Doug Kass: Goodbye Goldilocks (Hello Reality)

As equities fall and the price of crude oil rises, the 'Long Boom Curse' may apply today!

You've reached your free article limit

You've read 0 of 1 free Pro articles.

“The obscure we see eventually. The completely obvious, it seems, takes longer.”

- Edward R. Murrow

Following a remarkable climb in equities since early April, it is being argued by a growing body of market participants that a new bull market leg has emerged, coincident with a virtuous economic and corporate profit cycle that may lie ahead: "Carson Group: Welcome to the Start of a New Bull Market?"

It should be emphasized that many of the newly minted bulls were actually very scared during the first week of April. They are the most optimistic today — reminding us of The Divine Ms. M's (Helene Meisler) quote:"There is nothing like price to change sentiment."

I strenuously disagree with the newly minted market optimism. In fact, it is my view that not since Wired Magazine's ill-timed late 1990s cover story "The Long Boom: A History of the Future, 1980-2020" (authored by Peter Schwartz and Peter Leyden) has a new investing paradigm been forecast:

“We’re facing 25 years of prosperity, freedom, and a better environment for the whole world. You got a problem with that?”

Of course that remarkably upbeat (but wrong footed) column was followed quickly followed by a -80% drawdown in the Nasdaq Index! To me, the "Long Boom Curse" probably also applies today!

In Thursday's market update (Downside Market Risk Is About 5-Times Upside Reward) I make the opposite — that there is no new investing paradigm ahead as we could not only face seven lean months over the balance of 2025 but, perhaps, another 6.5 lean years after that.

To summarize some of my concerns:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

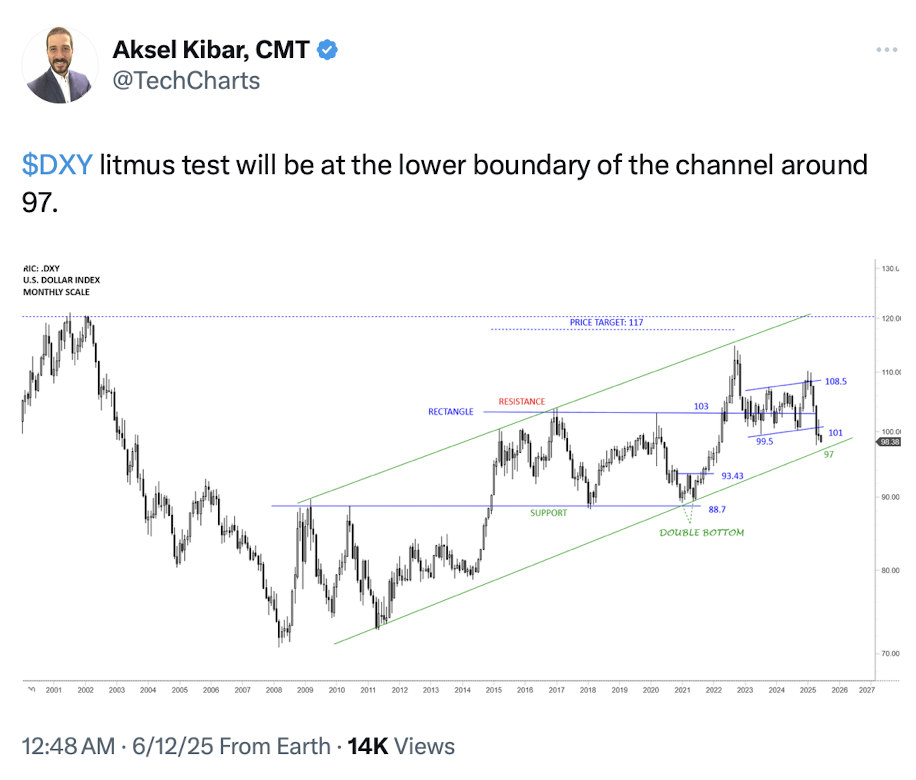

See: NDR: Breakdown for U.S. dollar?

* We face the greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsover.

* We face the largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot.com, it feels like deja vu all over again.)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

As I have also noted, what is most surprising is that market enthusiasm has multiplied at a point of time in which price-earnings multiples are at an elevated 22-times.

