Doug Kass: The 'Happy Meals' Won't Last Forever

Let's look at how history repeats itself, some lessons from McDonald's past and the wise words of Einstein and ... Deemer.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What follows is a combination of my recent correspondences with Seabreeze Partners' investors and timely articles I have written on TheStreet Pro. As I make my points about the market -- including that when the time comes to buy, investors won't want to -- I will quote the wise words of Yogi Berra, Albert Einstein, Warren Buffett, Howard Marks, Larry Fink, David Rosenberg, Voltaire, Jean-Jacques Rousseau, George Orwell, Franklin D. Roosevelt and (last but not least!) Wally Deemer.

Valuations: Excessive to Pornographic

In my hedge fund, we remain slightly net short in exposure (out of respect for the stock market's upward momentum) but plan to add to that exposure if our fundamental concerns appear to be developing (and if stock price action begins to confirm my ursine outlook).

Investors Don't Buy Companies, They Buy Stocks

The equity of a company is fundamentally a claim on assets - representing the residual value of an asset or business after all liabilities are paid off. This is the shareholder's stake, a "leftover" amount in the accounting equation:

Assets - Liabilities = Equity

Calculating shareholders' equity or what truly belongs to a holder of equity is relatively easy to compute and is objective.

What is more difficult, however, is what that equity is worth - this is the subjective part of investing.

This is where my hedge fund, Seabreeze Partners, disagrees with the consensus - we question what the multiplier should be on earnings.

A Stock Is Not the Same as a Company

- Wally Deemer, Introduction to his new book When the Time Comes to Buy You Won't Want To (Volume II)

