Data, With a Dose of Ugly

Let's see how unpleasant those numbers really were for jobs as we look toward price inflation and the forecast Fed rate cuts.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Remember last week's early Tuesday morning column that came out after the long weekend? Data released the prior week had covered personal income and spending for July as well as that month's personal consumption expenditure inflation. Those numbers came a week after the Kansas City Fed's late summer clambake at Jackson Hole. Soon to land were the Bureau of Labor Statistics market survey results for August, which were released last Friday.

Well, those employment numbers have come and gone. They were awful. The markets kind of, sort of, tried to react, but did not quite know how. Now, again, this week, we are "on to the next thing." As investors, traders, economists, job seekers, employers and heads of households all try to make heads or tails of last week's data, here comes this week's data.

Huzzah?

I let you know about "huzzah" a couple of miles down the road, gang.

I will tell you this: Ready or not, our central bankers have likely just had to switch from focusing on price stability to prioritizing full employment as they attempt to balance their dual mandate. Now, this week, inflation will push and shove its way back toward the center ring of our financial circus as the Bureau of Labor Statistics publishes its numbers for August producer level prices on Wednesday and August consumer level prices on Thursday. What could possibly go wrong?

Worse Than You Think

How disappointing was August "Jobs Week?" Well, kids, remember our old friend (he's not our friend), the "ugly stick?" The ugly stick tried to hammer Treasuries, but they hammered back. Then, the ugly stick tried to body slam the stock market, but equities refused to die and really rallied for most of Friday afternoon, leaving many traders if not the indices wondering how they managed to close out the day in the green.

Just one thing. The ugly stock put a whammy on last week's employment related data and it was not just the numbers posted by the Bureau of Labor Statistics, which I covered in depth for TheStreet PRO on Friday. Before we even got to the anemic August labor market survey results on Friday, the ADP Employment Report on private sector job creation for August forewarned that some gnarly looking digits were headed our way.

In addition to that, weekly state-level unemployment claims increased to an eleven week high. On top of that, the Challenger report of job cut announcements showed a planned 85,979 layoffs in August, up from 62,075 in July and up 13% from August 2024. This made August 2025 the worst single August for announced job cuts since the pandemic year of 2020. Ex-the pandemic year, it was the worst August since 2008.

On Those August Jobs...

Job creation has become a four-month problem. Non-farm payrolls, which is considered the headline number, drawn from the establishment survey, showed growth of 22,000 seasonally adjusted positions, well below less than aggressive expectations for roughly 76,000 new jobs.

Looking backward, July non-farm payroll growth was revised up 6,000 to 79,000, while June growth was revised down 27,000 to -13,000 making June a negative month for job creation. Not good. That leaves Friday's print as a net +1,000 from where we thought we were. Gee whiz. June had previously been revised down to the still too high 27,000 new jobs from an initial report of 147,000 for anyone wondering why someone needed to get fired at the BLS.

Oddly enough, the Household Survey showed 288,000 new hires for August, but that was after that survey showed -260,000 new hires in July for anyone still thinking a shakeup at the BLS wasn't necessary. Leaders at government agencies need to be held to private sector standards and that kind of inaccuracy would never be tolerated at any business of any kind.

Beyond the headlines, The unemployment rate inched higher in August from 4.2% to 4.3% as participation ramped from 62.2% to 62.3% moving that metric off of an almost three-year low. The number of individuals working part-time for economic reasons increased by 65,000 persons while the number of individuals working part-time for non-economic reasons increased by 528,000 persons. With 593,000 part-time jobs created, the implication taken from the household survey would suggest 571,000 full-time jobs were lost during the month.

Wage growth was disappointing as well. Average hourly earnings printed flat from July at month-over-month growth of 0.3%. But on a year-over-year basis, average hourly earnings printed at growth of 3.7%. That was down sharply from 3.9% growth in July and below expectations for 3.8% growth.

On Policy...

