Doug Kass: Complacent Bulls Are Alive and Well and Living on Wall Street

Investors are astonishingly bullish and dismissive of a plethora or possible adverse outcomes. When we stop questioning, complacency leads the way.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Sundays, the bulls get so bored

When they are asked to show off for us

There is the sun, the sand, and the arena

There are the bulls ready to bleed for us

It's the time when grocery clerks become Don Juan

It's the time when all ugly girls

Turn into swans, hah

Who can say of what he's found

That bull who turns and paws the ground

And suddenly he sees himself all nude, hah

Who can say of what he dreams

That bull who hears the silent screams

From the open mouths of multitudes

- Jacques Brel Is Alive and Well And Living in Paris, The Bulls (Les taureaux)

Two weeks ago, I read (as I have for a number of years) John Mauldin's luminous weekly commentary in Thoughts From the Front Line in which he summarized some of the comments from his annual Strategic Investment Conference. (Run, don't walk to read "Thoughts From The Front Line" — subscribe, it's free!)

John has been a great pal of mine for several decades throughout which I have read his musings in detail and with interest. I was initially attracted to his writings (and thoughts) because of his facts-based market and economic analysis. I particularly admired his objectivity (and ability to react to changing conditions and trends), common sense, logic of argument and deep dives.

John constantly exhibits an ability to give you the facts (nothing but the facts!) and to, in a non-consensus way, bring up "takes" and new ideas from his analysis that I hadn't thought about. (Therein lies the value-added to me).

What caught my eye was his May 31, 2025 issue entitled "Bullish Highlights" in which John highlighted the generally upbeat equity market perspective that permeated his conference (as "pessimism is decreasing").

A vivid example was (an historically skeptical) Felix Zulauf, a former Barron's Roundtable member and Swiss money manager who expects a move to 7,000 in the S&P Index:

“So, if somebody puts a gun to my head, I would say on the S&P 7,000... and then 9,000 again thereafter."

- Felix Zulauf

As I am at the polar opposite of Felix (as I am a short-term bear), I thought after reading Felix's musings, that if he is bullish and sees equities going to new highs — I should pay heed to him.

With Felix joining the herd's bullish chorus I reexamined over several days (as John has taught me to do over the year) my ursine market view.

Despite Felix's apparent bullish turn and after that reexamination (following my second time viewing his SIC presentation) I remain stalwartly negative — and I have concluded that (what I would describe as) The Bull Market in Complacency may soon come to an abrupt end.

Most everyone focuses on two big headwinds — and are of the belief that both will soon be resolved, as these factors rarely lead to impacting the long-term economic and investing trends — and will likely lead to an extension of the April-June market climb:

* Tariffs

* The Israel/Iran Conflict

As I will explain, my concerns run far deeper that these two issues, though these headwinds may not be as short lived and trivial as bulls suggest.

In the words of a broken heart

It's just emotion that's taking me over

Tied up in sorrow, lost in my soul

- Bee Gees, Emotion

Let's briefly examine how market structure has contributed to where we are today (6,000 on the S&P Index), why emotion (and FOMO) have taken over and what other concerns I have:

Buyers Live Higher, Sellers Live Lower

Passive products/strategies, institutional and individual investors now, greater than ever, worship at the altar of price and price momentum.

The business shows are a reflection/microcosm of the consensus sentiment and are now, almost universally bullish. (Bears are scoffed out these days.)

By contrast, over the last decade I have reminded subscribers that I wake up every morning before trading starts and I ask these questions of myself. Unfortunately I don't like the answers — those answers have haunted me and they are potentially market and valuation unfriendly:

- In a paperless and cloudy world, are investors and citizens as safe as the markets assume we are?

- In a flat, networked and interconnected world, is it even possible for America to be an "oasis of prosperity" and a driver or engine of global economic growth?

- With the G-8's geopolitical coordination at an all-time low, how slow and inept will the reaction be if the wheels do come off?

I Am Shocked That Bulls Are Dismissing So Many Non Trivial Headwinds

Let's now shift to my near-term concerns that have been thoroughly dismissed in The Bull Market In Complacency.

On Monday (The Bear Market Will Be Back) and Tuesday (The Bear Market Will Be Back (Like Before)... I'll Fight the Fight and Win the War) I outlined a number of factors that investors should be concerned with:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

* We face the greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsoever.