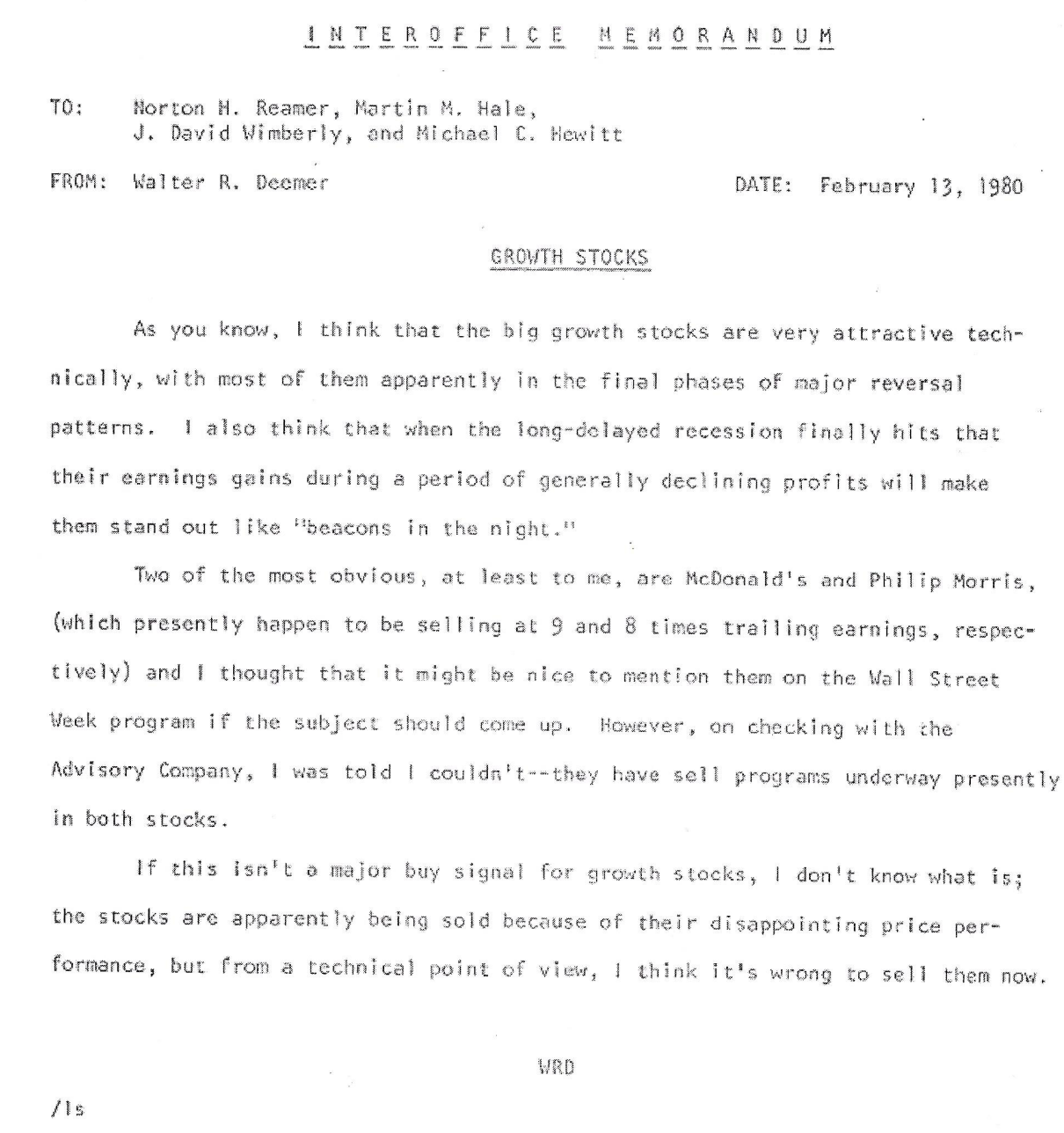

The investment mosaic is so much more complicated than simply taking an S&P profit expectation and multiplying it by a multiple — as Wally Deemer's extreme example of McDonalds' (MCD) share price performance during and after the collapse of The Nifty Fifty era (1972-1980) shows.

The share price of McDonald's during the decade of the 1970s (when I was at Putnam Management Company) provides a vivid and extreme blueprint of a market (and consensus) being very wrong about the value accorded one of the most popular stocks. This illustration will better explain why we see as the risks associated with currently elevated valuations.

