Don't Take Off Those Safety Belts Yet, Folks

Apple, Amazon, CVS, GM, and many more report this week; tariff news will still dominate (and can we trust it?) and look what Huawei's newest technology....

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What a week! From that panic-driven low last Monday afternoon up until the closing bell on Friday, the past week really was something special for traders and investors. Not only did most net long core portfolios rise sharply in value, but short-term trading opportunities seemed to show up each and every afternoon. It was as if four-plus days were plucked out of the bull market and placed in this trade-war environment that had been such a drag on stocks and other risk assets. Can it take? Will last week's run continue? Can the levels attained at least be held?

It's easy to have serious doubts, and for good reason. That said, worst-case scenarios had started to be priced into U.S. financial markets and last week ... conditions, at least for the moment, appeared to alleviate worst-case outcome fears. That doesn't mean that investors will return to a "business as usual" environment. I believe that we'll still have to learn to trade and invest in this new arena and that some of the same drivers of that panic that appeared to climax last Monday, are still out there. Not just the "Sell America" trade trend that reversed so sharply last week, but the simple reality of "headline risk."

With this president and his erratic way of messaging his both intent and his changes of heart, headline risk will persist. Then there are the facts that this is the heart of earnings season and that as the economy is showing signs of weakness, that data releases will be an ongoing threat.

The Money's Back

The S&P 500 gained a more than impressive 4.59% last week, which was the second-best weekly performance of the year for our market's broadest large-cap index. The Nasdaq Composite screamed 6.73% higher, supported by an incredible 10.94% run by the Philadelphia Semiconductor Index. It wasn't all fun and games. Despite that buyers have poured back into U.S. Treasuries over the past couple of weeks, suppressing the longer end of the yield curve, buyers also abandoned small to mid-cap stocks on Friday.

Buyers also got out of the stocks that comprise the Dow Transports. That's typically not a good sign for economic growth. On that note, we'll get our first look at Q1 GDP this Wednesday. Such is life. Still, the markets gifted us with raucous rallies last week that spanned across both "growth" sectors, all five cyclical sectors and even reached down into the "defensives." We'll take it, largely because we did need it. Last week bailed out many struggling traders.

Even if still under water since the trade war began in earnest, were any "profits" taken last week? Hope is not a strategy. Assuming purchases were made last Monday and late the week prior, profitable traders must act on both sides of the market as appropriate. Investors who do something else occupationally are different. You can take your eye off of the ball from time to time as long as you rebalance your book on a pre-set schedule. Traders, though, must maintain a certain level of cash just to remain mission capable.

Matter of Trust

So, do we trust the past four sessions? Sure, the president spoke of contact between the U.S. and China, despite Beijing's denial. Sure, the president's administration has hinted at a number of trade deals that might be in the works with various nations, Asian nations in particular. Sure, the president scaled back on his aggressive rhetoric regarding Fed Chair Jerome Powell's immediate future. These were all headline items that led the keyword-reading algorithms that control price discovery in 2025 in a northerly direction for the period.

Markets will still have to deal with great uncertainty and that uncertainty will grow as trade deals become difficult to get across the finish line or become messy so to say, all as the economic data gets wobbly. Investors may have to settle for "letters of understanding" and the like as actual signed trade agreements could take the remainder of this president's term if Treasury Secretary Scott Bessent is taken at his word.

The Numbers

What the major to mid-major U.S. equity indexes did as equity markets struggled through the holiday shortened week just completed. Most of these indexes remain close to the midpoints of their ranges for the month of April.

- The S&P 500 gained 0.74% on Friday and 4.59% for the week.

- The Nasdaq Composite gained 1.26% on Friday and 6.73% for the week.

- The Nasdaq 100 gained 1.14% on Friday and 6.43% for the week.

- The Russell 2000 closed flat on Friday but gained 4.09% for the week.

- The S&P Small Cap 600 gave up small on Friday but gained 3.76% for the week.

- The S&P Mid Cap 400 gave back 0.42% on Friday but took back 3.18% for the week.

- The Dow Transports gained 0.43% on Friday but surrendered 1.93% for the week.

- The Philly Semiconductors gained 1.03% on Friday and a stunning 10.94% for the week.

- The KBW Bank Index lost 0.41% on Friday but gained an impressive 5.74% for the week.

On Friday, just four of the 11 S&P sector SPDR ETFs closed in the green, led higher by the Discretionaries XLY and Technology XLK. Though seven of these funds closed out the day in the red led lower by the Materials XLB, none of them lost a full percentage point on the session.

For the week, ten of the 11 sector SPDR funds made gains. Technology was the big winner, up 8.09%, followed by the Discretionaries and Communication Services XLC. Those two funds were up 6.58% and 4.6% for the week, respectively. Only the Staples XLP lost ground over the five-day period.

