Doug Kass: This Market Sees No Evil, Hears No Evil

Markets have ignored the same conditions that set off the January-February selloff and none of the non-war issues have been resolved.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The strength and rapidity of the market's rally, especially since March) has likely been momentum-driven (due in part to market structure changes over the last decade in which passive products and strategies have dominated the investment landscape). This backdrop of momentum based machine-driven dominance — in which buyers buy strength and sellers sell weakness — has, in turn, led to a great deal of fear of missing out. These factors and others have contributed to a record pace of recovery ("V"-type) from the March, 2026 lows.

While I pivoted long in the second half of March, I quickly took profits and eliminated many of my longs late last week.

The magnitude and strength in the major indexes over the last week have been anathema to me, and especially to those with a value (and non-momentum based) orientation.

At times like this I am reminded that incredulity robs us of many pleasures and gives us very little in return! Or as Samuel Johnson wrote:

"To revenge reasonable incredulity by refusing evidence, is a degree of insolence with which the world is not yet acquainted; and stubborn audacity is the last refuge of guilt."

and of this by Marshall McLuhan:

"Only the small secrets need to be protected. The large ones are kept secret by public incredulity."

In my view, the markets have ignored the same conditions that set off the January-February selloff. None of the non-war issues that drove stocks lower have been resolved.

* Oil prices are off their highs but are likely to remain elevated because of the magnitude of the supply shock and continued uncertainty.

* Inflation is higher than before the conflict in Iran.

* Interest rates will be higher for longer.

* The 2026 annual deficit will approach $2 trillion, neither political party show any signs of being fiscally responsible.

* The U.S. debt will hit $40 trillion - the cost of servicing the debt is over $1 trillion/year.

* With a burgeoning deficit, stiff debt load and persistent inflation, the Fed's hands are tied.

* While private equity's problems are not systemic, the leverage they brought us remains in place.

* The enormous amount of money spent on AI will probably never see an adequate return on investment. As noted by Stan Druckenmiller, AI's societal and transformative impact could rival the internet's life changing influence — and so may the stock market consequences (rhyme) be similar:

"If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to fruition. That’s not going to happen with AI. But it could rhyme – AI could rhyme with the Internet as we go through all this capital spending we need to do. The big payoff might be four to five years from now. So AI might be a little overhyped now but under-hyped long term."

