Don't Blame It on the Bonds

It's true the auction was weak, but here's what's not true. Also, let's chart the market action, and check on Palantir.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

OK, I see that Wednesday's weak U.S. Treasury auction of $16 billion worth of 20-year bonds has largely been blamed for the profit-taking across domestic equity markets over the second half of the regular session. I have read and heard of this "awful" and "horrific" auction. Yes, it's true that the auction was a bit on the weak side. It is not true that a whole lot rides on what "20-year U.S. paper" does and it is not true that portfolio managers went into Wednesday's auction holding their collective breath.

There are several other, probably more important, forces at work here. One would be advancement of the "Big Beautiful Bill," making its way through the U.S. legislature.

While the extension of the 2017 tax cuts here in the U.S. is probably paramount to a pro-growth economic agenda, there would be a huge increase made to the "SALT" cap for federal tax deductions for those taxpayers owning real estate in high-tax states. The bill in its entirety would be likely to increase the federal government's budget deficit over time, which has the fiscal hawks like me a little nervous.

Then there are other recent developments, such as Moody's downgrade of U.S. sovereign debt and a global sell-off of government debt securities that is hardly U.S.-centric. From Japan to all of Europe, yields have headed north this week. The U.S. had a weak-ish auction of a relatively small amount of a relatively insignificant series of its offerings of debt securities. The algorithms that control the point of sale then took the equity market lower from there for technical reasons, which I will illustrate for you down below.

The 20-Year Bond is not the benchmark Ten-Year Note in terms of impact. In fact, it's not the Two-Year Note, nor is it as key to the rest of the economy and public access to credit or to preservation of capital as are T-Bills of the 30-Year Long Bond. So, let's just cool our jets, take a long sip of cool water, see the lay of the land for what it is, and behave in an appropriate manner that both allows for portfolio value appreciation and provides for some protection, shall we?

The Auction

Let's take apart and look at the auction that supposedly took down U.S. financial markets on Wednesday. The high yield awarded was 5.047%, which is notable, but it's not like the Twenty-Year Note wasn't already paying better than 5%. That yield tailed the "when issued" by 1.2 basis points, which was the largest tail for this series since December. That is a sign of weakness, as was the "bid to cover," which was 2.46, down from 2.63 for this series in April.

The internals, however, were just fine. Indirect bidders (foreign accounts) took down 69.02% of the auction, which was down just a tick from April, but still stronger than recent averages for this series. Direct (domestic) bidders actually increased their appetite for the series at auction from 12.3% in April to 14.1% this month. That left dealers with a 16.9% slice of the pie, down from 17% in April.

This was certainly not the end of the world, at least not at auction. The fact that rates and yields are higher now than they were just a couple of weeks ago is real, and causing some managers to increase cash positions, but this was not a 1 p.m. ET Wednesday thing.

Marketplace

The equity market selloff was quite broad. The S&P 500 gave up 1.61%, posting a second consecutive red-candlestick day. The Nasdaq Composite surrendered 1.41% and also posted a second consecutive losing session. The difference was that on Tuesday, markets rallied throughout the session to close down small, while on Wednesday, the pressure accelerated into the afternoon.

Moving out into the weeds just a bit, the "ugly stick" really made its presence felt. The Philadelphia Semiconductor Index lost 1.8% on Wednesday as the Dow Transports gave back 2.7% and the Russell 2000 gave up 2.8%. The KBW Banking Index was taken out to the woodshed for a loss of 3.07%.

All 11 S&P sector SPDR exchange-traded funds closed out the Wednesday session in the red, led lower by the REITs XLRE, Health Care XLV, the Financials XLF and the Discretionaries XLY all of whom lost at least 2.03% and as much as 2.65%. Communication Services XLC at -0.75%, was the only fund among the eleven to lose less than 1%.

Breadth was awful. Losers beat winners at the NYSE by a rough 9 to 1 and at the Nasdaq by about 17 to 4. Advancing volume took just a 12.1% share of composite NYSE-listed trade, but a more respectable 39.8% share of composite Nasdaq-listed activity. The scary thing on Wednesday was the trading volume. Aggregate trade increased by 19% on a day over day basis across the realm of NYSE-listings and by 22.8% across Nasdaq-listings.

Bond Vigilantes?