Looking at the Treasury yield curve, the U.S. Ten Year Note paid 4.09% by day's end on Friday, down seven basis points for the session and down 21-basis points from its high last Wednesday. The dollar showed weakness on Friday, which proved to be a positive for gold, silver, Bitcoin and the entire materials sector for the session. This was all in anticipation that Fed Chair Jerome Powell and his Federal Open Market Committee will have to be more dovish going forward than they as a group have seemed comfortable with.

Coming out of the August employment data, Fed Funds futures trading in Chicago are now pricing in a 92% probability for a quarter-point rate cut on Sept. 17, which is next Wednesday. According to these markets, there is now a 79% likelihood for a second quarter-point rate cut on Oct. 29 and a 71% probability for a third quarter-point rate cut on Dec. 10. There is now, according to these markets, a 53% chance for a whopping 2.50 percentage points worth of rate cuts by New Year's Day 2027. Personally, I see 1.5 percentage points worth of cuts by then as more realistic.

The Week That Was...

What the major to mid-major U.S. equity indexes did last week, as the nation focused on August jobs and moved into September:

- The S&P 500 gave up 0.32% on Friday, but gained 0.33% for the week.

- The Nasdaq Composite gave back just 0.03%, but gained 1.15% for the week.

- The Nasdaq 100 gained 0.08% on Friday and 1.01% for the week.

- The Russell 2000 gained 0.48% on Friday and 1.04% for the week.

- The S&P Smallcap 600 gained 0.29% on Friday and 0.83% for the week.

- The S&P Midcap 400 added 0.50% on Friday and a nifty 1.31% for the week.

- The Dow Transports lost 0.28% on Friday and a gnarly 1.11% for the week.

- The Philly Semis popped for 1.65% on Friday to gain 1.63% for the week.

- The KBW Bank Index dropped a nasty 1.77% on Friday and 1.58% for the week.

Readers will see that these results were very lumpy. Winners and losers were everywhere. There was no broad market move either on Friday nor for the week. On Friday, six of the 11 S&P sector SPDR exchange-traded funds closed out the session in the green, led higher by the REITs XLRE and the previously mentioned Materials XLB. Energy XLE was the day's big loser despite the softer greenback.

For the week, just five of the eleven S&P sector SPDR ETFs traded higher. Communication Services XLC easily led the winners followed by Consumer Discretionaries XLY. Energy was again the big loser, with the Financials XLF in tow. For those wondering what was up with the energy sector, the weakness came ahead of another expected increase in oil production by the OPEC+ nations over the weekend. That announcement came on Sunday.

