Doug Kass: Here's How I Handle Hostile Markets

What I think about trading in tough times, an update on my 'Seven Years' thesis and a review of my 2025 predictions.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What follows is a combination of Diary entries and recent communications with my Seabreeze investors. I will lay out my tactical strategies in dealing with hostile and volatile markets, let you know how I'm thinking and why, and, of course, update my market view. In addition, I will update my "Seven Years" thesis and review my 2025 predictions and how some of them are playing out so far.

Let's dig in:

Waiting For the Right Pitch

During the past 15 months, I have structured my Seabreeze Partnership's portfolio conservatively, with mostly pairs trades and modest net short exposure. While failing to expect the emergence of "animal spirits" contributing to large equity fund inflows and a rapid climb in stock prices in the past year, our fund's ability to generate positive investment returns (and not to incur losses) speaks volumes to disciplined risk management. Though embracing an admittedly wrong-footed and negative market outlook since early 2024, my fund has recorded profitable returns in 14 of the last 15 months. (My hedge fund's only monthly loss was a meager -0.22%.)

"The only certainty is that nothing is certain."

- Pliny The Elder

Looking further out, as I will discuss in today's commentary, my base case is for an extended period of substandard investment returns. As always, I might be proven wrong as I acknowledge the uncertainty of outcomes (see Pliny The Elder!). The factors that influence markets move ever faster these days! So, regardless of my current view, I will remain flexible and opportunistic. Remember, I am not Perma anything. I recognize that shorting stocks preserve capital but buying stocks generate wealth. Despite my intermediate-term market concerns, some sectors and individual securities have already entered value levels (with favorable upside reward vs downside risk) and I have raised our net long exposure to approximately 20%-25%. It seems increasingly probable that, over the next few months, stocks could fall to levels that will encourage me to further and more aggressively expand our net long exposure.

"The trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot. And if people are yelling, 'Swing, you bum!,' ignore them."

- Warren Buffett

While I will be patient and let stock prices "come to me." It is at that time that it will be time to generate wealth.

Many of My Concerns Are Now Being Realized

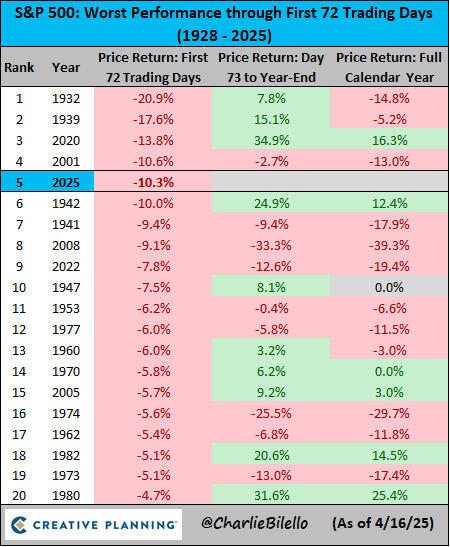

Since early 2024 I have repeatedly expressed a series of concerns regarding corporate profit and economic expectations and sticky inflation. I worried about fiscal and monetary policy mistakes and a paper-thin risk equity premium. I feared that extremely elevated stock market valuations were a poor launching pad for future stock prices. This year the markets have begun to recognize the validity of my concerns and stock prices have fallen. As of Friday the S&P Index is down by -10.3% in the first 72 trading days of 2025:

It got worse yesterday:

Before I restate the market headwinds I see, I will briefly explain why the backdrop of an extended period of non-trending stock prices -- somewhere between slightly higher to slightly lower stock prices (that behave in a volatile manner) -- is the ideal environment for a hedge fund, like Seabreeze, to prosper.

"I don't know how to predict the stock market, I don't know how to predict interest rates, I don't know how to predict business. All I know is if I buy the right kind of business at the right price with the right people I'll do well over time."

- Warren Buffett

Unlike most, I admit to being wrong at times and always in doubt -- that is why we manage your money with a calculator in hand. Having an analytical view of intrinsic values (see Buffett's quote above) and relying on "a margin of safety" keep our uncertainties checked. Let me start by noting that over the course of my investment career I have interviewed thousands of managements. Not surprisingly, not one management team ever expressed concerns about their companies' intermediate-term profit prospects. The same observation applies to money managers. Most asset gatherers state that they can deliver superior investment returns during all sorts of weather.