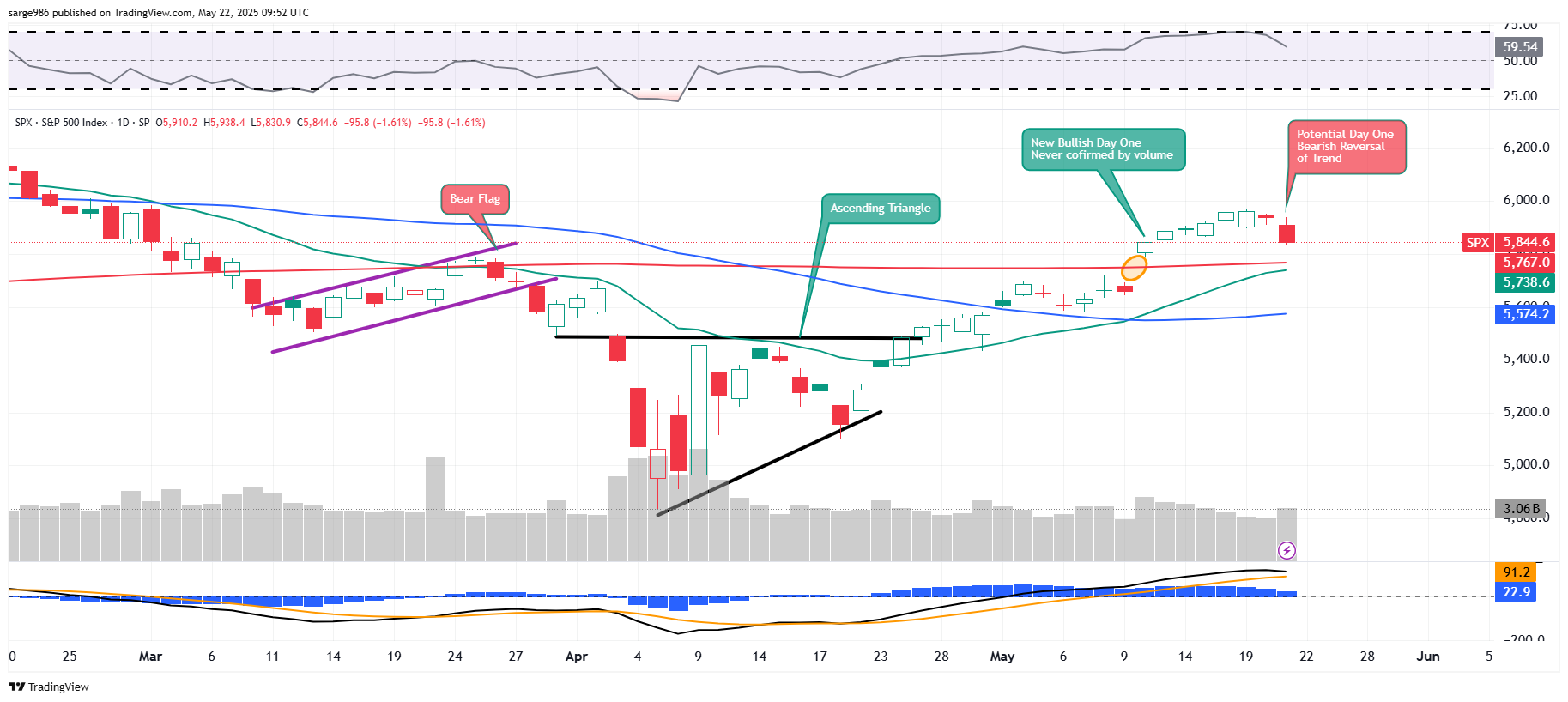

Oh, I do believe in the bond vigilantes. I do believe that they may be warming up. I'm just not sure they were all over this market on Wednesday as some believe. At least a significant portion of the selloff can be attributed to an algorithmic response to a failure to confirm a next leg of the equity market rally in place since the lows of April 7. Let me show you...

This chart illustrates how I have guided readers through the past couple of months. We had that Bear Flag in March that produced some selling pressure, followed by the Ascending Triangle in early April that generated an upside breakout. Those patterns worked like a couple of charms.

Then we get to the bullish regeneration of a "Day One" set-up on May 12. This "Day One," readers will see, was never followed by the required pause as trading volumes drifted lower for five consecutive green candle days.

We had no confirmation of the extension of the rally. The market turned on Tuesday, and now we have a potential bearish "Day One" change of trend on our chart. We need at this point a pause and a day of confirmation, but going the other way. Could news events such as trade deals impact this change of trend? Sure, but news events work in both directions. Be ready, and as Arthur Cashin always used to say... "Stay nimble."

Palantir's in the Army

On Thursday evening, the Department of Defense announced that Palantir Technologies PLTR had been awarded a $795 million U.S. Army modification contract for Maven Smart System software licenses. Work locations and funding will be determined on an order-by-order basis. The contracting agency is the Army Contracting Command Aberdeen Proving Ground in Maryland and the work is to be completed by May 28, 2029. This modification is an increase to the $480 million contract that had been previously awarded.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 230K, Last 229K.

08:30 - Continuing Claims (Weekly): Last 1.881M.

09:45 - S&P Global Manufacturing PMI (May-Flash): Expecting 50.0, Last 50.2.

09:45 - S&P Global Services PMI (May-Flash): Expecting 50.9, Last 50.8.

10:00 - Existing Home Sales (Dec): Expecting 4.15M, Last 4.02M SAAR.

10:30 - Natural Gas Inventories (Weekly): Last +118B cf.

The Fed (All Times Eastern)

2:00 p.m. - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: AAP (-.69), ADI (1.70), RL (2.04), WSM (1.76)

After the Close: INTU (10.91), ROST (1.44), WDAY (2.01)

At the time of publication, Guilfoyle was long PLTR equity.