Doug Kass: Market's on Path for 10%-15% Decline in 2025

We see this year as unlike 2024 and more like the 1973 peak and end of Nifty Fifty dominance.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Since mid-February, equities have begun to roll over. This is consistent with my expectation that January 2025 may mark the top in equities which have been led by large-cap tech and the Magnificent Seven — for the year. I see this phenomena as also analogous with the January 1973 peak in the broader market and the end to The Nifty Fifty leadership/dominance and cycle).

The weeks' long rotation away from large-cap tech and away from the Magnificent 7 stocks is growing more conspicuous. Through Tuesday, the Mag 7 is down 10% year-to-date. Put another way, it's double the decline of the Nasdaq Index and compared to only a couple percentage point drop in the S&P 500 Index.

I believe the market is on a path — more or less — for a 10%-15% decline this year.

The expected downturn will not likely come in a straight line. It is my view that machines and algos will exaggerate moves up and down, contributing to a sawtooth pattern lower. While not meant to be precise and possibly I'm wrong, this is my baseline expectation upon which I tactically manage my hedge fund, Seabreeze Partners.

Responding to the market selloff, fear and negative investor sentiment has risen over the last few weeks: See the Fear and Greed Index - Investor Sentiment | CNN.

With seven out of the last eight days lower for the S&P Index, the CNN Fear & Greed Index highlighting "Extreme Fear", the S&P Short Range Oscillator moving to a deeper oversold (-5.12%) and the S&P Index hitting (at their nadir Tuesday morning) an important support line. I was not surprised (and I took a small trading long rental in the Indexes) that stocks exhibited a powerful reversal higher Tuesday afternoon (and in stock futures this morning):

I do not expect the recovery in stocks (seen in the last 12 hours) to be long lasting or the start of another leg in the bull market that we have witnessed over the last two years.

My multiple concerns are now well known. These include stubborn inflation and sluggish economic growth ("slugflation"), fiscal and monetary policy risks, elevated valuations, and rising geopolitical threats.

We can now add the Trump administration's agenda and policy impact on inflation, economic growth and the Federal Reserve's policy decisions to the list. Specifically, I am concerned about the poorly thought out and current implementation of tariffs, which will serve to raise prices, slow economic activity, increase unemployment, worsen inequality, diminish productivity and raise global tensions.

I am fearful that the lack of predictability of current economic (and tariff) policy, in and of itself, may contribute to delayed capital and consumer spending — and even slower economic growth than I currently anticipate.

Finally, as noted in the nearly 70 columns in my "More Tales From Nvidia" series since June 2024, I expect capital spending on artificial intelligence to go through a digestive phase this year. So, with their outsized market weightings, the averages will likely be adversely impacted. Already six of the seven Mag 7 companies have reduced first-quarter 2025 revenue guidance. I anticipate cuts in Mag 7 earnings per share estimates for the second half of 2025.

Here is a mid-February recap of my 2025 market outlook:

What Goes Up May Come Down

* Updating my market outlook...

What goes up must come down

Spinning Wheel got to go 'round

Talkin' 'bout your troubles

It's a cryin' sin

Ride a painted pony

Let the Spinning Wheel spin

You got no money, you got no home

Spinning Wheel all alone

Talkin' 'bout your troubles and you

You never learn

Ride a painted pony

Let the Spinning Wheel turn

- Blood, Sweat and Tears, Spinning Wheel

I continue to be deeply skeptical of the market's advance and I am maintaining our cautious investment strategy in the belief that equities are braced for a decline this year.

We believe that we are close to 2025's high in the averages and that downside is now roughly 3x the upside.

Investors should now be fearful of the excessive market optimism.

Nine days before the 1929 stock market crash that led to the Great Depression, Dr. Irving Fisher, an economist at Yale University, famously said (at the Purchasing Agents Association Dinner in New York City):

“Stock prices have reached what looks like a permanently high plateau.”

Fisher's prediction is considered one of the most notorious stock market forecasts of all time. The market's crash cost Fisher much of his wealth as well as his academic reputation.