Earnings

We're now into the meat and potatoes of first-quarter 2025 earnings season. According to FactSet, with about 36% of the S&P 500 having reported, 73% of companies so far have beaten earnings expectations, while 64% of them so far have beaten expectations for revenue generation.

On a year-over-year basis, the S&P 500 is running at a Q1 blended (earnings & expectations) growth rate of 10.1% for earnings, up "big" from just 7.2% last week. Revenue growth is running at 4.6%, up from 4.3% a week ago. Interestingly, the outlook for the second (current) quarter is still falling out of bed. Consensus for Q2 earnings growth is down to 6.4% from 7.2% a week ago and from 9.1% three weeks ago. Q2 revenue growth is currently seen at growth of 4.0%, down from 4.2% last week and 4.6% three weeks ago.

For the first quarter, Health Care is currently expected to show earnings growth of 36.7%, with Technology a very distant second place at growth of 15.1%. Four sectors are still expected to post Q1 earnings contractions led lower by Energy (-14.2%) and the Materials (-7.7%).

For the full year 2025, Wall Street now sees earnings growth of 9.7% even, down from 10% a week ago, and 11.3% three weeks ago. Expectations for full year revenue growth have fallen from 5.4% to 5.0% over those same three weeks.

As far as valuation is concerned, the S&P 500 went into this past weekend trading at 19.8-times forward looking earnings, up from 19.0-times a week ago and 24.6-times 12-month trailing earnings, up from 23.7 times a week back. These valuations both remain an inch below their five-year averages of 19.9-times forward looking earnings and 24.7-times trailing twelve-month earnings, respectively.

The GDP Game

Last week, the Atlanta Fed revised its GDPNow model for the first quarter up to -2.5% (q/q, SAAR) last week, down from -2.2% the week prior. Outside the gold trade, Atlanta sees a first-quarter GDP of -0.4%, down from -0.1%. As most readers probably well know by now, there is absolutely no consensus in regard to this economic contraction.

Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q1 growth now stands at 2.63%, up from 2.58%, while the Cleveland Fed continues to leave its model unrevised at growth of 1.86% (still wondering if this model is being updated). Interestingly, The St. Louis Fed's model was revised higher over the weekend to growth of a surprisingly strong 3.07% from 2.83%.

Where is my trusted Hedgeye Nowcast Model? If you're a reader of mine, you know that I trust Hedgeye's work enough to pay for it because I have outsourced the need for retaining a staff in this way. Hedgeye remains mildly contractionary on a quarter-over-quarter, seasonally adjusted, annualized basis for the first quarter.