The reality of investment returns is different, though. Most asset/hedge fund managers only flourish when stocks rise and the tide is in. Few possess the ability to short stocks or to opportunistically capitalize on market volatility by trading unemotionally (and "ringing the cash register") in a period of expanding volatility - when stocks fall and the tides goes out. What makes those opportunities even greater today (than in the past) is the dominance of passive and momentum-based quant trading (like risk parity) that know everything about price and nothing about value. Over history, given my investing style I typically trail rapidly rising markets, but I thrive and differentiate my performance when markets rise slightly, are flat or are down (as I did in 2022, when I delivered positive returns as the major indices dropped by -20%). As I have written in the past, and with a hat tip from Lee Cooperman, here's a quote from the Bible's Genesis 41:27-28, which references the seven years of famine that would follow seven years of prosperity in Egypt (as revealed by Joseph who interprets the Pharaoh's dream): "Behold, seven years of great abundance are coming throughout the land of Egypt, but seven years of famine will follow them. Then all the abundance in the land of Egypt will be forgotten and the famine will devastate the land."

My core view that there is likely to be some lean market years ahead is based on multiple headwinds. Here are a few that concern me:

- Sluggish global economic and slowing corporate profit growth combined with sticky inflation sets the stage for an extended period of “slugflation” (which is not friendly to price earnings multiples)

- S&P consensus estimates are too high as company margins are exposed to rising costs (including but not limited to the costs of resourcing manufacturing back to the U.S.)

