Doug Kass: There Are No New Eras, Excesses Are Never Permanent

We see a multitude of cracks in the market as skepticism and doubt have left Wall Street.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* From my perch, equities are more overvalued than at any time this year.

* Current valuations are a poor launching pad for future investment returns.

* "Slugflation" likely lies ahead — as domestic economic growth is moderating and inflation is sticky.

* We see numerous cracks in forward-looking global economic fundamentals, an unclear path of U.S. corporate profit.

* Speculation has run amok with the proliferation of 0DTE options, meme stocks, Palantir (100x revenues), dip buying, etc. have led to a suspension of fear, doubt and skepticism.

* Everyone (especially "The Kids Today"), it seems, now worship at the altar of price momentum — a condition previously seen in the Winter of 1999, the Summer of 2007 and in late 2021.

What follows is a summary of some of my recent Daily Diary contributions on TheStreet Pro and selected correspondences with my hedge fund investors at Seabreeze Partners.

God's Plan

Skepticism and doubt have left Wall Street.

To learn from history it is helpful to go back in history.

“Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.”

- Warren Buffett, “God’s Plan” (November 1999)

The Oracle of Omaha delivered the above quote only a few months before the end of the dot-com boom. Arguably, it may apply to today’s markets.

Buffett’s warnings should have been heeded, as, by March, 2000, the Nasdaq made a seminal top and commenced on a sutherly route that would result in a -80% drawdown in that index.

Twenty eight years ago I wrote an editorial in Barron's, Kids Today — the zeitgeist today is similar to that 26 years ago near the end of the dot-com boom:

"Being over 40 years old has been a liability in the Bull Market of the 1990s. ... I want to be like Sheldon The Kid and the rest of the kids in the 1960s and 1990s — trading in and out and relentless buying all dips, paying 15x revenues for tech stocks, disregarding value and common sense — but I can't."

- Doug Kass, "Kids Today" editorial in Barron's, July 7, 1997

A decade later another vivid illustration of the acceptance of "God's Plan" was made in an infamous quote by Citigroup's former CEO Chuck Prince in July, 2007 — a few months before the Great Financial Crisis, which also led to an unprecedented market decline in percentage terms and in time:

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We're still dancing."

Voltaire said that “History never repeats itself. Man always does.”

I am blinded by a sense of history.

In both the Winter of 1999 and in the Summer of 2007 day traders and speculation ran amok and a rising market was an almost accepted part of the zeitgeist.

Conditions today are clearly much different than in 1999 and 2007 — today's market leaders are healthy/profitable companies with deep moats (and not companies with no or limited futures).

We don’t expect anywhere near the declines of 2000-03 or 2007-09. However, we do expect an extended period of substandard to negative returns — an ideal backdrop for a long/short hedge fund, like Seabreeze, that is comfortable with a short book.

Investors face a host of secular headwinds that could be more long lasting than even at prior market peaks — the most important of which are:

* A rising probability of "slugflation" (prickly inflation, disappointing economic growth)

Prickly Inflation: Despite the slowdown in the domestic economy, recent reports suggest a possible reacceleration in the rate of growth of inflation. Tariffs will not help in the time ahead. (See my comment on tariffs later on in today’s commentary)

An acquaintance made some good points to me over the weekend (edited):

To put Fed 2.0% inflation target in proper perspective, to reach 2.0% inflation is not reality.

From 1965 to 2024 inflation averaged 3.9%. The last time inflation was generally low and not due to a crisis of some kind was the sixties. It was 1.6% in 1965 when the economy was booming at 6.5% GDP growth. Then again in 1986 as Fed Chair Volcker was coming to the end of his inflation crushing interest rate program, so not a normal period. In 1998 it was 1.6% when the economy was doing well and there was a trove of new technology being introduced which helped improve productivity. GDP grew at 4.2% real growth. Then from the period of the GFC 2009-2016 it was under 2.0%. But again, that was a very unusual period of financial market meltdown and grave financial crisis when the banks and Wall Street were essentially out of the market. Then in 2002, right after 9-11, so again, not a normal period. If we look for periods comparable to today when inflation was 2.0%, there are almost zero. We must ask where did this 2.0% target for the Fed come from and how did that number become the gospel. Achieving it based on history is not realistic. Perhaps the entire premise the Fed is operating under of needing to reach 2.0% is a fantasy that is unlikely to be achievable so long as the economy is growing. It would only be achievable if there is a deep recession or another financial crisis like 2009. 3.0% is a realistic target and we are there now with PCE at 2.6%, so rates should come down.