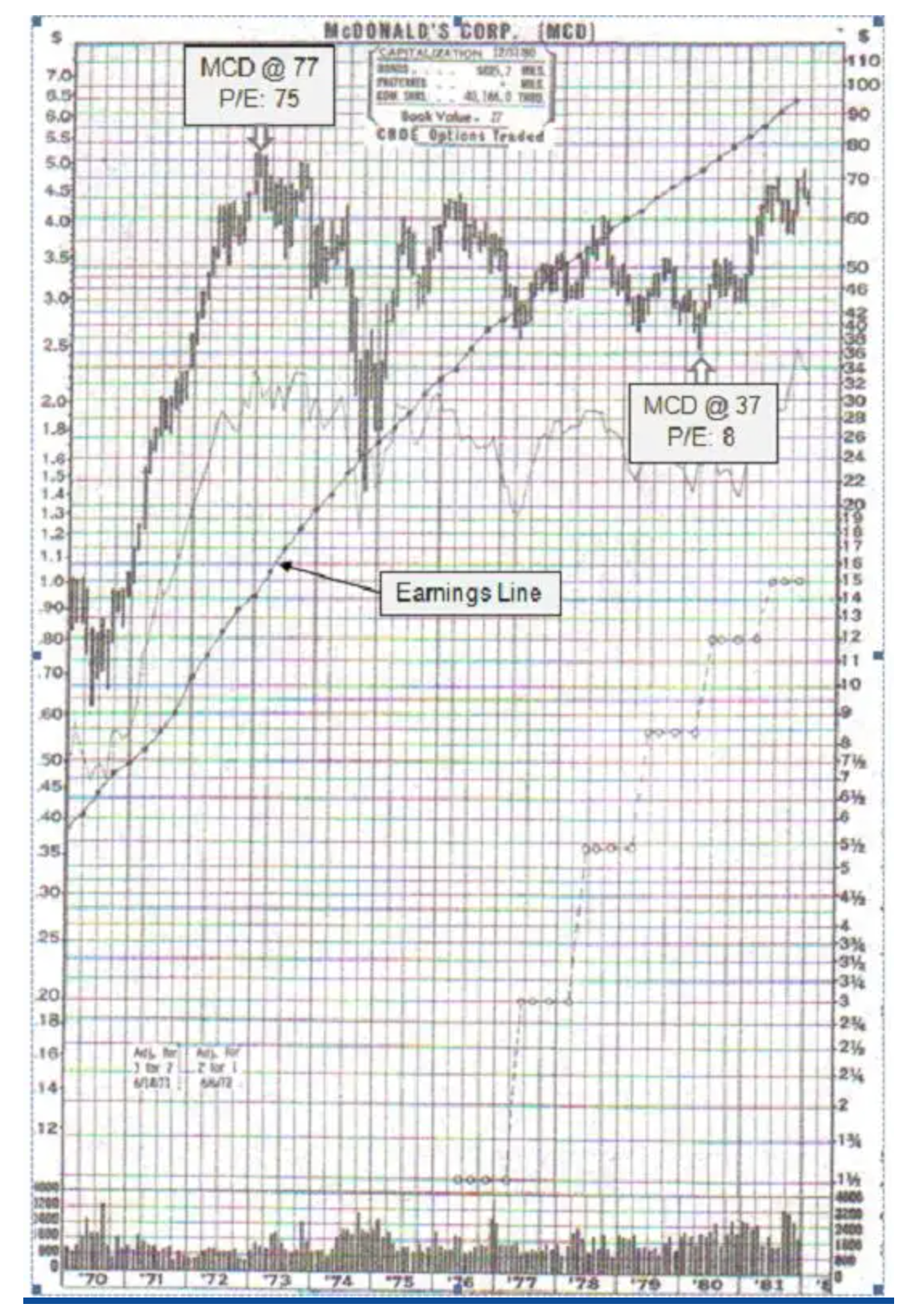

From 1972-1980, McDonald’s growth in earnings per share compounded by an extraordinary 25% per year. Yet, its price-to-earnings ratio dropped from 75-times to only 9-times and its share price declined by more than -50%!

- Wally Deemer, When The Time Comes to Buy You Won't Want To (Volume II)

Here is a memo from Wally (my associate at Putnam) in 1980:

And here is the McDonald's chart from the 1970s:

While the S&P Index is not anywhere as overvalued as McDonald's was in 1972 (when MCD possessed a 75-times price earnings multiple), as noted previously, we believe the markets are materially overpriced at current valuations.

We see a Bull Market in Group Stink with a herd-like chorus of "first level thinking" at a near unanimous pitch and adoption today – somewhat like the peak in “The Nifty Fifty” so clearly expressed by a 77-times multiple in McDonald's' stock price in 1972.

To paraphrase Wally, when it’s time to sell (McDonalds in 1972) or perhaps the S&P Index in 2026, investors won't want to....

Repeating My Fundamental Concerns

"We have now sunk to a depth at which restatement of the obvious is the first duty of intelligent men."

- George Orwell

Seabreeze is slightly net short for the multitude of reasons mentioned in our previous commentary to investors and on TheStreetPro:

* We reject the generally positive consensus expectations for U.S. economic growth:

"We have learned that we cannot live alone, at peace: that our own well-being is dependent on the well-being of other nations far away. We have learned that we must live as men, not as ostriches, nor as dogs in the manger. "

- Franklin D. Roosevelt

Increasingly (and importantly), errant Administration policy could begin to adversely impact economic alliances and contribute to a downturn in global economic activity.

Domestically, we believe there is a growing possibility that the current K-shaped economy's weakness in the lower income cohort spreads into the middle and upper middle class as the cumulative (or stacked) inflation since Covid finally has an impact — causing a spending freeze. With the outlook for global economic growth dissipating, consumer and business sentiment could plummet. BNPL (buy now pay later) and credit defaults would then rise and auto repossessions could increase dramatically.

Drawdowns in the global equity markets and a still moribund housing market may contribute to a negative "wealth effect" and an air pocket with the high end consumer as investor optimism of 2023-25 is abandoned.

* We also reject the notion that the new Fed Chair will grease the economy (and run it "hot") by lowering interest rates. We disagree on several counts: we see inflation remaining sticky and we don't think the new Chair will have a cooperative Committee.