- Stanley Druckenmiller

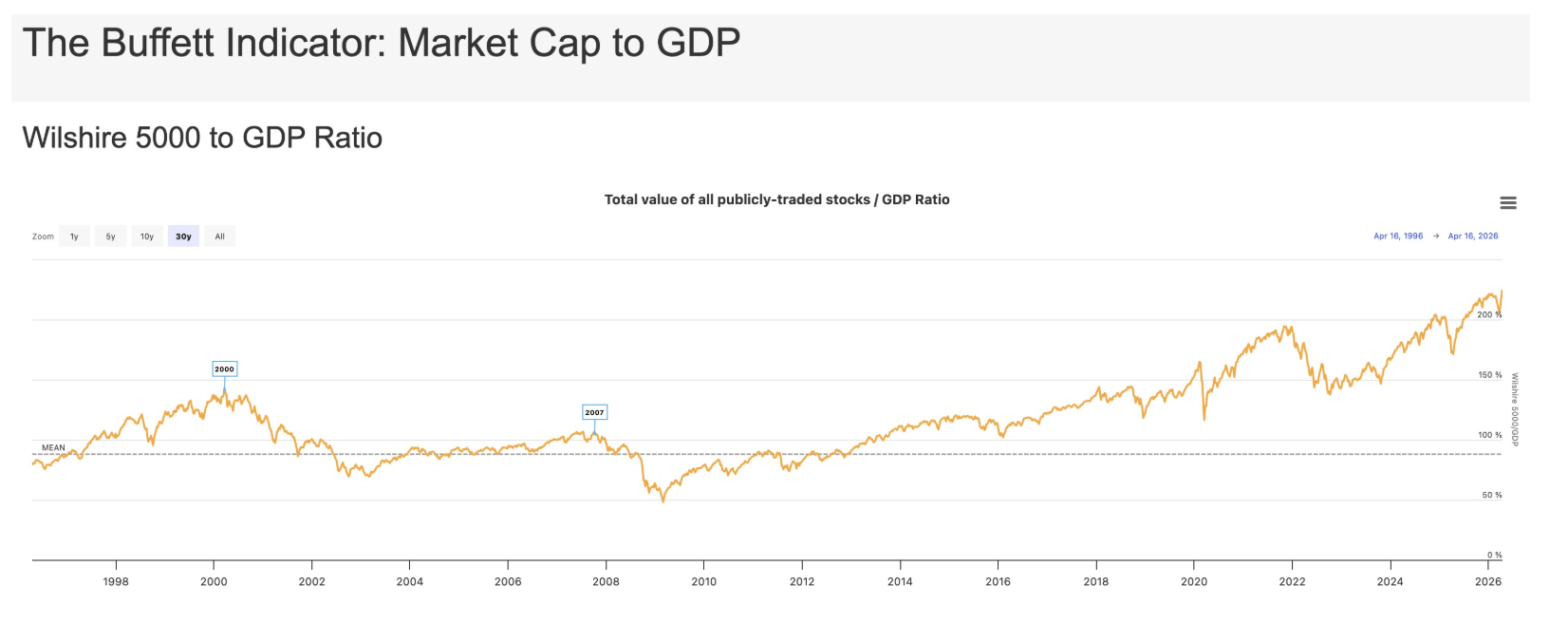

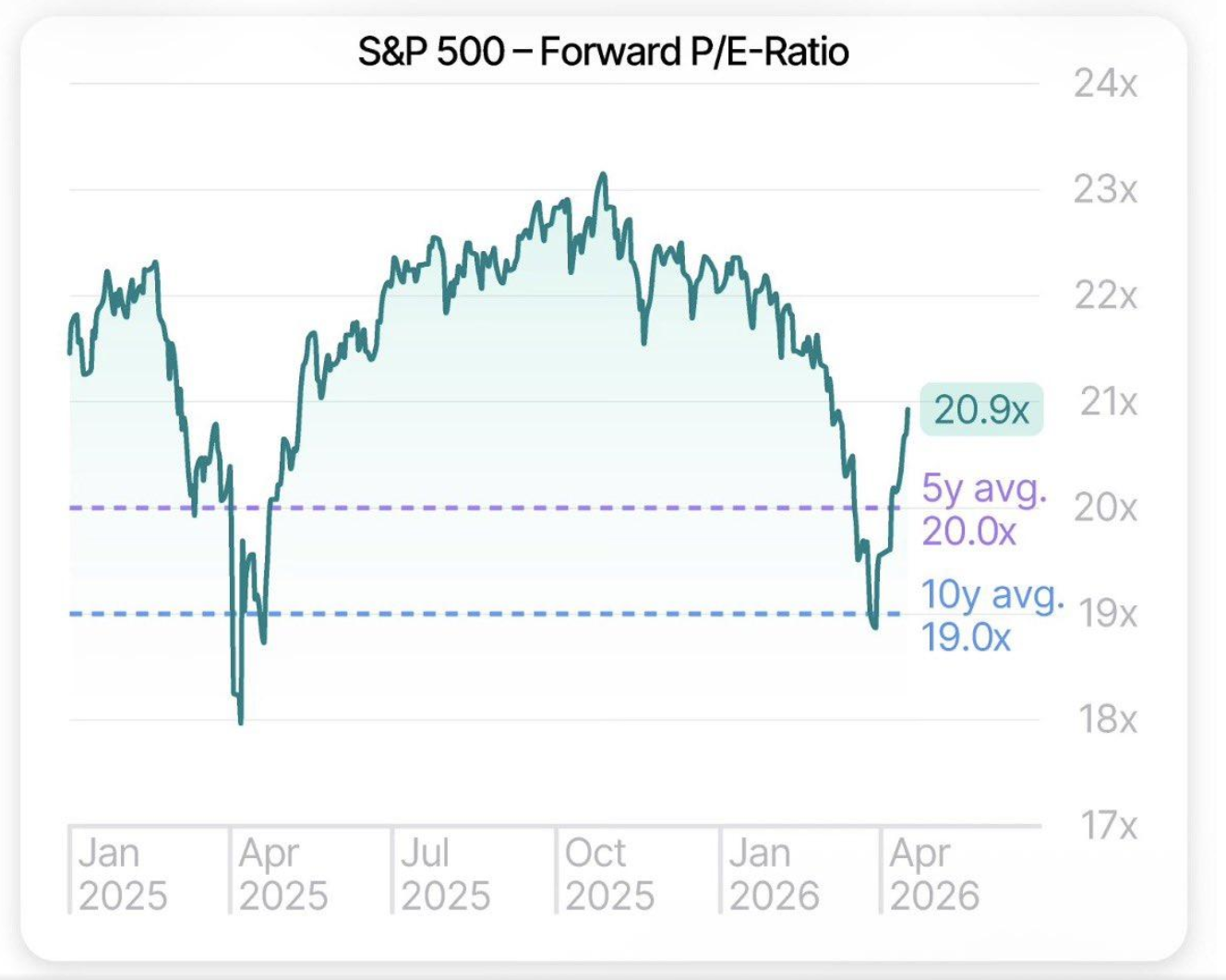

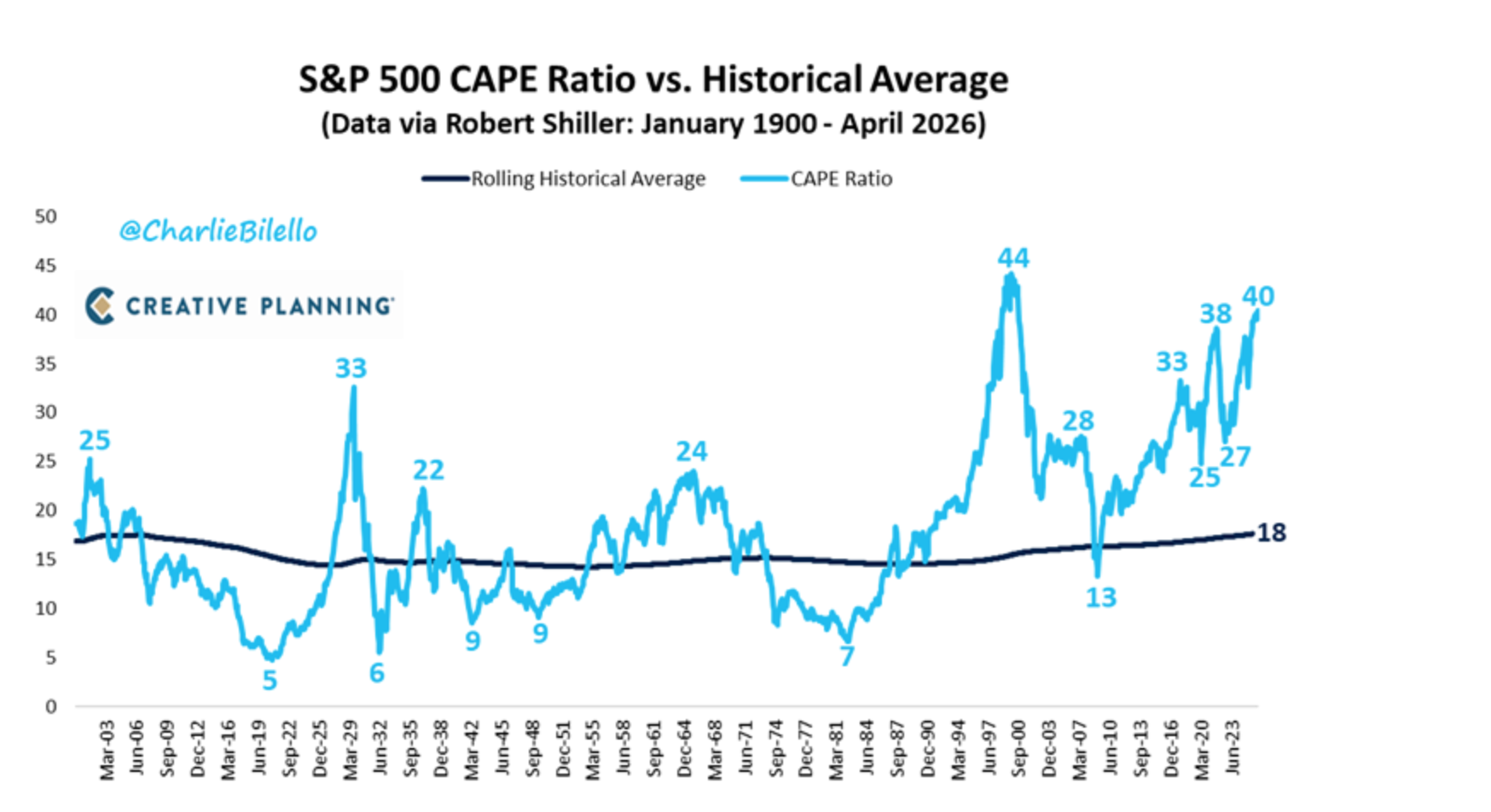

* Valuations are stretched (e.g., the Buffett ratio (the total market capitalization divided by GDP) hit an all-time high this week). Other methodologies and traditional historical metrics signal overvaluation.

