China) are liquidating our Treasuries at a rapid rate. The U.K. is picking up the slack but, as previously noted, this is not keeping U.S. interest rates from rising; the long bond is at the highest yield in 18 years:

In place of U.S. Treasury holdings, China is buying gold:

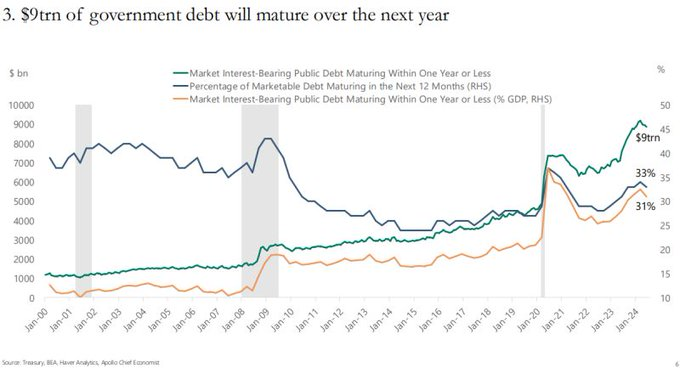

At a time in which the U.S. needs to refinance $9 trillion of debt in the next 12 months - interest rates are climbing and the Fed is quantitatively tightening:

There are only two ways to sell so much debt:

* With higher yields.

* Or the Fed steps in and buys the debt.

Both outcomes are inflationary.

Knowing this, investors will likely demand higher yields - leading to more adverse rate and economic outcomes:

Seeing the U.S. dollar as an inflationary asset, other countries could accelerate the sale of our debt, raising the risk that the dollar will no longer be seen as the reserve currency of the world. This possible condition is what Bridgewater's Ray Dalio describes as the "breakdown of the global monetary order."

At the same time, the self-induced tariff "crisis" is being manifested in continuing inflationary pressures, making it difficult for interest rates to drop, reinforcing the debt problem and likely producing "slugflation" (sluggish economic growth/persistent inflation).

Bottom Line

“I'm not terribly affected by the fact that the crowds are agreeing with me or disagreeing with me. I'll do whatever my own sense tells me. The trick is simply to sit and think.”

- Warren Buffett

To paraphrase Winston Churchill, the rally of the past few weeks does not likely represent the end of the market's decline. It is more likely that we are facing the beginning of a broader market decline (that initially began in January 2025). Our baseline expectation for a negative return for the S&P 500 Index in 2025 remains unaltered. Equities likely peaked (for the year) in January and large cap technology stocks (The Mag7) may have reached a seminal top three months ago (much like The Nifty Fifty topped in January, 1973). We see some potentially serious cracks in the foundation of economic and corporate profit growth - and in global economic cooperation:

* Higher Debt = Higher Interest Rate Burden

* The Fed Is Trapped Between Inflation and Insolvency

* Dollar Reserve Status is Eroding

Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits- creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor."

U.S. debt, in particular, will likely weigh on future S&P investment returns.

This is not the end of the U.S. safe haven status nor does this imply a systemic collapse.

But it is likely end of the free (macro) lunch.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass was short SPY common (M), QQQ common (M).