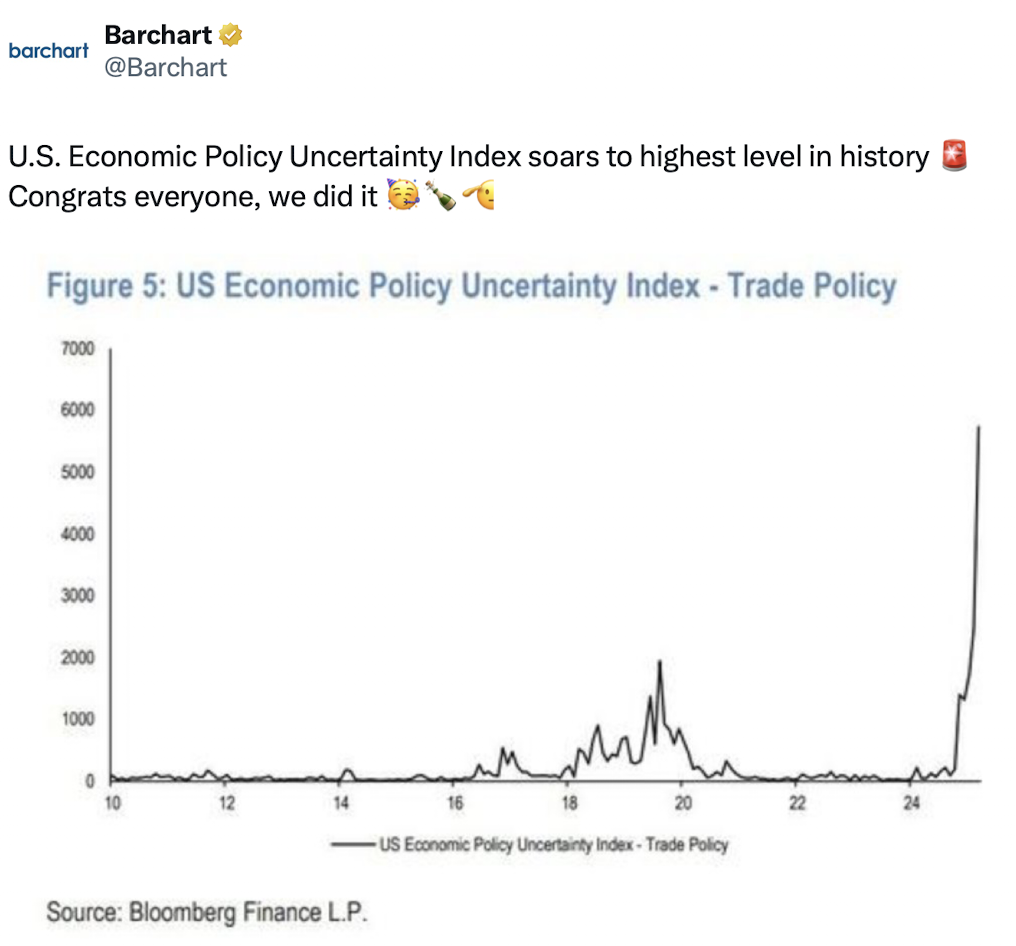

- Profligate fiscal policy and (self-imposed) trade policy errors raise the potential for a crisis in public sector finance and could contribute to the loss of U.S. “safe haven” status – this could produce adverse knock on impacts on our currency and on interest rates.

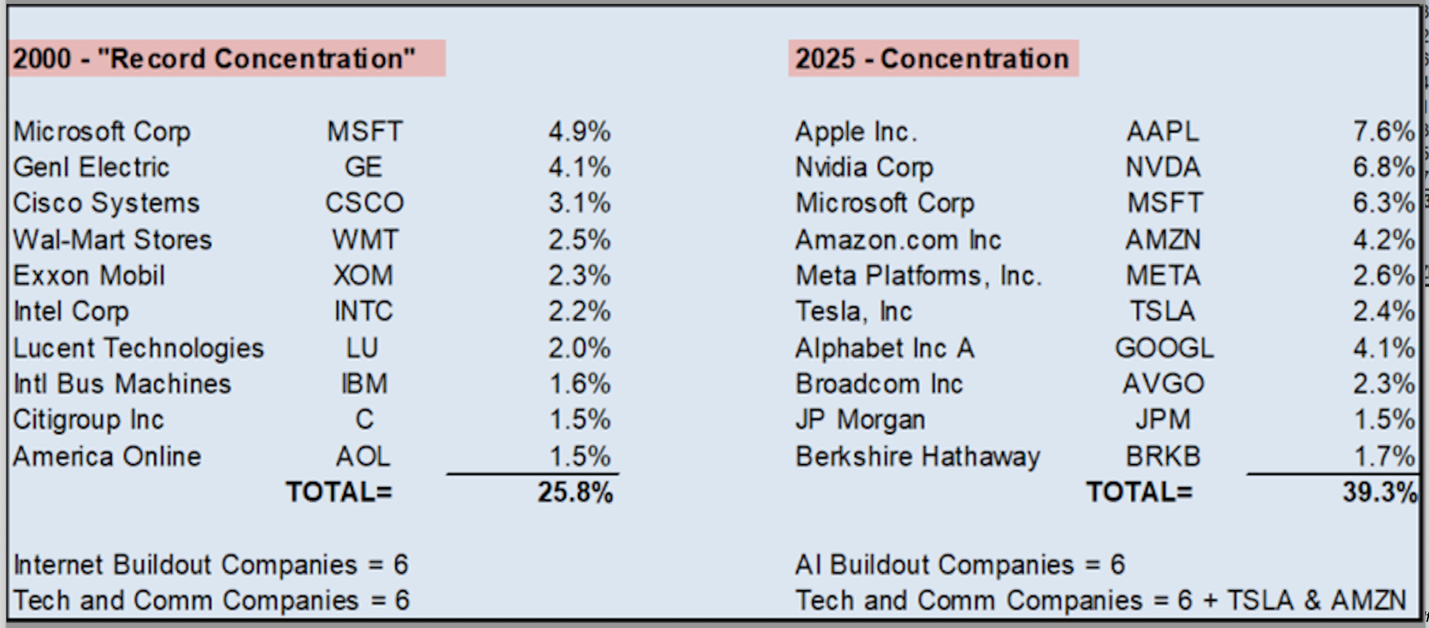

- Large-cap technology – so dominant in portfolios and in S&P 500 Index weighting - is in the cross-hairs of a number of issues/headwinds (still limited AI use sets and unclear sources of future revenues vs large AI capital expenditures, weakness in cloud, threats to current search machines, a slowdown in advertising as economic growth moderates, a spent up not pent up consumer’s appetite for “devices”, etc.)