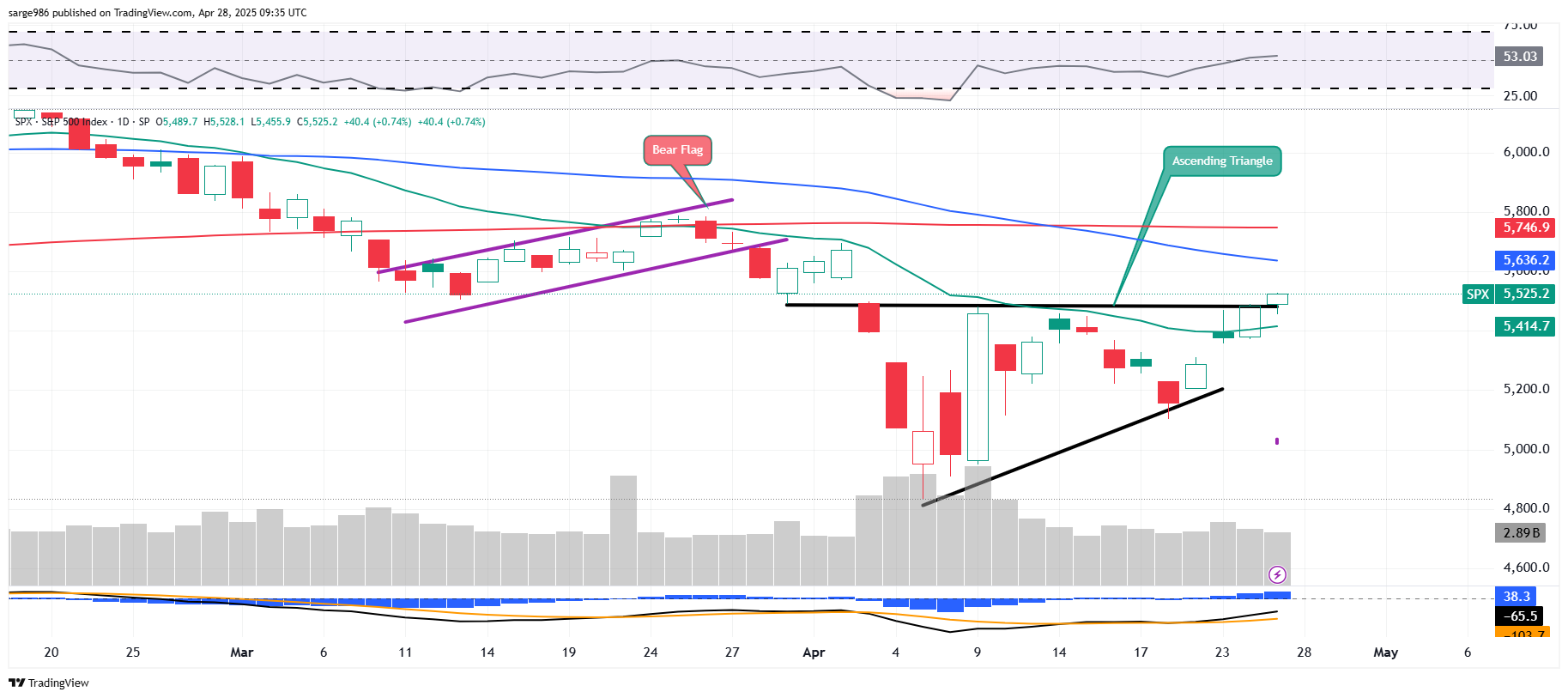

The Chart...

Equity Index futures have been a bit soft overnight but are well off of their Sunday night lows. Our daily chart of the S&P 500 continues to evolve in interesting fashion...

Readers will recall the "bullish" ascending triangle pattern that we showed you as last week wore on. On Friday, the attempt was made by the index to break out of this pattern. Should the index find support early this week at the level that had been resistance since early April, that could go a long way as markets roll into several Mag 7 earnings releases as well as the release of several key macroeconomic data-points.

Note that the S&P 500 has taken and held its 21-day exponential moving average. That could potentially keep swing traders in place as the index makes a run at its 50-day and 200-day simple moving averages. Though there will likely be resistance at both of those key technical levels, making that run will be a litmus test for portfolio manager sentiment. Taking those levels would force that crew to increase long-side exposure and allow them to do so without facing interference from their respective risk managers.

What's Ahead?

- The domestic macroeconomic calendar is pretty heavy this week. The highlight will be April "Jobs Day" this Friday. The focus this month will likely be not just on job creation and wage growth, but quite possibly on the "Underemployment Rate" as full-time employment surprisingly grew significantly in March. Before we get to Friday, investors will face the Conference Board's Consumer Confidence survey for April on Tuesday, March PCE inflation on Wednesday, Q1 GDP growth on Wednesday and the ISM Manufacturing survey for April on Thursday.

- The Fed has gone into media "Blackout" period ahead of the May 7 policy decision. We won't be hearing from this crew this week. Currently futures markets trading in Chicago are pricing in just a 7% probability for a rate cut at that meeting. However, there is now a 62% probability for a rate cut at the subsequent meeting culminating on June 18.

- The earnings calendar is extremely heavy this week. On Monday morning, we'll hear from Domino's Pizza DPZ. Then the calendar heats up. Key reports on Tuesday will be Coca Cola KO, General Motors GM, Honeywell HON, PayPal PYPL and Spotify SPOT. Wednesday brings reports from Caterpillar CAT, Meta Platforms META, and Microsoft MSFT. Thursday will be the most active day of the week for corporate earnings. That day, we'll hear from CVS Health CVS, Eli Lilly LLY, McDonald's MCD, Amazon AMZN and Apple AAPL. On Friday morning, ahead of the jobs report, we'll get a check on the energy sector as both Chevron CVX and Exxon Mobil XOM report.

Notes

- The Wall Street Journal is reporting that Huawei Technologies is apparently preparing to test the Chinese company's newest and most powerful AI-capable processor. This may or may not have negative implications for U.S. chip designer Nvidia NVDA depending on U.S. export trade rules.

- Palantir Technologies PLTR continues to break out.

The stock extended its move past pivot on Friday. The stock closed Friday's session up 4.64% for the day, up 20.26% for the week and up 26.28% from last Monday's low. Rock and Roll. Readers know that my current target price is $122. Palantir is expected to report on Monday, May 5th.

Economics (All Times Eastern)

10:30 - Dallas Fed Manufacturing Index (Apr): Expecting -15, Last -16.3.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DPZ (.76), ROP (4.74)

After the Close: NUE (.66), TER (.62), WM (1.59)

At the time of publication, Guilfoyle was long PLTR equity.