Possibly we can have 2.0% inflation someday once AI is much more widespread and productivity is even higher than today and GDP is growing at 4.0%. But we are not there now and with tariffs we are not going there anytime soon.

Many recall the Humphrey-Hawkins Full Employment and Balanced Growth Act of 1978 – a landmark legislation designed to address unemployment and promote economic stability. That bill set the goal for inflation to be at 4% by 1988. The lesson was that Congress cannot set inflation rates just as these rates cannot be legislated today.

Disappointing Economic Growth: All traditional signposts (labor reports, ISMs, etc.) point to a slowing U.S. economy and a challenge to the wrong-sided bullish notions that macro-U.S. data is resilient, S&P EPS growth will be robust and the trade war rhetoric is improving.

I won’t repeat the multiple macroeconomic and company/sector examples of a growing slowdown but I would add something that I have found to be one of the best predictors of growth — Las Vegas tourism. And, on that score, we should also be cautious on a consumer-based economy.

The consumer is spent up, not pent up.

(We have numerous consumer sector shorts in our Seabreeze portfolio).

Representatively, this is from Colgate-Palmolive’s CL 3Q2025 EPS release (hat tip Peter Boockvar). Colgate makes things we use every day like toothpaste, deodorant, soap, and shampoo.

"There is a persistently cautious consumer in North America right now. We saw some rebound in April, May. The categories took a little step back in June, which we weren't expecting."

"Many of our markets and categories around the world remained challenging in the second quarter and we expect this to continue through the second half of the year."

"The cost environment is difficult as we're dealing with tariff increases, higher raw and packaging material costs, and less underlying category inflation. This means that our revenue growth management strategies need to drive additional pricing and mix with lower levels of elasticity as we look to improve organic sales growth in the second half of the year."

* The rate of corporate profit growth will markedly decelerate in this year’s second half

* Undisciplined fiscal policy by both parties that will likely lead to a continued and large deficit, adding to our nation's debt load

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits — creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor"

* Equities are overpriced against interest rates: The equity risk premium is at a two-decade low — typically consistent with a slide in equities. (Given the plethora of uncertainties (many of them adverse), risk premiums should be rising, not falling!) The S&P dividend yield is at a near record low of 1.27% — and the spread between the dividend yield and the 10-year U.S. Treasury note yield has rarely been as wide.

* Valuations that are in the 98%-tile, a poor launching pad for future investment returns: The S&P Index’s trailing P/E multiple now stands at 26x — taking out the 23x peak of late 2021 and similar to the valuation reached in August 2000 (right before a two-year bear market commenced). The current multiple is more than +30% above the long-run norm. This is even more disquieting in that the real risk-free interest rate (at more than two percent) is double the historical average.

Tariffs: Changing Goal Posts

Over the last few weeks the markets have been buoyed by, among other factors, the Trump administration's "tariff" agreements which have been viewed by market participants as a big net investment positive.

We strongly are of the view that tariffs represent a bonafide threat to economic growth.

Most recently, the energetic reaction to a series of economically unfriendly tariff announcements and "agreements" are an exclamation point of unbridled and, arguably, poorly analyzed blind political and market enthusiasm. Moreover, the goal posts have been constantly been moved (in attempts to represent tariff policy success).

From John Mauldin ( "Thoughts From The Front Line) over the weekend in "Uncertainties Squared" Uncertainty Squared - Mauldin Economics:

“I know very few bullish investors who think tariffs are good. Mostly, they see tariffs as the “least bad” response to an intolerable situation. They recognize the ill effects but believe the tariff pain will end soon. (More on that below.) In this view, the current confusion and chaos will lead to a new equilibrium that is manageable and maybe even positive. They don’t think it will be bad enough to derail the other bullish factors like AI technology. If that’s what you believe, then it makes sense to take advantage of current bearishness to buy more. I’m not in that group but I understand their thinking. What I don’t see is reason to think the tariffs lead to even a neutral outcome, much less a good one. I’ve gone over the reasons before and won’t repeat them now. (Read this if you’re interested. It is my letter from April 25 and realize how much change there has been since then. Rather astonishing, really.)The best case I can imagine is that tariffs will raise import prices for American consumers enough to show up as higher inflation but not enough to trigger a recession. Because I think even 2% inflation is too high and robs all of us, I don’t see that as a good trade-off. Further, the way all this is being done makes the hoped-for manufacturing revival more difficult in reality than it is in the theory that some political types believe. I would also note that bulls keep moving the goal posts. Stocks rallied back from their April crash because Trump postponed the highest tariff rates for 90 days, during which he was going to negotiate a bunch of great deals with our top trading partners. The 90 days passed with no significant deals. Now we are told higher rates are coming in August, but traders seem to think those rates won’t happen, either. Maybe they’re right. But other governments are planning their retaliatory moves, and this could easily spiral into a broader trade war. Hopefully cooler heads will prevail, and we won’t end up with a repeat of the spiraling Smoot-Hawley tariffs. I get the idea of “seeing through” short-term volatility. My problem is with the “short-term” part. I just don’t see the finish line. I assume one is out there. I don’t think it is near.”

The unjustified bows taken by the current administration were recently outlined in The Financial Times:

“Anyone surprised by this? Thinking equities will keep going up once the great negotiator finishes the most amazing beautiful deals with Europe and others might be in for a rude awakening.

“I just signed the largest trade deal in history, I think maybe the largest deal in history, with Japan,” Trump boasted Tuesday. But a new report from The Financial Times demonstrates that U.S. and Japanese officials don’t see eye to eye on what exactly the countries agreed upon.

According to Trump and his administration, in return for a reduction in tariffs, Japan would invest $550 billion in certain U.S. sectors and give the United States 90% of the profits.

Japanese officials, however, say the profit sharing isn’t so set in stone: A Friday slideshow presentation in Japan’s Cabinet Office, contra the White House, said profit distribution would be “based on the degree of contribution and risk taken by each party,” according to The Financial Times.

The FT also reports conflicting messages between Washington and Tokyo as to whether that $550 billion commitment is, as team Trump sees it, a guarantee or, as Japan’s negotiator Ryosei Akazawa sees it, an upper limit and not “a target or commitment.”

Mireya Solís, a senior fellow at the Brookings Institution, told The Financial Times that the deal contains “nothing inspiring,” and that “both sides made promises that we can’t be sure will be kept” and “there are no guarantees on what the actual level of investments from Japan will be.”

The inconsistent interpretations of the deal could be because it was hastily pulled together over the course of an hour and 10 minutes between Trump and Akazawa on Tuesday, according to the FT, which cited “officials familiar with the U.S.-Japan talks.” And, moreover, “Japanese officials said there was no written agreement with Washington—and no legally binding one would be drawn up.”

Does Trump’s so-called “largest deal in history” even count as a deal at all? Brad Setser, senior fellow at the Council on Foreign Relations,

Another New Threat

“Well-nigh two thousand years and not a single new god!”

- Fredrich Nietzsche, The Antichrist (1888)

