December Inflation Looks Pretty Chill as My Stocks Get Hot, Hot, Hot

Also, let's chart the Nasdaq and S&P as we take a cold, hard look at prices.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Whoa! Was that an overreaction on Wednesday? Sure, felt like it. Will I take it? Happily, and greedily. Especially since many of the names of which I had been public about buying on weakness, such as SoFi Technology SOFI, Palantir Technologies PLTR, Rocket Lab USA RKLB and Quantum Computing Corp QUBT all outperformed the market.

Markets roared on Wednesday, as both equity and debt securities soared in response to weaker-than-expected December core consumer-level inflation and a bevy of better-than-expected earnings releases from the financial space. Sarge name Wells Fargo WFC, along with JP Morgan JPM, Citigroup C, and Goldman Sachs GS all impressed investors. Even more impressive than what happened across the equity space, the US Ten Year Note yielded 4.65% by day's end, down from 4.8%, as the U.S. Two Year Note paid 4.28%, down 11 basis points.

The rally in Treasuries stretched from the 30-day T-Bill all the way out to the Thirty-Year Long Bond. Fed Funds futures showed a strong reaction as well. Still pricing in just one rate cut for all of 2025, the probability for that quarter-point cut moved all the way up from September to June as the likelihood for a second quarter-point cut improved to 46%. On top of equities and debt securities, nearly the entire commodities complex rallied as well, despite that the U.S. Dollar Index more or less held its ground.

How Cool Was December Inflation?

In all honesty, the December consumer price index print was not as cool to the touch as one might have expected had they missed the release and only had only seen the rally in risk assets. The fact that this data came one day after a rather cool report on December produce prices, I think, is what helped produce a really strong "relief" rally up and down Wall Street.

As far as December CPI is concerned, on a month-over-month basis, the headline print landed at +0.4%, which was in line with expectations, and up from growth of 0.3% in November. On a year-over-year basis, the headline number crossed the tape at growth of 2.9% (actually 2.89%). This was also in line with consensus and up from November, which printed at growth of 2.7%. So, let's make sure this is understood. Headline consumer prices are still accelerating to the upside. The culprits in December were gasoline, fuel oil, piped gas, used vehicles, and transportation services.

Core inflation produced a happier story and that's what markets clung to. Core December CPI hit the tape at month-over-month growth of 0.2%, down from growth of 0.3% in November and below expectations for another 0.3% print in December. On a year-over-year basis, December Core CPI printed at 3.2% vs. expectations for growth of 3.3% and down from November's 3.3%. Helping core inflation slowdown in December were Apparel, medical care commodities and medical care services. Notably, shelter prices, which had been putting upward pressure on CPI, have now printed below monthly growth of 0.5% for a fourth-straight month.

What Does This Likely Mean?

Simple. Core inflation slowed, but still expanded. Yippee! Service-sector inflation is still sticky. The acceleration is still in place and has not slowed down at the headline. Should incoming President Donald Trump's administration pursue a weaker dollar policy (forget about tariffs, as they are a tool of negotiation), this headline inflation will not abate quickly.

The Cleveland Fed's model shows January headline-level CPI slowing to growth of 2.82%, but headline CPI for the three months that comprise Q1 2025, growing a nasty looking 3.72%. What do we think that will do to Treasuries and Fed Funds futures? The Hedgeye model, which I have replaced my own model with, shows January headline CPI rising above 3% with a flat print from December as the low end of their range of probabilities.

On Equities

This is key, at least for the short to medium term. Did we just experience a "Day One" reversal of trend? Maybe. The Nasdaq Composite ripped for a gain of 2.45% on Tuesday, followed by the S&P 500, which was up 1.83%. The gains made by the small to midcap indexes spanned from 1.29% to 1.99% as the KBW Banks popped for a run of 4.07% and the Philadelphia Semiconductors took the football and ran 2.13%. The semis, by the way, are up further overnight in the wake of a solid earnings release by Taiwan Semiconductor TSM.

Ten of the 11 S&P sector SPDR exchange-traded funds closed out Wednesday's regular session in the green, with both the Financials XLF and Discretionaries XLY gaining more than 2.5%. An additional four of these funds gained at least 1.47% for the session. Only the Staples XLP finished in the red at -0.34% as defensive sectors lagged cyclicals and growth for the day.

As for breadth, winners commanded the marketplace, by an 11 to 2 margin at the NYSE and by a rough 16 to 5 at the Nasdaq. Advancing volume took a dominant 82.3% share of composite NYSE-listed trade and a nearly as dominant 75.7% share of composite Nasdaq-listed activity. Now, here's where it gets even better. Aggregate trade across NYSE-listed securities was up 9.7% day over day, while aggregate trade across Nasdaq-listed securities squeaked out a day over day expansion of 1.3%.

Day One?

Possibly....

Readers will see in this chart of the S&P 500 that we still have a head-and-shoulders pattern in place, which is bearish and did produce a minor selloff. That said, on Wednesday, the index was up sharply on increased trading volume. For the S&P 500, Wednesday was the third day of a rally off of Monday's low, but the first of those days where volume expanded.