- Elevated valuations are a poor launching pad for future investment returns

Keeping Emotions In Check In an Unpredictable and Volatile Market

Besides seeing several years of substandard performance for the major averages, I see a heightened and lengthy regime of greater volatility. This puts a premium on temperament and emotion -- things rarely discussed in evaluating money managers.

"If you can detach yourself temperamentally from the crowd, you will get very rich. You don't have to be very bright, (either), It doesn't take brains. It takes temperament."

- Warren Buffett

These conditions present an ideal setting for the contrarian, for "stock pickers" and for dispassionate and opportunistic traders (that have a sense of "intrinsic value") to produce alpha (or excess returns).

"When things go badly, people become cautious. Then, their caution causes things to go well, and when things go well, they become incautious. I think that’s a forever cycle."

- Howard Marks

Uncertainty in policy and economic/corporate profit outcomes are reagents to continued vaporous market conditions. A regime of heightened volatility is anathema to most buy-and-hold investors who might have problems with it -- having never experienced such volatility in years. By contrast, as I have written, volatility represents opportunity for money managers, as it is satisfying to those with a strong sense of "fair market value" who can capitalize on non-trending markets.

Reviewing My 2025 Expectations

I entered 2025 with the strong belief in several baseline assumptions and expectations:

* The consensus outlook for global economic growth (which serves as the lifeblood for corporate profits and stock prices) was too optimistic. Throughout 2025, growth expectations have been steadily downgraded.

