Doug Kass: The Sugar High Is Over

I'm bearish as, so far, my views for the market in 2025 are playing out as expected.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Back in early March, I wrote the following, in which I said I expected we were on the path for a 10%-15% Decline in 2025:

"Since mid-February, equities have begun to roll over. This is consistent with my expectation that January 2025 may mark the top in equities, which have been led by large-cap tech and the Magnificent Seven — for the year. I see this phenomena as also analogous with the January 1973 peak in the broader market and the end to The Nifty Fifty leadership/dominance and cycle)."

Remember, we entered 2025 on a sugar high. Investor optimism abounded while a steady deterioration in domestic economic activity and stubborn inflation -- "slugflation" -- were ignored in the face of emerging animal spirits.

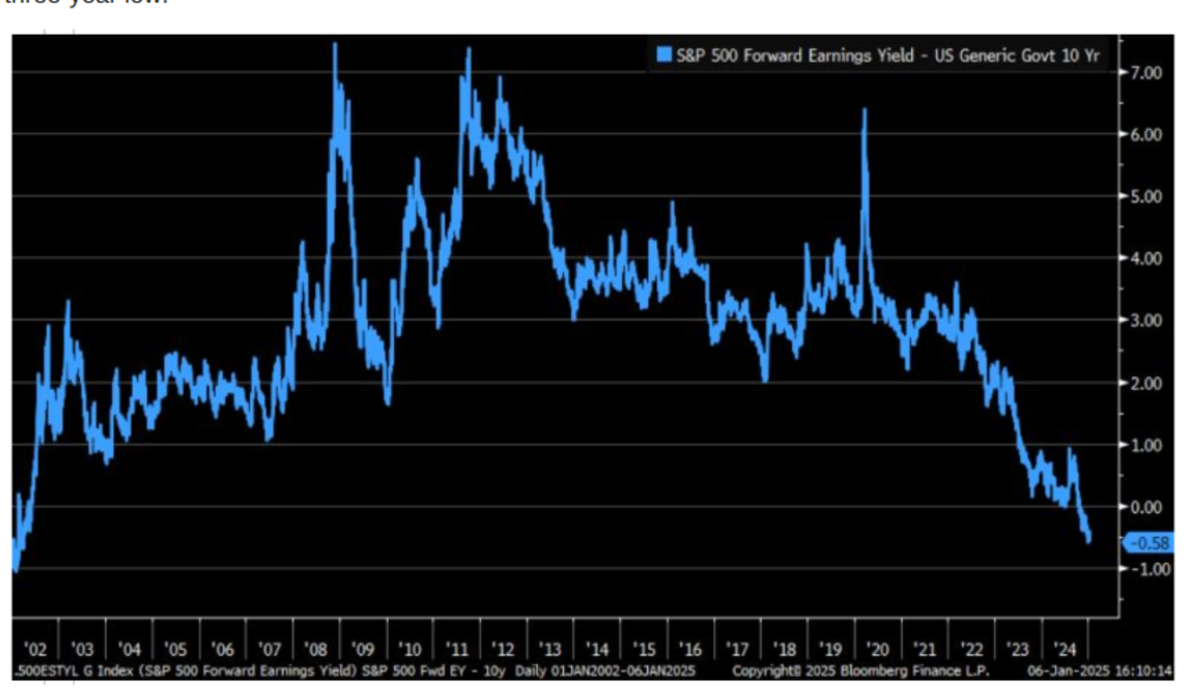

Importantly, the increase in interest rates and the decline in the corporate-profit outlook contributed to an ever-thinning but disregarded equity risk premium. The spread between the S&P 500 Index's forward-earnings yield and the 10-year Treasury yield recently reached a 23-year low. (What was initially seen as 14% S&P earnings per share growth (2025 over 2024) now appears to be only +7% to +8%). Check out the chart below:

Investors at the start of the year also paid no regard to questionable and unpredictable fiscal and monetary policies led to a herd-like FOMO (fear of missing out) and a continued and spirited climb in equity prices. These policy risks were put on the back burner as animal spirits were abetted by historically aggressive company buybacks -- over $1 trillion in 2024 -- and massive equity fund inflows (also over $1 trillion in 2024).

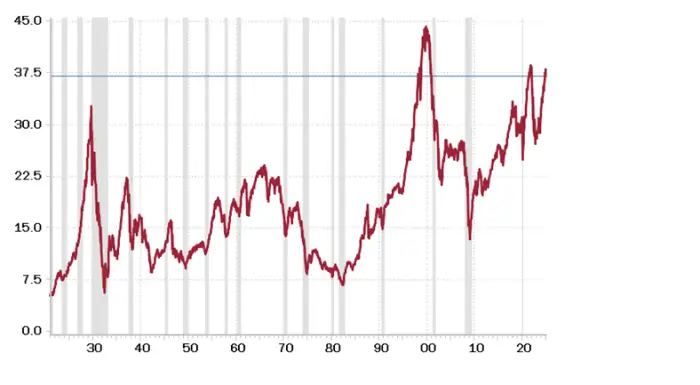

Valuations, which soared to an over 95%-tile by most traditional metrics and measures, were also ignored.