* We face the largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot-com, it feels like deja vu all over again.) (More on this shortly.)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

These are bonafide and legitimate issues that are being ignored.

We never hear any of these concerns on the shows (they are being glossed over, at best), particularly when stocks are flirting at their highs.

But, like Tim Russert did as the longest standing moderator of Meet The Press ... let's examine what today's bulls also confidentally said in the past:

1. At the end of 2021, after a strong year, the consensus was very bullish. Equities fell by approximately -20% in 2022.

2. At the end of 2022, the consensus was negative and the S&P rose by about +20% in 2023.

3. At the end of 2023, the consensus was mixed and the S&P rose, again by about +20% in 2024.

4. At the end of 2024, the consensus was very bullish and, thus far the S&P is up only modestly (after experiencing a near -20% drawdown between late January and early April)

The other question rarely asked on the shows is what price are we paying for the confident view expressed by investors?

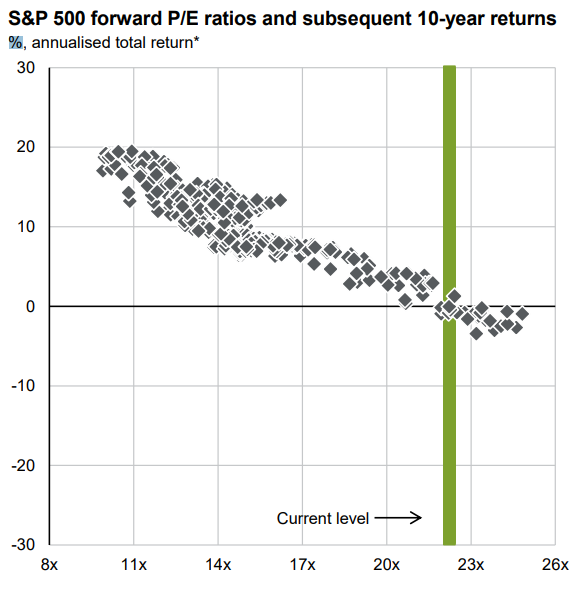

Does a 23x price-earnings multiple incorporate investors' optimism?

Does a 23x price-earnings multiple provide a "margin of safety?"

We do know, as illustrated in the chart I started today's opener with, that a 23x price-earnings multiple is historically a poor launching pad for future investment returns. This chart is so important that I am repeating it here:

To conclude this section, perhaps the overriding complacency simply reflects that investors today are trend followers and are acting like first-level thinkers:

"First-level thinking is simplistic and superficial, and just about everyone can do it - a bad sign for anything involving an attempt at superiority. All the first-level thinker needs is an opinion about the future, as in: 'The outlook for the company is favorable, meaning the stock will go up.'

"Second-level thinking is deep, complex and convoluted. The second-level thinker takes many things into account:

- What is the range of likely future outcomes?

- Which outcome do I think will occur?

- What's the probability I'm right?

- What does the consensus think?

- How does my expectation differ from the consensus?

- How does the current price for the asset comport with the consensus view of the future and with mine?

- Is the consensus psychology that's incorporated in the price too bullish or bearish?

- What will happen to the asset's price if the consensus turns out to be right, and what if I'm right?

- Howard Marks, It's Not Easy (Sept. 9, 2015)

S&P Earnings Will Not Likely Grow Into Inflated Valuations

* And Bloomberg's U.S. Economic Surprise Index is at the year's lows.

Two additional fundamental concerns should be underscored.

I am stupefied that the bullish cabal is comfortably and confidentally extrapolating 1Q2025 S&P EPS and U.S. economic growth data.

First, most bulls respond to today's elevated valuations that earnings will grow rapidly (corporate profits are the lifeblood of our markets), making a P/E multiple of 23x not unreasonable.

This, too, I disagree with:

With prices paid moving up and the prices received component now moving down — corporate profit margin squeeze/pressure likely lies ahead.

Again, consensus S&P 2025-2026 EPS estimates are too high and at a starting point of 23x forward EPS — problematic for equities.

Second, Bloomberg's U.S. Economic Surprise Index has turned the most negative thus far in 2025:

Bottom Line

When we stop questioning, complacency leads the way.

Technically and fundamentally, we are already seeing more than tiny cracks - that's how it starts.

And as we grow more complacent, cracks will deepen and widen.

Let's end with some sage and simple advice from Warren Buffett, The Oracle of Omaha:

"Price is what we pay, value is what we get."

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.