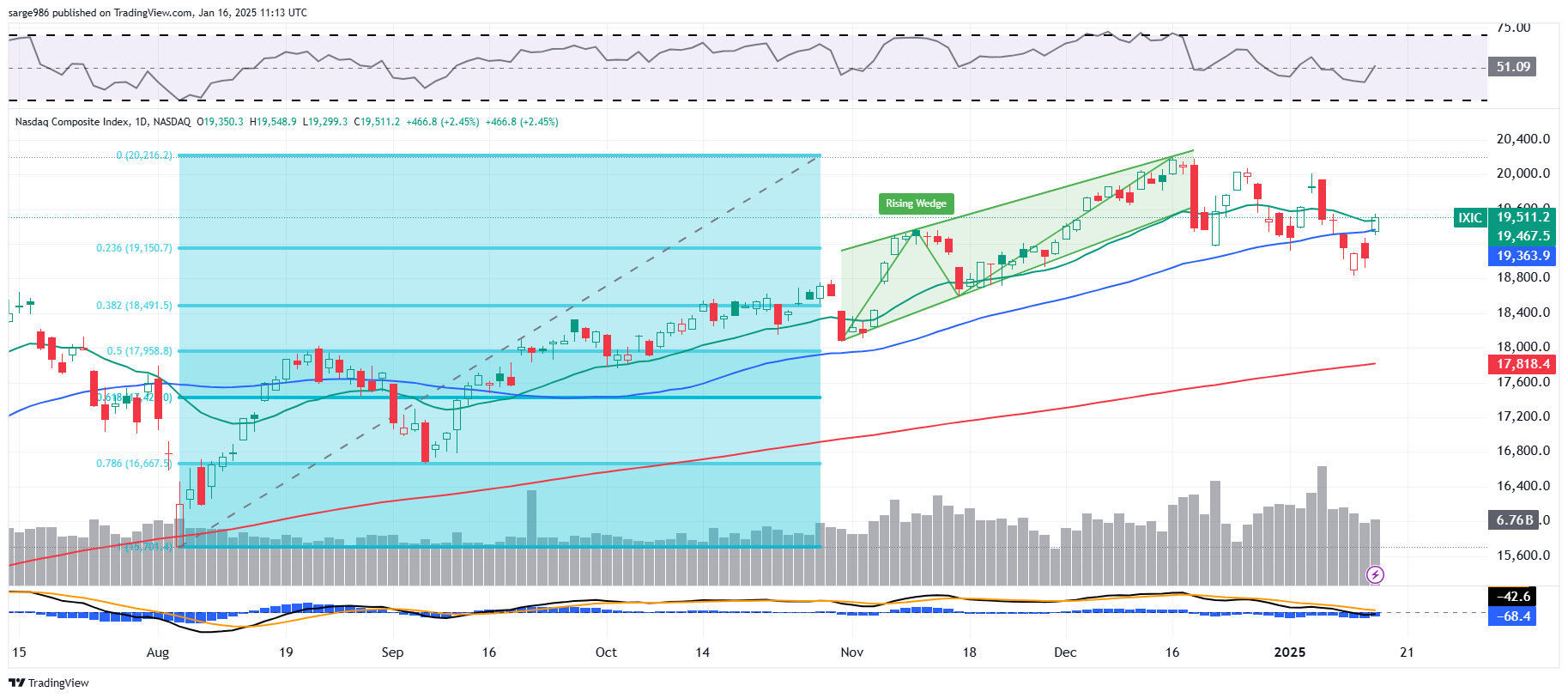

For the Nasdaq Composite, we also see the Rising Wedge pattern that we had discussed and that did produce a selloff. That said, Wednesday was the first "up" day for the index after a five-session losing streak, and trading volume expanded from where it had been.

The Catch

There has to be a break in between a "Day One" and a "Confirmation Day." While that seems simple enough, that could require the above S&P 500 to fail at the 50-day simple moving average, and the Nasdaq Composite to lose its own 50-day SMA, which is something that the index had just regained.

December retail sales are going to matter as will tomorrow's numbers for December Housing Starts and Industrial Production. All of these numbers will impact Q4 gross domestic product expectations, which will be key toward how the marketplace interprets its place at this time.

This will put undue pressure on the revisions that the Atlanta Fed will make to their GDPNow model for the fourth quarter later this morning and then again tomorrow morning ahead of a three-day weekend for the markets. I don't think we'll be bored.

Extra! Extra! Nate's Note

On Wednesday, short-seller Nate Anderson announced that he will be disbanding his Hindenburg Research firm. Anderson posted a note to his firm's website claiming that "There is not one specific thing." Anderson is just ready to close this chapter of his life and did not want his role at Hindenburg to define him. To quote the famous Yankees announcer Mel Allen... "How 'Bout That?"

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 210K, Last 201K.

08:30 - Continuing Claims (Weekly): Last 1.867M.

08:30 - Retail Sales (Dec): Expecting 0.5% m/m, Last 0.7% m/m.

08:30 - Core Retail Sales (Dec): Expecting 0.4% m/m, Last 0.2% m/m.

08:30 - Philadelphia Fed Manufacturing Index (Jan): Expecting -7.8, Last -16.4.

10:00 - Business Inventories (Nov): Expecting 0.1% m/m, Last 0.1% m/m.

10:00 - NAHB Housing Market index (Jan): Expecting 45, Last 46.

10:30 - Natural Gas Inventories (Weekly): Last -40B cf.

The Fed (All Times Eastern)

11:00 - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BAC (.77), FHN (.39), MTB (3.74), MS (1.67), PNC (3.31), USB (1.05), UNH (6.75)

After the Close: JBHT (1.62

At the time of publication, Guilfoyle was long SOFI, PLTR, RKLB, QUBT, WFC equity.