But Ignorance May Not Be Bliss

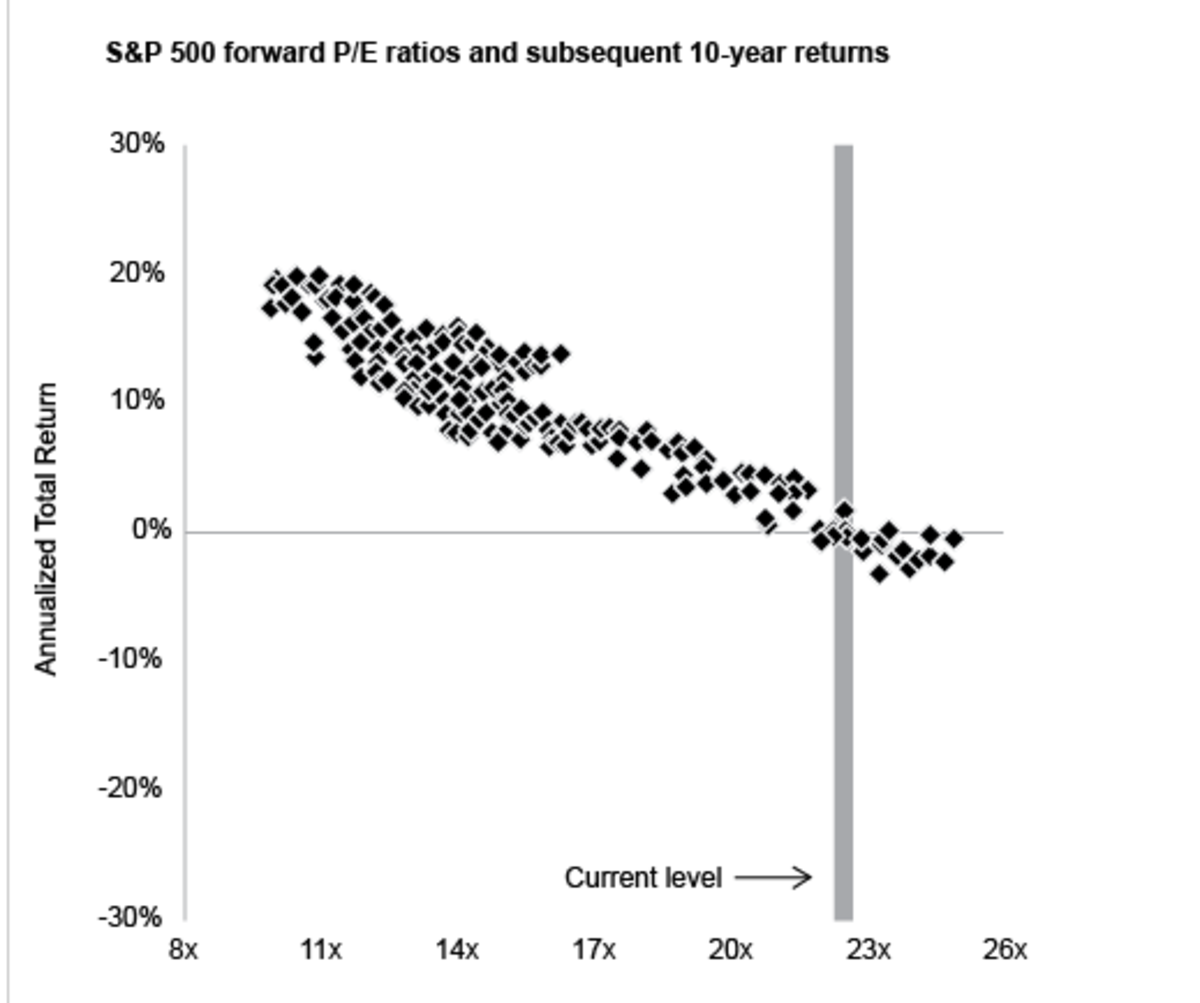

Historically, such a high cyclically adjusted price-to-earnings ratio multiple is a launching pad for inferior returns. Check out this chart of S&P 500 forward price-to-earnings ratios and subsequent returns over the decade following:

Source: J.P. Morgan Asset Management

Market Performance for 2025 Has Grown More Problematic and Cloudy

Thus far this year, the markets have conformed to most of the elements of my full year outlook.

Here were my baseline expectations as we entered this year (three months ago):

- The S&P Index will likely decline this year, with a small double-digit percentage drop as a base case.

- The upside of the S&P Index will be approximately +5%. (At its peak in late January, the senior Index was up by nearly +4.0%)

- The downside of the S&P Index will be about -10% to -15%. (The S&P Index is currently -3.5%).

- The S&P Index might make its yearly high during the first month of the year (January).

- Importantly, the league-leading Mag7 will likely begin a lengthy decline in January 2025 (similar to the top in the Nifty Fifty in January 1973). Here's what I wrote earlier on this topic:

- Looking at the near term, the recent low in the S&P Index from about a week ago would likely be followed by a three-to-six day contra rally that could fail (similar to 2018) at around the 200-day moving average:

- We see the overall decline in the S&P Index from January 2025 as likely to be characterized by a saw-toothed pattern (see my Diary entry in the TheStreet Pro) a slow but steady and undramatic fall.

So far, my 2025 forecasts seem to have been correct.

Stay tuned, fingers crossed.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.