Doug Kass: I'll Consider the Bullish Case. And Then I'll Pick It Apart

Here I'll lay out the current consensus bullish arguments that could continue to buoy valuations, and then I'll give my take on each.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Investors are now almost universally bullish. However, during the past month, I have argued that investors are overly positive. I outlined much of this in my post, The Bull Market in Complacency Is Alive and Well land Living on Wall Street. But here is a partial list of my continuing concerns, as we face the:

- Highest geopolitical risks in many decades (which will not be resolved quickly).

- Largest level of social and political risks in the U.S. since the Vietnam war.

- Greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

- Biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

- Greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsoever.

- Largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot-com, it feels like deja vu all over again.) (More on this shortly.)

- Viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

At the suggestion of Oaktree's Howard Marks, I have made a list of what I believe to be the most significant and now consensus bullish arguments that could continue to buoy valuations. It's regardless of my ursine view. Note that I will follow each point with an explanation of why I differ with some of these arguments:

- There is a Fed Put: President Trump has announced that he will replace Fed Chairman Jerome Powell with a dove, leading to lower short-term interest rates.

The Fed now expects inflation to rise over the next few months, which is not an ideal setting for lower rates. A Fed Chair monitored and under the watchful eye of Pres. Trump will likely produce a more uncertain monetary policy. I am not sure that a Fed Chair (with a committee of Board of Governors) will be as closely influenced by a Fed chief that works close or is even at the beckon call of the President. The capital markets could grow quite worried (with a dependent and not independent Fed); American Exceptionalism might be threatened with the selling of our currency and bonds, especially if the inflationary backdrop grows more problematic. Institutional credibility and independence will be challenged in a very public (and market!) way. Finally, wasn't there a lesson to be learned in 2024 when a one-percentage point cut in the Fed Funds rate produced higher intermediate and longer term Treasury and mortgage rates? If this occurred, the equity risk premium would narrow ever more (with reduced S&P profits and higher risk free interest rates).

- The current Administration is pro business and economic growth and deregulation are the cornerstones of Trump policy.

Pres. Trump's "big, beautiful bill" incorporates the notion of spending cuts with economic incentives (skewed toward corporations and the wealthy). There could be a populist pushback in a consumer-led slowdown. Given the deteriorating state of the business and economic cycles the outcomes of pro business policy might be disappointing relative to expectations -- especially with the margin pressures of the evolution from globalism to nationalism.

- Geopolitical risks have been reduced with the recent aggressive attack against Iran's nuclear facilities.

Yes for now. But there remain potential regional hotbeds that represent bonafide threats.

- With a U.S. service economy expanding, recessions are no longer likely.

I would say recessions are not endangered. But a service economy will likely cushion the magnitude of economic downturns. This is a subject I addressed in Have Both Economic Cycles and Sentiment Surveys Become Less Relevant?. That said, AI could be threat to this theory of "stability," should a larger-than-expected displacement of jobs occur. The resumption of student loan repayments could further pressure personal expenditures. Also, as stated above, the shift from globalism to nationalism might prove to be a greater headwind to S&P earnings per share than the consensus expects.

- Corporate profits will grow steadily and above expectations over the balance of the year.

The rate of S&P EPS growth likely peaked in 1Q 2025. Who pays for higher tariffs, consumer or corporations? An estimated $400 billion of tariffs represent 20% of total corporate profits. Its a Sophie's Choice: The imposition of tariffs will likely deliver either higher inflation or lower corporate profits.

- While the budget deficit and U.S. debt load are well above expectations, they are not threats, as a rising budget/debt as a percentage of GDP has been in place for years.

DOGE failed and both sides of the political view lack fiscal discipline. I would argue that, with annual interest payments now in excess of the defense budget, we are closer to seeing the reemergence of the Bond Vigilantes than ever.

- AI will provide a fountain of corporate productivity, additive to revenues and profits.

Thus far the commercial applications and user sets of AI are minimal, though this will likely change. But, as I have also argued in "More Tales From Nvidia", it is unclear whether the trillions of dollars of capital investment (by the hyperscalers and others) will result in an adequate return on invested capital. Moreover, the AI trade started in 2023 and is almost three years old.

- Higher equities will deliver a wealth effect to the consumer and offset housing's weakness.

I agree that the consumer will benefit from a continuation of higher stock prices - but remember the S&P Index has simply returned to its late January/early February level. As to housing, the contraction is growing closer in focus and, given the disproportionate role of housing (it hits above the belt!) on consumer wealth, a drop in home prices could offset some of the wealth effect provided from the benefit from higher stock prices.

- American Exceptionalism is intact; if nothing else there is no alternative.

In Time To Rethink American Exceptionalism, I argue that the worm is turning. I agree to some extent, but I do believe that the recent trend away from investing in the U.S. will reduce domestic investments -- at the margin.

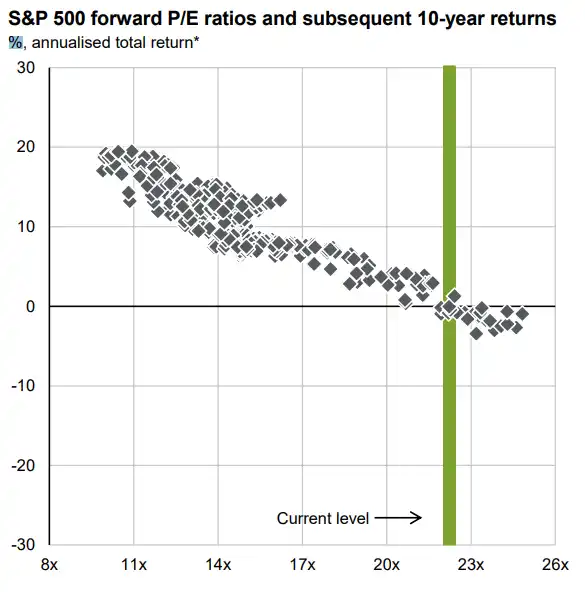

- Price earnings multiples (at 24-times) are inflated, but in past periods of speculation valuations have been even higher.

This is where I disagree strongly with the bullish cabal. Isn't this simply "the greater fool's theory," in which investors are relying on a greater fool to bale them out? This hasn't worked well in the past when valuations were excessive. As reflected in the illustration below, (historically speaking) current valuations are a poor launching point for future returns:

- The market's advance has been broadening out.

Yes, it has broadened out. But look at the lagging Russell Index, which has not been crowing. Let's keep a bead on market breadth in the weeks ahead.

- There is a massive build up in cash reserves that will flow back into equities.

The "cash on the sidelines" is as dumb as wood as an argument. First, cash should be looked at not in the absolute ($7 trillion), but as a percentage of stock market capitalization. As such, cash reserves are actually at the low end of history. Second, the maturation of the baby boomers suggests a lot of the cash is sticky (and being invested in equity-like returns now available in the fixed income markets).

- Market structure favors the bulls: The dominance of passive investing products and strategies has reduced "the float' of equities.

This is accurate. When combined with trillion dollar buybacks (yearly), a rising demand for stocks is being met with a diminished float. For now everyone is on the same side of of the boat. Of course, when the worm turns (and equity fund redemptions rise) -- and it will eventually -- the movie goes in reverse and there will be few buyers (I am old enough to remember when the S&P slipped to 4850 2.5 months ago as sellers overwhelmed buyers.

- There is a new generation of investors and speculators that will buoy equities.

(This is Jim Cramer's argument). As I explain the speculation may be more likely to end poorly than being sustained as Jim suggests.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no position in any security mentioned.