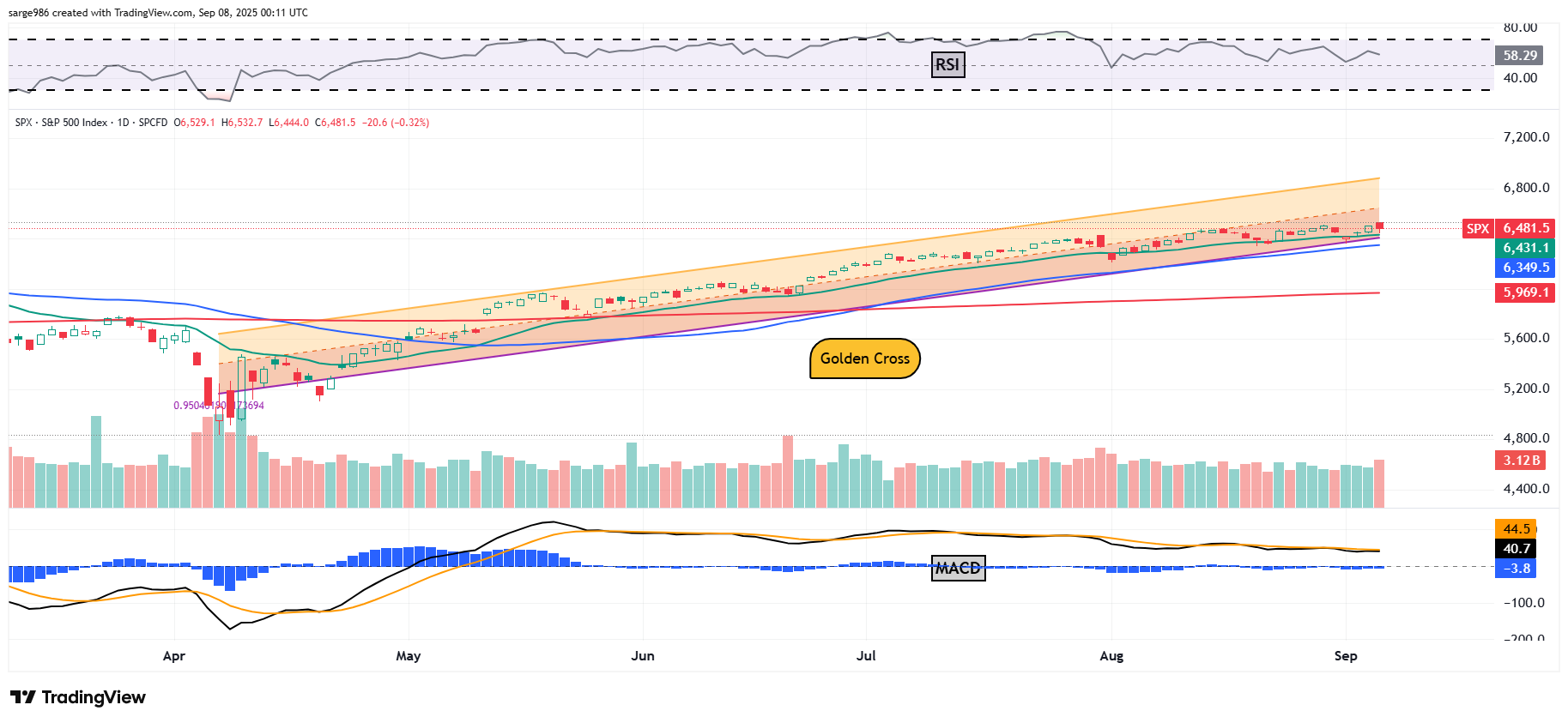

The Chart

Readers will see that I have decluttered my chart of the S&P 500 as the action over the past few sessions has really created almost a blank slate for the index. The early weak pressure last week just about negated the bullish change of trend that had been confirmed by volume the week in last August. Was Friday a "Day One" bearish reversal of trend. No, not even close. Not only did the stars not align properly, which I will explain, but the index has been moving sideways now for about three weeks. There is no bullish nor bearish trend in place.

Relative Strength has remained robust and still is without getting close to being technically overbought. Bullish. However, the daily Moving Average Convergence Divergence still paints a slightly bearish picture. The histogram of the 9-day exponential moving average is still in negative territory. That remains a potentially bearish short-term signal. The 12-day exponential moving average is still slightly below the 26-day exponential moving average. Those lines remain poised for a bullish crossover but could easily go the other way.

As for Friday, losers beat winners at the NYSE, but winners beat losers decisively at the Nasdaq. Advancing volume easily took a majority share on composite listed volume at both exchanges and on increased aggregate trade as well. If not for the fact that the indices closed ever so slightly into the red (especially the Nasdaq Composite), Friday was actually technically closer to being a green Day One than a red one.

Earnings

Second-quarter earnings season is complete. According to FactSet, for the second quarter, 81% of member companies beat earnings expectations, while 81% also surprised the street to the upside on revenue generation. For the quarter, year over year earnings growth across the S&P 500 landed at 12%, on revenue growth of 6.5%. For the period, Communication services easily led the winners, having grown earnings by a stunning 45.6%, followed by Tech at +22.9%. Three sectors suffered a year over year contraction in earnings, easily led lower by Energy (-18%). The Materials and Staples also finished on the wrong side of the growth ledger.