Related: Peace Talk Trouble, Trump 'No More Mr. Nice Guy,' Earnings Bonanza

Valuations are a terrible clock but a good weather forecast:

And...

And ...

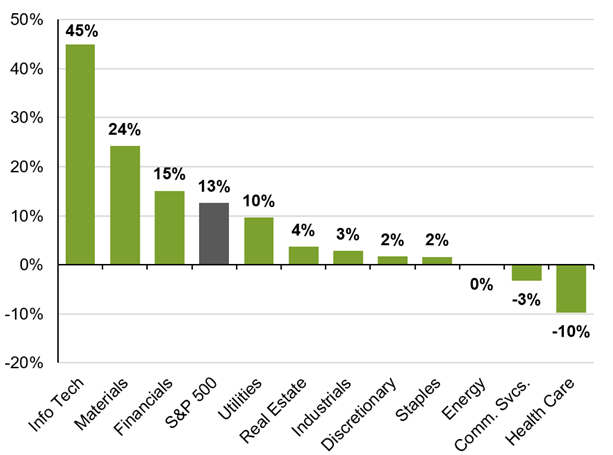

One last important bullet point (that I highlight from the above 10 issues) is that bulls argue that 2026 S&P earnings per share growth will be robust (at about +17%) — so profits justify current valuations. However, if one takes out Nvidia (NVDA) and Micron (MU) from the calculus, 2026 S&P EPS growth will be under +10%:

Bear in Mind

Most investors are now convinced we are in a continued Bull Market led by AI-related equities.

But the anatomy of a bear market, which we will not know until after the fact, is that there are violent rallies.

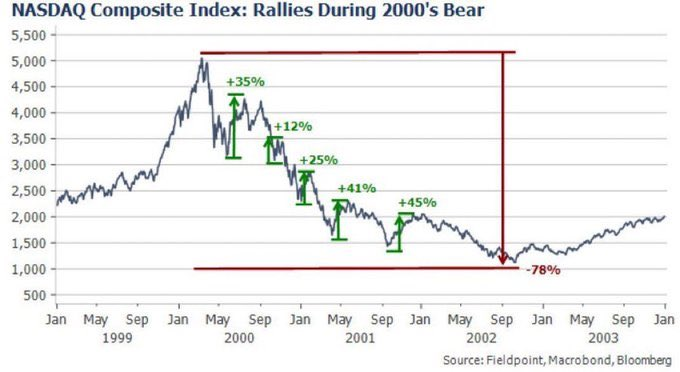

As noted above, a classic and extreme example was when the Nasdaq declined by -78% (2000-2002) following the dot.com boom in which the revolutionary impact of the internet was heralded and applauded in the indexes.

Along the way to the nearly 80% drop, there were five robust rallies of between +12% and +45%. The average gain in the rallies was +33%.

Every rally felt like a bottom but every rally was a trap:

Bottom Line

"It is always well to accept your own shortcomings with candor but to regard those of your friends with polite incredulity."

- Russell Lynes

In my Diary I share my views and try to attach empirical evidence and observations that support that outlook.

In the case of today's markets I am reminded of Warren Buffett's quote:

"What the wise do in the beginning, fools do in the end."

With the same intended message, Barton Biggs was more colorful when he said:

“A bull market is like sex. It feels best just before it ends.”

Citigroup's CEO Charles Prince — in July, 2007, only months before The Great Financial Crisis (and historic market decline) — had a different view (as reported in an interview he had with The Financial Times): “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing."

That said, with the S&P Index making an all-time record in April — and despite my protestations — it is abundantly clear that neither the markets nor most market participants (human and machine) share my outlier and ursine outlook.

Market participants are still dancing and having sex.

This commentary was originally published in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass was short SPY common (S).