Dissecting the Aussie Deal, Apple's Chart, Who Wins When AWS Loses

The great under-covered deal on rare earths could shift the China-trade dynamic; also let's see who could benefit from Amazon's outage and check out AAPL's blast-off.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The deal on Monday was not quite under the radar, but certainly under-covered by the media: Pres. Trump signed what might be described as a "landmark" agreement with Australian Prime Minister Anthony Albanese. The idea is simple. The two nations, both rich in rare earth minerals and metals, will jointly invest in the mining of these materials and in their processing and refining as well. That, in theory at least, would reduce reliance upon Chinese refiners as the global base of supply for such critical resources.

Under the agreement, according to Bloomberg News (I have not yet seen the text), Australia will beef up its ability to process these materials while the U.S. will help protect Australia from unfair trade practices as it does so. Both the U.S. and Australia will pay more than $1 billion over the next half year to get the program under way and that will set the stage for further projects related to a continuance of this relationship.

This announcement comes after China's recent announcement concerning additional restrictions on the export of critical minerals to the U.S. and ahead of the upcoming meeting in South Korea between Pres. Trump and his counterpart in Beijing, Xi Jinping. This is easily the most significant bilateral deal made between "western style" democracies in the critical minerals and metals space and almost certainly weakens to some degree Beijing's hand going into the upcoming trade negotiations.

Additionally, Australia agreed to purchase $1.2 billion worth of underwater drones and take delivery of the first tranche of Apache attack helicopters as part of a $2.6 billion deal. The Apache is a Boeing (BA) product that in U.S. versions is built with an engine manufactured by GE Aerospace (GE) . GE reports this morning. The "Ghost Shark" underwater attack drone is likely what the Royal Australian Navy is purchasing here. These are manufactured by Andruil Industries, a private company. Palantir Technologies (PLTR) is likely involved with Andruil in this project somehow. That last part is opinion, not fact.

On top of all of that, under the Biden-era AUKUS pact between the U.S., UK and Australia, the South Pacific nation still may purchase as many as five Virginia-class nuclear submarines by 2030. These subs are a General Dynamics (GD) product and are propulsed by pump-jets created by BAE Systems (BAESY) rather than by traditional propellers.

Up & Running?

It appears so. Overnight Sunday into Monday, Amazon (AMZN) Web Services experienced a major widespread outage that in turn, disrupted service across a broad swath of major websites and apps. AWS confirmed that the outage stemmed from its US-EAST-1 region. The company spent most of the day in recovery mode. I know that several of the websites that I use on an everyday basis were down on Monday morning and then crashed on and off throughout the day after I thought that I had them back.

While everything appears to be back to normal, and has been since Monday afternoon as far as I can tell, an experience like this that costs many businesses as much as half a day, will likely drive an acceleration across C-Suites this morning for many large businesses to diversify the cloud services that they rely upon so as not to lose their own customers' orders. This event likely ends up being a positive catalyst for the likes of Azure at Microsoft (MSFT) , Google Cloud at Alphabet (GOOGL) and to a lesser degree, Oracle (ORCL) .

Marketplace

Monday was a truly great day for risk assets. Some were calling it the "Everything Rally." Treasury debt securities found a bid as the yield for the U.S. Ten-Year Note dropped to 3.98%. I have seen U.S. Ten-Year paper pay less than 3.97% overnight. Gold, silver and Bitcoin all rallied on Monday, but all three have sold off a bit overnight as the U.S. Dollar has strengthened against both the yen and the euro.

Propelled by a rise in the share price of Apple (AAPL) , the major equity indexes showed great strength on Monday. The S&P 500 gained 1.07% for the session, outdone by the Nasdaq Composite which ran 1.37%. Dropping down to the mid-majors, the KBW Bank popped for a gain of 2.2%, while the Philadelphia Semiconductors moved 1.58%. All of our small to mid-cap indexes showed daily gains of between 1.16% and 1.95%.

Of course, it was not just Apple's run for glory that pushed markets higher. National Economic Council director Kevin Hasset, told CNBC in a Monday morning interview that he expected that the government shutdown was "likely to end sometime this week." Hasset believes that moderate Democrats will take party leadership away from the extreme left in order to strike a deal and get the government reopened this week. Please save your hate mail. I am just reporting on what Hasset said.

Nine of the 11 S&P sector SPDR exchange-traded funds closed out the Monday session in the green, led by the Materials (XLB) thanks to Cleveland- Cliffs (CLF) , the Industrials (XLI) and the Financials (XLF) . Only the Staples (XLP) and Utilities (XLU) closed in the red as defensive type sectors took four of the bottom five rungs on the daily performance tables.

Tricky Breadth

This is not easy to figure out. Positive breadth was dominant. Winners beat losers on Monday by a rough 17 to 4 at the NYSE and by about 10 to 3 at the Nasdaq. Advancing volume took a 79.4% share of composite NYSE-listed trade and a 70.4% share of composite Nasdaq-listed activity. All good, right? How about trading volume? Hmm... Aggregate trade ended Monday down 1.2% across Nasdaq-listings on a day over day basis and down a more significant 12.8% across NYSE-listings. Trading volume was notably lighter across the membership of the S&P 500 as well.