For the third quarter, the street is looking for earnings growth of 7.5% on revenue growth of 6.1%. Technology and Utilities are expected to be the outperformers while Energy is expected to take another beating. For the full calendar year of 2025, Wall Street now sees S&P 500 earnings growth at 10.6% on revenue growth of 6%..

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 22.4-times 12 months' forward looking earnings. That stands well above the five year average of 19.9 times for the index and its ten year average of 18.5 times. The S&P 500 also ended last week trading at 27.9 times trailing twelve months' earnings. That also stands well above the five-year (25 times) and ten-year (22.6 times) averages for the index.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the third quarter down to growth of 3.0% (q/q, SAAR) from 3.5% the week prior. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth now stands at 2.1%, down from 2.22%. The Cleveland Fed's model for the third quarter still stands at growth of 1.94%, while The St. Louis Fed model now stands at a paltry 0.56%, up from 0.54. There remains no consensus.

Two Can Play...

On Friday, Pres.t Trump threatened to move ahead on a potential trade investigation into what he referred to as discriminatory fines levied against large U.S. tech firms such as Alphabet GOOGL and Apple AAPL. Hours after the European Union had hit Alphabet's Google division with an almost $3.5 billion fine in a major search advertising antitrust case, the president went to social media.

To his Truth Social account, Pres. Trump posted: "We cannot let this happen to brilliant and unprecedented American Ingenuity and, if it does, I will be forced to start a Section 301 proceeding to nullify the unfair penalties being charged to these Taxpaying American Companies.

Additions & Deletions

Late Friday, shares of advertising technology business AppLovin APP, retail stock trading app Robinhood Markets HOOD, and construction services provider EMCOR Group EME all moved higher in after-hours trade after S&P Global announced that the three companies would be added to the S&P 500 ahead of the opening bell on Monday, Sept. 22. To make room for these three firms, MarketAxess Holdings MKTX, Caesars Entertainment CZR, and Enphase Energy ENPH will be dropped from the index.

On The Docket

......The domestic macroeconomic calendar will focus primarily on August inflation this week. The BLS will release its data for producer prices on Wednesday morning followed by its data for consumer prices on Thursday morning. Also in focus will be this Friday's University of Michigan's initial September survey results for both consumer sentiment and inflation expectations. Lastly, the U.S. Treasury will auction off $39 billion worth of new Ten-Year Notes on Wednesday afternoon and $22 billion worth of Thirty-Year Long Bonds on Thursday afternoon.

.... The Fed will be silent this week. The FOMC has gone into their eight times a year media blackout period ahead of scheduled monetary policy decisions. The meeting culminating September 17th is the first meeting of 2025 where an actual change to policy is anticipated.

..... Apple will hold its biggest product launch event of the year on Tuesday. The company is expected to announce the coming availability of its thinnest iPhone ever, an updated Apple Watch and updated AirPods according to Bloomberg News. Pricing is a huge unknown here and will likely impact the share price of the stock this week as well as the value of any and all funds holding the most widely held stock across our market.

..... The earnings calendar is extremely light this week as the second quarter earnings season has largely ended and the third quarter earnings season is still about five weeks out. There are, however, a few well-known firms that do report in between seasons. Tonight, we'll hear from Casey's General Stores CASY. Tomorrow night, AeroVironment AVAV, GameStop GME and Oracle ORCL will all go to the tape with their respective numbers. Over the rest of the week, Chewy CHWY will report on Wednesday morning, while Kroger KR and Adobe ADBE report on Thursday.

Economics

(All Times Eastern)

3:00 p.m. - Consumer Credit (Jul): Last $7.37B.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights

(.EPS Expectations)

After the Close: CASY (5.02)

At the time of publication, Guilfoyle was long GOOGL equity.