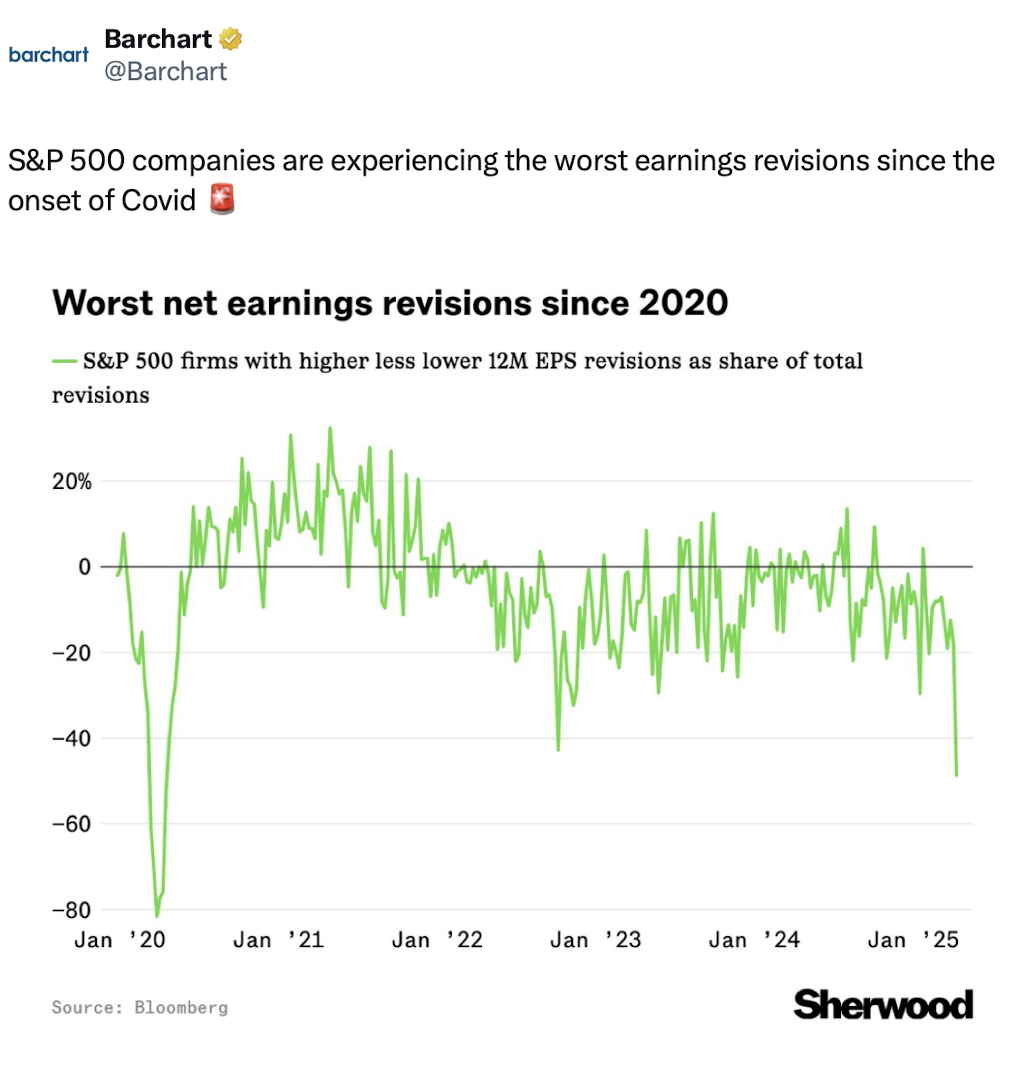

* Consensus 2025-26 S&P profit estimates were unrealistic. Earnings revisions have been marked lower in each of the last 17 weeks:

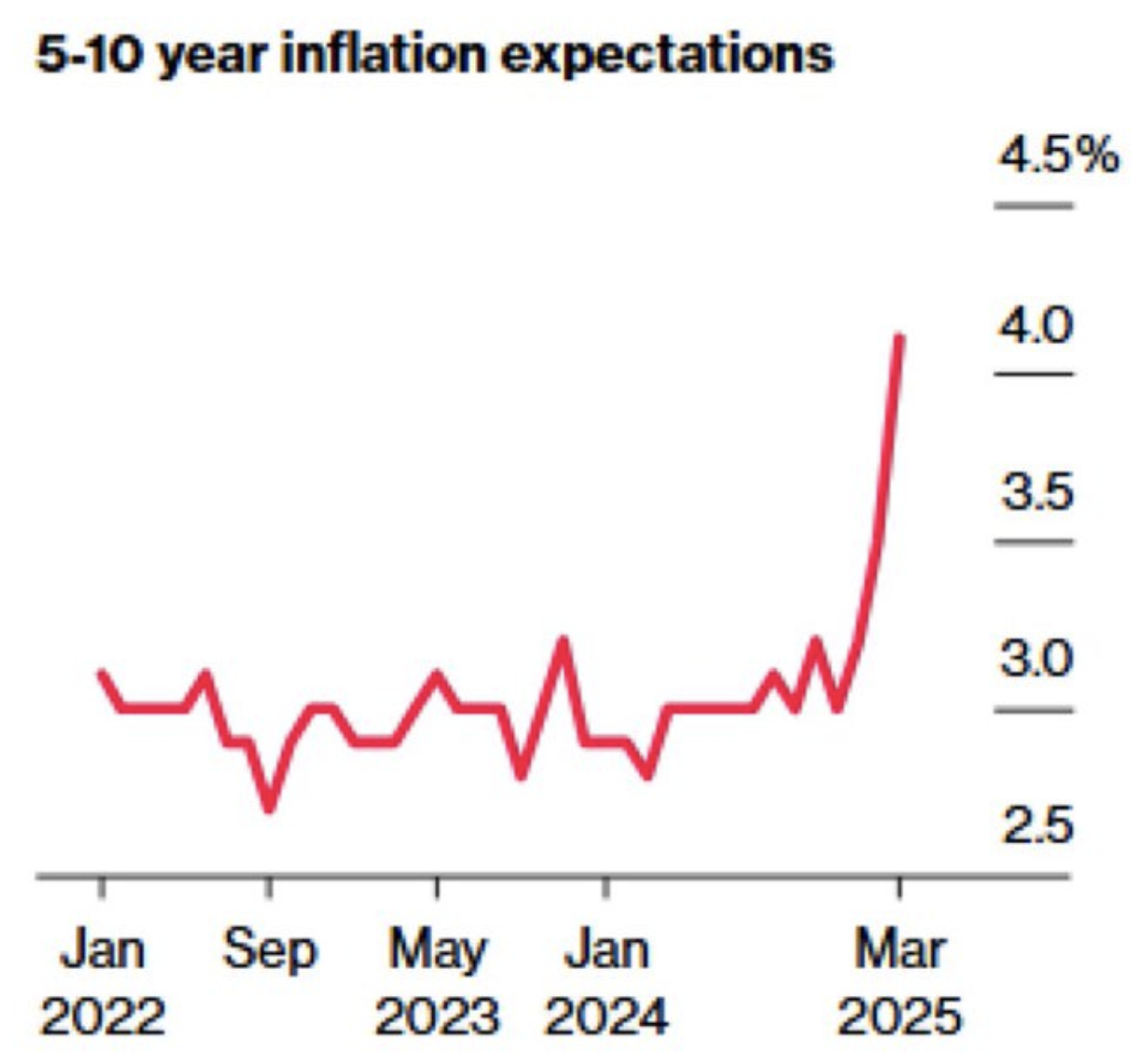

* Inflation would remain uncomfortably high. (Inflation is a price earnings multiple killer) Americans expect inflation to reach +4.1% over the next decade; that's the highest reading since February 1993:

* Fiscal and monetary policies continue to be off the rails and, at times, are dangerously unpredictable and improvisational. Regardless of one's political views, some of these conditions and policies have served to reduce consumer and corporate confidence and have some questioning America as a "safe haven" (with adverse implications for a lower U.S. currency and higher interest rates for longer).

The recent tariff moves, in particular, have the potential to act as a neutron bomb that could wipe out supply chains and small businesses and rekindle inflation - reminiscent of what happened with the spread of Covid.

* Going forward, overseas equities may be viewed as more favorable than U.S. equities. This has already begun to happen. Here is an 18-year chart that compares the Vanguard All World Index to the S&P 500 Index.