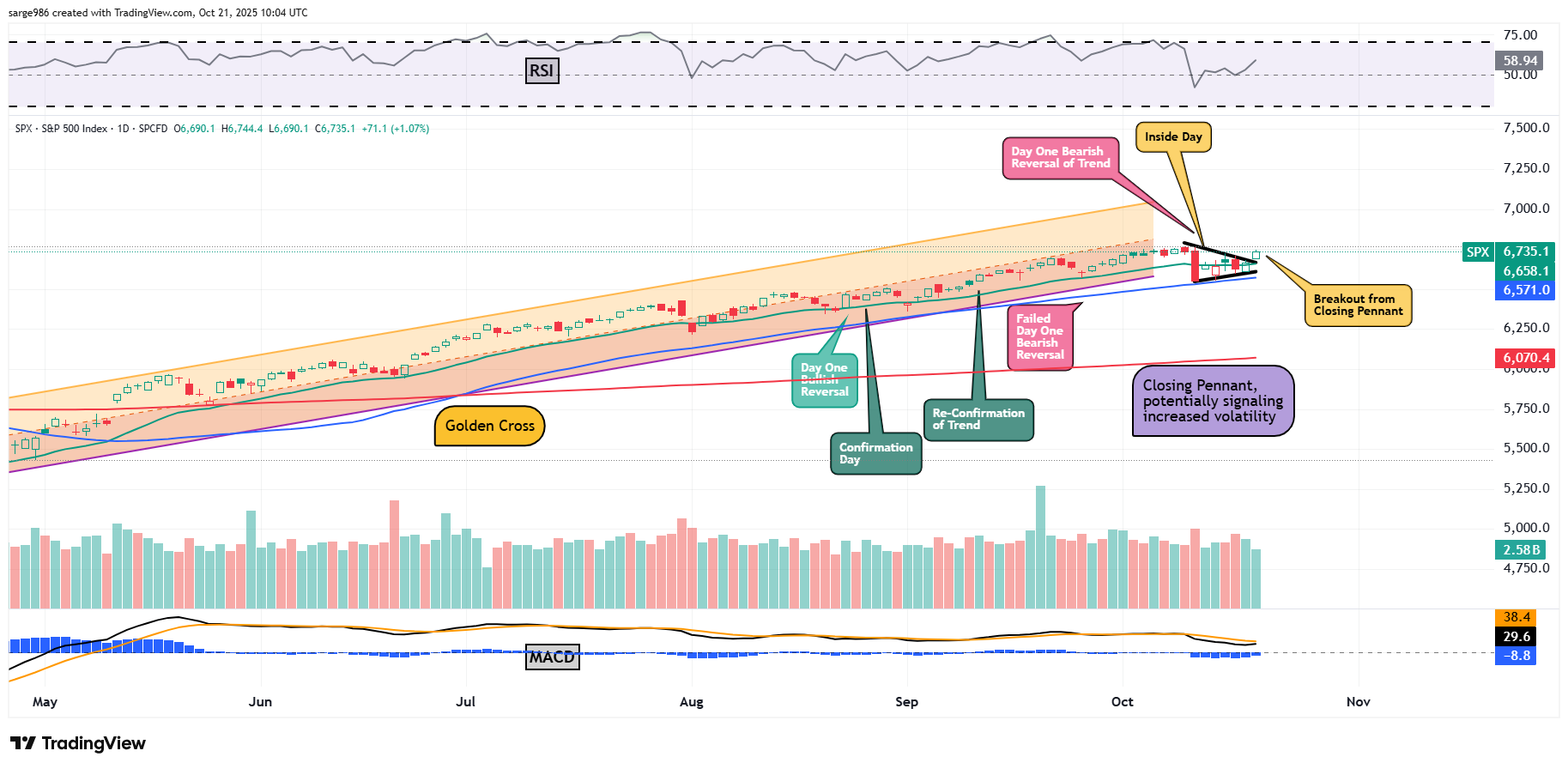

There is a big "but" here though. But how do we account for the outages across those businesses reliant upon AWS. We do know that trading volume was adversely impacted. What does that mean for us? Take a look at the chart:

We look like we definitely have a violent upside breakout from a Closing Pennant pattern on Monday. This technically puts to bet the "Day One" bearish reversal of trend from Friday, Oct. 10. That attempt to rattle the marketplace has died in obscurity. The next attempt will be a new attempt altogether and will be unrelated.

But does yesterday, in addition to representing a breakout from a closing pennant, also represent a re-confirmation of the bullish trend? Without knowing precisely, the impact of yesterday's AWS outage upon trading volume, this question cannot be answered. WE may have just experienced a technical re-confirmation of the bullish trend, but I cannot tell you this with any certainty. Very, very frustrating and quite frankly, creates opportunity cost for many of us.

Blast-off!

On Thursday, shares of Apple traded at a new record for the first time in 2025. AAPL finally completed a 100% retracement of the December 2024 through April 2025 selloff.

That $260 December 2023 high is your pivot. As the stock has appeared to respect Fibonacci sequence retracement levels on the way up, especially the 50% (not a true Fib level, 61.8% and 78.6% retracement, it stands to reason that a reasonable target price for AAPL should it hold the 100% retracement (a big if), could be the 161.8% retracement level at $315. No, I am not long the shares.

Economics

(All Times Eastern)

08:55 - Redbook (Weekly): Last 5.9% y/y.

4:30 p.m. - API Oil Inventories (Weekly): Last +3.524M.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: MMM (2.07), KO (.78), DHR (1.72), GE (1.47), GM (2.33), HAL (.50), LMT (6.35), NOC (6.46), RTX (1.41)

After the Close: COF (4.36), CB (6.15), NFLX (6.97), TXN (1.48), WAL (2.07)

At the time of publication, Guilfoyle was long GE, NOC, RTX, BA, PLTR MSFT equity.