Here are some snippets from my Thursday column, which support my more ursine view, which is backed by rising, not declining uncertainties:

My commentary today is decidedly downbeat – some might even say dystopian. But I think my concerns are largely justified. Importantly, with markets trading at a 22-times forward price earnings multiple there is little room for disappointment.Indeed, it is my view that adverse outcomes are likely to become more common place in the time ahead – witness the recent juvenile and angry Elon Musk/Pres. Trump exchanges. Never in my investing career has there been so many possible social, political, geopolitical, economic, interest rate and fiscal policy outcomes. Many of these possible outcomes could easily upset overvalued markets. Based on my calculus and scenario analysis, the market’s downside risk is roughly 5-times the market’s upside reward -- this is the worst ratio since late 2021...

Unfortunately, Americans continue to be exposed to unvarnished political self-interest, the continued loss of conventions and general lack of ethics and morals. (As an example is the insider trading of our Congressional members, right in front of our eyes). It is increasingly obvious that political positions of influence can easily be bought — sold by both Democrats and Republicans. To this observer, fewer and fewer politicians are even pretending that they care about the American people. This may help to explain the capital outflows out of the U.S. and that many (including ourselves) are "Rethinking American Exceptionalism." (Consider what the world outside of the U.S. thinks of us these days).

As dark as all this is, my concerns relate to both parties. The Republican party has its own set of issues while Democratic leadership doesn't even seem to exist — making the situation rather sickening. This concerning condition has real economic and investment consequences, most importantly as reflected in the continuing lack of fiscal discipline and unwillingness to address our country's debt load. I express this reality and these conditions not as political statements, but rather as economic and investing considerations. It is highly unlikely that any politician on either side of the pew will address our progressively and steadily deteriorating financial position. At this point, if they did recommend some hard decisions, they would likely be voted out of office. There are simply too many forces inside the government opposed to cutting spending to produce meaningful results -- just look at the resistance to DOGE.

Whether the "big, beautiful bill" increases or decreases the deficit by a few trillion dollars has now lost its relevance. We have already lost the ability to control the deficit — as the total federal debt load is now projected to be nearly $50 trillion in 2030 and over $70 trillion by 2040. The harsh truth is that it is getting almost too late to dent the deficit (and the arc toward an erosion in U.S. solvency) without radical changes in non-discretionary spending and/or taxation requiring austerity and large tax increases (which would trigger a severe recession). As a consequence of the above factors (and other influences) interest rates will stay higher for much longer — an unfriendly condition for future price earnings ratios (as interest rates are at the core of all equity valuation models). Additionally, higher interest rates (and deficit neglect by our representatives in Washington, D.C.) will result in sharply rising costs of servicing our burgeoning debt load.

Bottom Line

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits — creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor."

* The cracks in the foundation of the bull market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense).

* With the S&P 500 Index at around 6000, the downside risk dwarfs the upside reward for equities — in a ratio of about 5-1 (negative).

* Valuations (a 22-times forward Price Earnings Ratio) and (consensus) expectations for economic and corporate profit growth are all inflated.

* Being dismissed are JPMorgan CEO Jamie Dimon's and others’ dour comments on complacency and a view that the corporate credit market is "ridiculously over-stretched.”

* Look for the soft data (see last week's weak ISM and climb in jobless claims) to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class.

* Below trend-line economic growth (housing will lead us lower) coupled with sticky inflation lie ahead ("slugflation") — uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions.

* Corporate profit growth (rising +13% in first quarter 2025) will markedly decelerate in this year’s second half.

* The equity risk premium is at a two-decade low - typically consistent with a slide in equities.

* The S&P Dividend Yield is at a near record low of 1.27% - and the spread between the dividend yield and the 10-year U.S. Treasury note yield has rarely been as wide. With so many possible adverse outcomes, my baseline expectation is for seven lean months ahead over the balance of 2025:

"In the Bible, 'lean years' refer to a period of famine that follows a time of abundance, particularly in the story of Joseph in Genesis 41. The prophecy, revealed through dreams to Pharaoh, foretold seven years of great plenty in Egypt, followed by seven years of severe famine. Joseph, interpreting the dream, advised Pharaoh to prepare for the lean years by storing grain during the period of abundance. This preparation allowed Egypt to survive the famine while other surrounding lands suffered greatly."

This commentary was originally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.