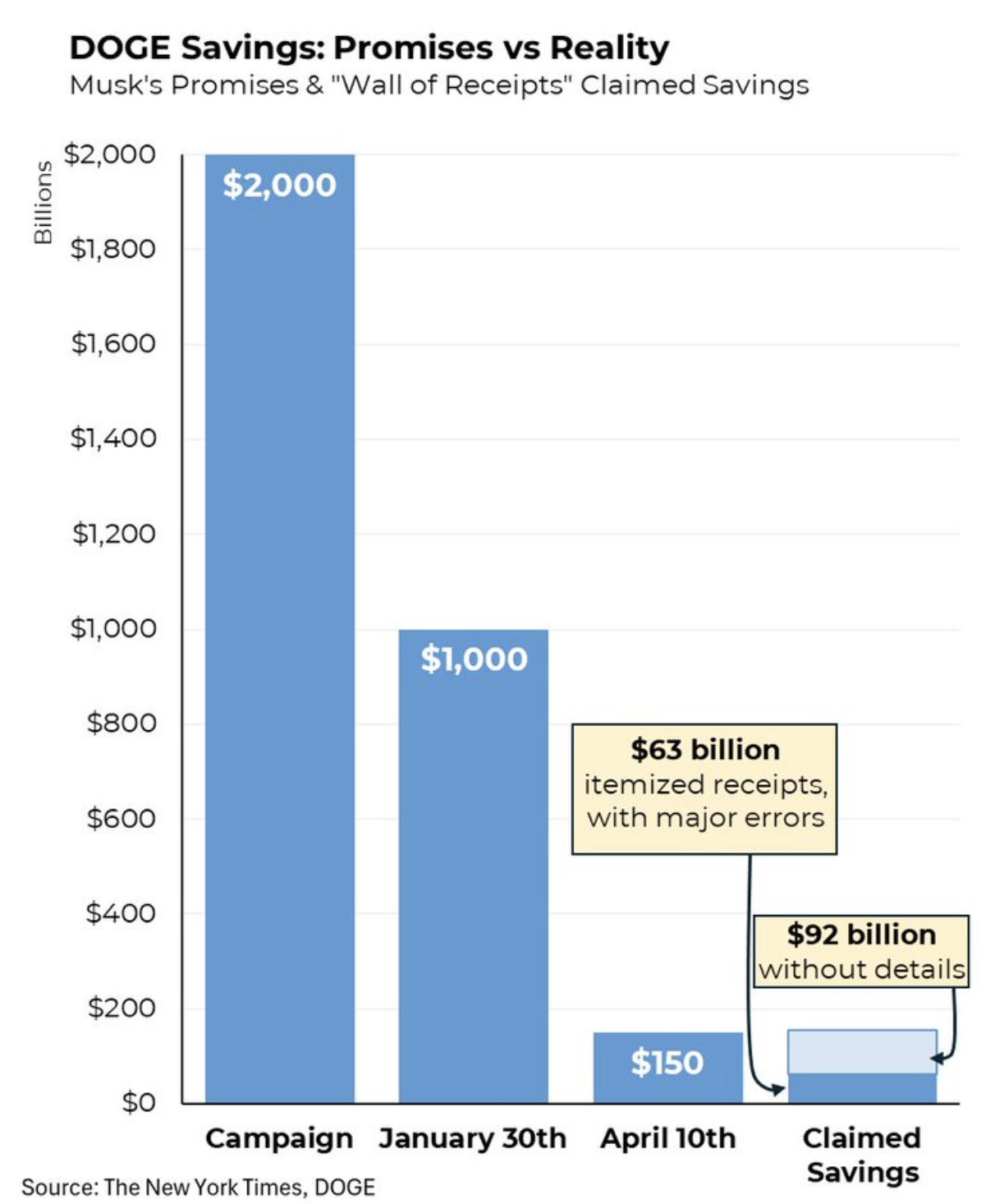

* I expected continued lack of progress in taming the U.S. deficit as Elon Musk's DOGE effort was expected to fall very short of their grandiose expectations. (This, too, has been the case.)

* I forecast that the S&P Index would make the year's top in January 2025. (Thus far this projection has proven correct -- the top was put in place during the last week of January.)

* I expected that the S&P Index had about +5% upside compared to -10% to -15% downside. (Again, correct in forecast thus far; the S&P Index rose by +5% by late January and fell to -16% in early April.) This anticipated range provides us with a general guideline to when we will accumulate equities and when we will disaccumulate (and short) stocks.

* The long climb of large-cap technology stocks (Mag7) could come to an end early in the year, resembling the end of the popularity of the Nifty Fifty in January, 1973. (This rotation away from Mag7 has been conspicuous this year and is growing ever more glaring in recent weeks.)

I recently wrote:

The conditions that exist today remind us of an important market top that took place in January 1973. Like 52 years ago, today we face a combative President (Nixon/Trump), market leadership is narrow (it was The Nifty Fifty in the early 1970s and The Magnificent Seven in recent years), interest rates and inflation have turned up (from the prior few decades) and public sector debt has been climbing rapidly. Also, like in 1973, we lack visibility today with regard to any fiscal discipline by our government. In both periods, the forward price-to-earnings was extremely elevated (today, at 23x, in the 96%-tile), the market advance was not broadening out, the "animal spirits" took stock prices higher without a commensurate change in future profit forecasts, and the equity risk premium was paper thin.

An epic market top was completed in January 1973 — leading to a poor year for the S&P Index, which marked the beginning of the end of the Nifty Fifty and several years of weak performance in the Indexes. I expect something similar in January 2025 — an important market top, a down year for the averages and marked by the beginning of the end of the Mag 7, which could extend multiple years. The Unexpected and Leveraged Corners of Speculation* As we have already noted, the entirety of the recent market advance has been based on an expansion in price earnings multiples.

Should I be correct that large cap technology has made a cycle peak, Magnificent Seven’s heavy weighting in the S&P Index and dominance in portfolios will importantly contribute to our lean years thesis:

* Given all of our fundamental and valuation concerns, consensus year-end target price forecasts for the S&P Index for year-end 2025 are still too lofty.

* A number of factors, including market structure and uncertain policy, will likely contribute to unprecedented volatility in our markets this year. (This has proven to be quite accurate.)

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no position any security mentioned.