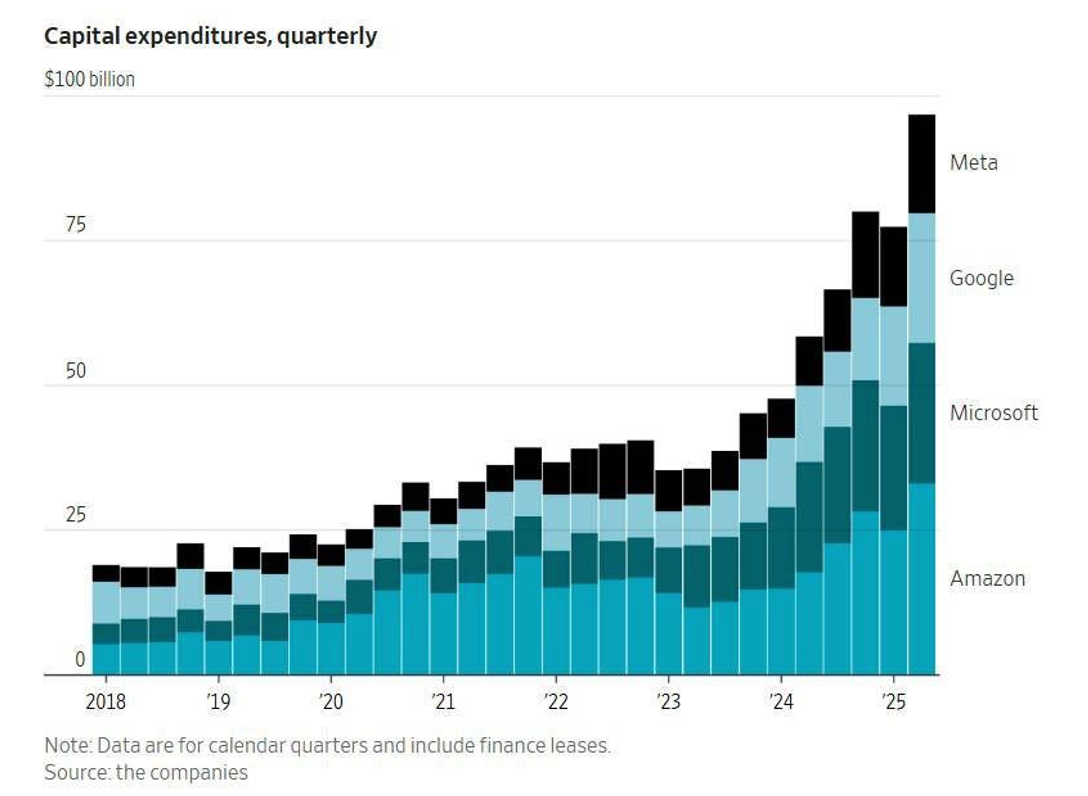

Another possible threat has emerged — the investing world almost universally believes it has discovered a new god in artificial intelligence and machine learning.

In dollar terms the AI outlays eclipse anything in history — with the four hyperscalers (Google GOOGL, Meta META, Amazon AMZN and Microsoft MSFT) undertaking a spending orgy by committing almost 60% of their 2025 cash flows (approximately $300 billion in 2025) on AI capital spending.

Putting this into perspective, AI infrastructure CAPEX is already 20% higher as a % of GDP than what was spent on telecom and internet infrastructure at the peak of the dot com boom. For Microsoft and Meta, CAPEX is now more than a third of their total sales. Astonishingly and according to Neil Dutta (head of economic research at Renaissance Macro Research), capital spending for AI contributed more to growth in the U.S. economy in the past two quarters than all of consumer spending.

The depreciation schedules being used for this AI spend is somewhere between aggressive and absurd. One company, CoreWeave CRWV, is reporting earnings before capital expenses!

I share the following concerns expressed over the weekend by The Credit Strategist:

“Anyone who questions AI faces the challenge of answering technology experts (genuine and self-proclaimed) who claim superior knowledge of the topic. But the projections on which future AI revenues and profits are based remain highly speculative because they are based on events that have yet to happen; put bluntly, they are based on predictions about the future that is always unknowable. But one characteristic of the future that is knowable is that it is reflexive, meaning human beings and organizations react and adjust to changes rather than remain static. As such, arguments that AI will eliminate jobs without creating new ones or arbitrage away margins without creating new margin opportunities are questionable. Further, it is unlikely that multiple LLM models addressing the same market will all prove successful; more likely, ruthless competition will create a small group of winners and many losers with a great deal of capital consumed in the process.

The quantum of AI spending dwarfs anything previously applied to a specific product or sector in such a concentrated period of time. All of this spending has yet to produce a commensurate amount of revenue or profit but we are still in early days and investors are convinced that it will. Whether the world needs numerous LLMs that perform similar tasks remains to be seen; it’s not clear that these models can meaningfully differentiate themselves despite spending hundreds of billions of dollars attempting to do so. As Fred Hickey writes in The High Tech Strategist (highly recommended): “revenue generation for the LLM builders is limited (they’ve not found killer apps for the masses) and the losses are unlimited. The capex would be destroying their company P&Ls – except for the fact that the chips and equipment costs are spread out over several years via depreciation expensing.” The fight for dominance and first-user advantage will continue to the bitter end. Some are projecting that annual AI spending could increase even further but I suspect it may end up tapering off if it doesn’t generate promised returns before long.”

To summarize, while Mag 7 and AI-related equities have dominated the market’s advance and participants’ attention over the last two years, AI has yet to demonstrate it will save the world. Any change in attitude towards these companies could send markets reeling lower.

Bottom Line

S&P 500 Index over past 4 years

We see numerous cracks in forward-looking global economic fundamentals, an unclear path of U.S. corporate profits, coupled with extended valuations (both absolutely and relative to interest rates).

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass was short SPY common (M) and calls (VS), QQQ common (M) and calls (VS), PLTR (VS).