* The equity risk premium — which has historically been an excellent forecaster of future equity returns — is now a discount. This means that the market is pricing more risk in bonds than in stocks!

* Historical valuation metrics are at about the 97%-tile. Indicators like the Buffett Ratio, Shiller CAPE and Price/Sales are at all-time overvalued readings. We strongly disagree with the many investors who believe we are in a new valuation paradigm. From Howard Marks:

* Dividends typically account for a bit more than 35% of the total return of stocks. The S&P Dividend Yield is now at a multi-decade low of 1.12% — contributions from dividends are modest — likely leading to substandard returns for an extended period of time.

* The composition of equity returns remains out of balance with a small number of large-cap technology stocks (highly dependent on the AI trade) contributing to overall returns. As noted in 170 "More Tales From Nvidia" columns, I am far less optimistic regarding the overall value of and return on investment prospects for the outsized AI capital expenditures - for society and as it relates to the productivity of individual companies.

* Margin debt, like valuations, is at a record high — inflating the indexes by borrowed money. Any reversal in market sentiment could trigger an unwind of this leverage, which could cascade in a market dominated by passive products and strategies that worship at the altar of price and momentum. The recent unwind in the leveraged cryptocurrency markets might foreshadow what may happen in equities in 2026.

* Neither political party is acting in a fiscally responsible manner. A feckless approach to our deficit is producing a steady march higher in our national debt:

* I recently mentioned reading my friend Andrew Ross Sorkin's new book 1929: Inside the Greatest Crash in Wall Street History-and How It Shattered a Nation.

I couldn't help but see the similarities between then and now. The 1920s did not end well as our society lost sight of the value of regulations: wise rules are a source of abundance, well-regulated markets/systems attract users and investors, removing the constables patrolling our financial markets is potentially dangerous and U.S. capital markets became the world's largest not despite regulation, but because of it.

* There are large risks associated with (leveraged) passive products and strategies, the proliferation of ETFs (today there are more ETFs than individual stock listings!), changes in market structure and in a leveraged crypto currency investing base. The gamification of the market is being ignored and is not being addressed by market participants and by regulators. (It is abnormal and symptomatic to the degree of speculation going on today that 70% of all options traded have only a 24-hour maturity!)

* Wall Street strategists are unanimously bullish - on average they are forecasting a +11% return for 2026. They are nearly always bullish, so their opinions should be taken accordingly — and with a grain of salt. We believe they are failing to consider the growing list of negatives....

The Future Ain't What It Used To Be

"I must seem like an ostrich who forever buries its head in the relativistic sands in order not to face the evil quanta."

- Albert Einstein

A famous philosopher, baseball player Yogi Berra famously once said that "the future ain't what it used to be."

As I noted in a recent monthly commentary to Seabreeze's limited partners - Warren Buffett warned about a too ebullient mindset in November 1999, only four months before the dot.com bubble burst:

Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.

Voltaire also put it well when he wrote:

"History never repeats itself. Man always does."

Delusions swing between extremes, like pendulums. Delusions of grandeur and unending wealth give place to delusions of unending gloom. One is as unreal as the other. Today we seem to be close to an extreme in speculative activity and valuations. Unfortunately, history teaches us that the unsustainable cannot be sustained as, ultimately, with panic and pain, bubbles burst.

When I look at today's valuations I am reminded of (a twist) of something written by Jean-Jacques Rousseau:

"History never deceives us; it is we who deceive ourselves."

For what we have learned from history is that we haven't learned from history.

In summary, perhaps the S&P Index in 2026 has some resemblance to McDonald's share price overvaluation in 1972 — when a top was made in McDonald's (and investors were willing to pay 75-times earnings per share). At that time (like today), everyone was all in the investing pool in the belief that equities were a buy on every dip and would never fall.

While we certainly don't think that today's stock market is as extremely overvalued as McDonald's was 53 years ago, there is a message in the comparison (and a twist of Wally Deemer's mantra):

"When the time comes to sell, most won't want to."

At the time of publication, Kass had no position in any security mentioned.