'Debt Diets' Are Manageable — But an AI Spend Diet Could Hit Growth Hard

When credit becomes a main part of the story, it is difficult to ignore. Here's why I'm nervous we could see an AI Diet developing.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I cannot remember the last time there was this much chatter about single-name credit default swaps, with Oracle’s (ORCL) CDS leading the way. Not only did we end the TV interview on Friday talking about that, but we also spent some time on Friday helping helping Barron's understand CDS, in relation to big tech and data centers.

The last time we brought up “Debt Diets” was in late 2018 as it was our “Theme for 2019.” At the time, many corporations (GE (GE) , Budweiser (BUD) , AT&T (T) , to name a few) were seeing their stocks come under pressure, largely due to strains in the credit market for their names.

It is “easy” for corporate leadership to ignore the debt markets when their stock price is doing really well. You can probably even give credit markets only a cursory glance if your stock is facing some pressure, but credit is just a side story. But when credit becomes a main part of the story — it is difficult to ignore. That isn’t necessarily a bad thing. It might sound bad, but it doesn’t have to be.

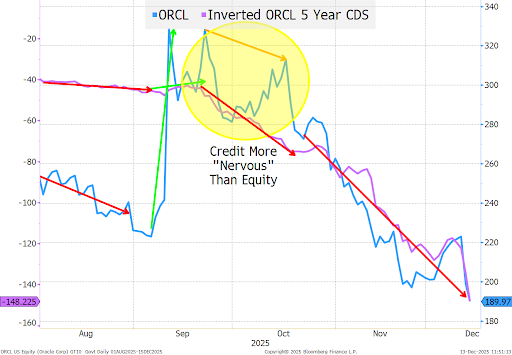

When Credit Leads the Way — The AI Debt Diet

This chart, for me, explains why a “debt diet” may be on the way (and yes, we will explain what we mean by that, and why it isn’t necessarily bad, and follows our end of “free” money narrative).

It is possible that I’m “grasping” at straws, but from the middle of September to the middle of October, the credit market and stock market were not “beating the same drum.” Yes, the stock market faced some selling pressure, but it also had a solid rebound. The credit market basically widened every day during that period.

Now they are back to moving in the same direction and it seems almost impossible to ignore the performance of the credit market when making a decision on the stock market.

Which brings us to the Debt Diet.

- Companies can alter their spending plans.

- Probably unnecessary here, but for the space as a whole, it might be a good time for CEOs and CFOs to explain their spending plans more clearly. To, not necessarily, pay “homage” to creditors, but make sure creditors understand their concerns are being taken into account.

- Clarity, especially as to what might make them cautious on building more (maybe some rough alignment of building with profits and positive cash flow in mind, versus an almost “build it and they will come” mentality).

- Companies do not need to be “afraid” of creditors, but a clearer recognition of their importance to your future might be in order.

A lot can be done without changing the plans today. I see a lot of ways that clarification and some identification of issues or trends that might change spending plans could go a long way towards= improving spreads and leaving the market hungry for more issuance in 2026 and beyond!

Debt Diets Are Manageable. An AI Spend Diet Might Not Be.

So far, this seems more like a “debt diet” type of situation in the data-center space. The news that has come out doesn’t seem to have changed the overall narrative. Backlogs, new clients, etc. all seem to argue this is more about a change in valuations than a meaningful change in trend for the industry.

However, I am nervous that we could see an AI Diet developing:

How much are companies budgeting for AI spend next year? The following year?

Just like the industry itself had “free” money for a period of time, it was impossible for any corporation in America to do anything but spend more on AI. As companies have now been using AI for two years or more, are they all seeing the benefits they thought they paid for? Certainly, some are and they are probably rejoicing in their spending. But everyone? Especially in an economy, where away from certain industries (our little i-shaped view of the economy), we are seeing little growth. For now, I think the spending from corporate America continues, but it will be possibly “abated” as opposed to unabated.

Chips and China

The Trump administration is comfortable selling a greater variety of chips to a greater variety of nations (China being the most important, though I’d argue that the Middle East isn’t far behind in importance). The question is whether China wants chips in the quantity that would fuel real revenue growth? Or is China willing to forego some quality today, in an effort to continue to bootstrap their own chip industry and make them more competitive with the top chips being designed/produced by U.S. companies and TSMC?

I think this is more about constraining the upside rather than creating downside risk to spending on U.S. chips, but I have this nagging concern that “we” may be underestimating the resources and skills that China is devoting to this.

Electricity

The importance of electricity in today’s economy is clear. As is the risk that we cannot generate electrons quickly and efficiently enough to satisfy the needs of industry going forward.

This “molecules to electrons” has been a theme of ours for quite some time and fits perfectly into our ProSec (Production for Security) framework.

I think the Debt Diet is real and not necessarily bad. I don’t think the AI Diet is real, but since it is very bad if it occurs, it seemed worth at least highlighting that risk in our “diet” framework.

All of this leaves me to be underexposed to the AI/Data Center growth story, and overexposed to stocks and sectors linked into my Production for Security (or ProSec thesis).