Coincident with two back-to-back +20% annual returns in the S&P Index, a developing and confident bullish market narrative has emerged — which is eerily reminiscent of Dr. Fisher's 1929 comments:

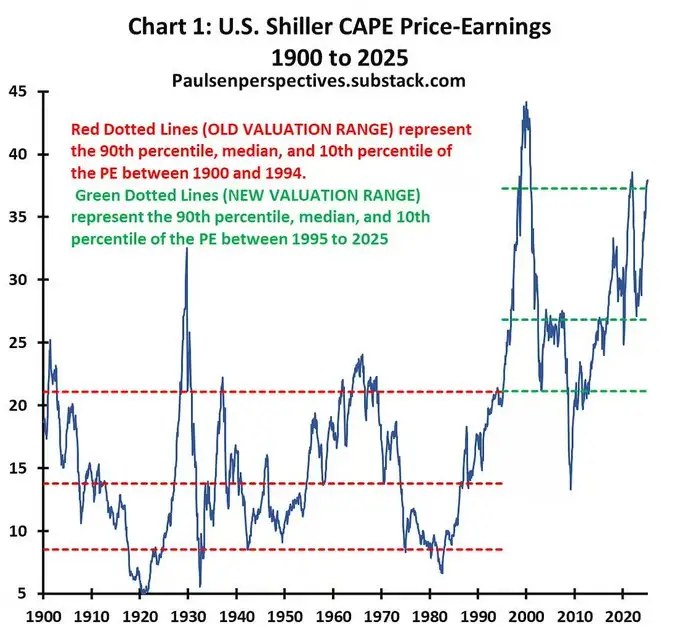

"Increasingly, at least from my perspective, the U.S. stock market's new valuation range (after 30 years its probably misleading to continue calling it new) appears to be permanent."

- The Daily Chartbook

Despite the near universal optimism in investor sentiment (as expressed in historically low cash reserves and most classical metrics and valuations above the 95% tile) there are rarely new eras — excesses are never permanent.

As noted last month, I remain of the view that we are not in a new (and permanently high) valuation paradigm for equities and that an important top in the U.S. stock market may be close at hand:

December marked the beginning of what we expect to be a lower-trending market accompanied by rising volatility.

We expect 2025 to look far different than 2024.

While we predominantly focus on an assessment of reward vs risk on individual stocks — if we were forced to hazard a precise forecast we would project only about a five percent upside and a ten to fifteen percent downside for the S&P 500 Index in 2025.

Today's commentary will explain why heady valuations are rarely a good launching pad for higher stock prices.

We will explore and summarize some of our fundamental near and intermediate-term concerns.

We will compare today with early 1973 (which marked the end of the Nifty Fifty era) and produced years of subpar returns for the major market averages. Then, we will highlight some longer-term existential market threats that few discuss, but that have a reasonable chance of emerging.

Finally, we will explain why the numerous uncertainties and headwinds provide a fertile basis for investors to prosper (absolutely and on a relative basis) in searching for asymmetric investment opportunities — and why a top-heavy, technology-led market (which has not broadened) has already begun to deliver some developing long opportunities with upside rewards that dwarf downside risks.

As I also recently wrote:

Many of our fundamental concerns (growing policy (fiscal and monetary) risks, sticky inflation, slowing economic growth and rising interest (higher for longer)) are finally beginning to be accepted by investors — at a point in time in which valuations are elevated and consensus corporate profit estimates seem too optimistic. We are increasingly more confident that stocks will correct to more attractive levels than exist right now — at which time we can begin to accumulate selected stocks that meet our investing criteria and standards.

Bottom Line

To sum things up, I believe the general lack of "predictability" in policy (and in turn, economic growth) is rising and I continue to expect this year's market to be much different from last year's market. In fact, downside market risk looks to me to be roughly twice to three times upside market reward. I still see the 2025 forecast for a 10% to 15% drop in the S&P Index as intact.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass was long SPY common (M), QQQ common (M); short SPY calls, QQQ calls (M).