'Data Dependent' Trading

Let's see why traders took profits on Friday (you might be surprised by one reason), a look at price and wage data, the jobs and earnings ahead and the chart of the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

One week after the other, it seems, as the summer season wound down, markets have had at least one major item to focus upon, or should I say, to game. The week prior to last, all eyes and ears were on Jackson Hole, Wyoming, and Fed Chair Jerome Powell's address that Friday. Powell pivoted ever so subtly from having the central bank prioritize one side of its dual mandate (fighting inflation) to supporting the other (full employment). Huzzah!

That speech led to a same day "Day One" bullish reversal of trend after the major indexes had suffered losses for five consecutive sessions going in. The reversal was confirmed last Tuesday and that rally held, though on declining holiday weekend-impacted trading volume, into last week's "big event." That was the Bureau of Economic Analysis' release of July personal income and spending this past Friday and that same agency's release of July personal consumption expenditure data on consumer-level inflation. To say all of those data-points landed precisely as expected would not be an overstatement. That's exactly what happened.

This holiday-shortened week will be "August Jobs Week." This Friday, our beloved (just kidding) Bureau of Labor Statistics, known more for its "Pin the Tail of the Donkey" approach to economic modeling than for anything positive, will release the salted, peppered, shaken and stirred results of its two labor market surveys for the month of August. Now that we all know what we are up against this week and what those who write high-speed, high-freak (frequency) electronic trading algorithms will be working on, let the games begin.

The Data

According to the BEA, for August, personal income was up 0.4% month over month as expected. Wages & salaries, when isolated, were even stronger, up 0.6% making August the strongest month of 2025 in that regard. Interest income, however, stalled and dividend income grew below trend. Taxes were up 0.6% too. Ugh.

Personal spending was up 0.5% month over month. The breakdown is striking, though. Spending on durable goods was up 1.9% after two months of declines, but spending on non-durable goods was up just 0.1%. In fact, spending on non-durables has been up 0.1% or less on a monthly basis for four of the past five months. Yikes.

Real Disposable Income was only up 0.2%, up from June and May, but well below the pace experienced from February through April that had come after a tough winter. So, how are we doing? Meh. We're doing. How about inflation, Sarge? Hang on, gang. let's have that look:

For August, at the headline, personal consumption expenditure inflation grew 0.2% month over month, as expected and was a welcome deceleration from the 0.3% pace of July. On a year-over-year basis, headline PCE showed an increase of 2.6%, in line with expectations and in line with July. At the core, ex-food & energy, August PCE printed at monthly growth of 0.3%, in line with both consensus and July. Year-over-year core PCE hit the tape at 2.9% growth, up from July's 2.8% and in line with consensus. So, income, spending, headline inflation and core inflation dished out no surprises for August? Exactly. So, why then did traders take profits on Friday? Good question. You're a smart one, ain't ya? I'll explain.

Two Reasons

One reason is so easy that you saw it from a mile away. Traders take profits going into three-day weekends and investors reduce risk ahead of three day weekends. Unless they are given a good reason to act differently, this kind of behavior is as old as the hills. How old are the hills? I have no idea. They were here when I got here.

The other reason is less simple. Seasonality? Good guess. As we know, September on average, is the worst month of the year for financial markets. Little Johnny and Little Jane are off to some campus for Fall semester and at least for the lucky ones, somebody with a portfolio might be paying those bills. That's just one possible reason that folks with money go to increased cash levels as summer cries out in death and autumn beckons. Oh, and the algorithms that control price discovery in 2025 all have some seasonal impact worked in.

That's a great story and to some degree true. That's not why traders who were going to speed rope out of a perfectly good Huey at some point anyway on Friday did so at 10 am-ish (ET). That was the University of Michigan's fault. The University of Michigan's revision to its August survey for Consumer Sentiment hit the markets on Friday morning like a lead balloon. The revision brought consumers' one year inflation expectations down to 4.8% from 4.9%. Big whoop.

It was the sentiment survey itself that rocked the boat. Two weeks earlier, the initial release of this survey put Consumer Sentiment at 58.6 when Wall Street had been looking for something with a 61 handle. Boo. Hiss. Traders, Investors and optimists were hoping for an upward revision on Friday after such a gnarly surprise. Alas, much to their collective chagrin, the number was revised lower to 58.2 from 58.6. Making matters worse, beneath the headline, the index for current economic conditions dropped from 68.0 in July to 61.3 in August. That's pretty ugly.

Tuesday Morning ...

U.S. equity index futures have remained weak overnight into Tuesday morning. Interestingly, gold, bitcoin and crude oil have all strengthened overnight, despite a U.S. Dollar Index that has also shown some gusto. These moves were spurred on by a ruling (in a 7-to-4 vote) on Friday night by a U.S. appeals court that most of Pres. Trump's tariffs are illegal and that the president had exceeded his authority in the use of emergency powers to change trade policy. The president has pledged to take the case to the Supreme Court if necessary. The administration did not appear to be surprised by the news on Friday night.

The Week That Was...

What the major to mid-major US equity indices did last week, as the nation focused on PCE Inflation ahead of its often sloppiest month. By the way, the S&P 500 gained 2.03% for August is now up 9.84% year to date.

- The S&P 500 gave up 0.64% on Friday, surrendering 0.1% for the week.

- The Nasdaq Composite gave back 1.15% on Friday to lose 0.15% for the week.

- The Nasdaq 100 lost 1.22% on Friday, losing 0.35% for the week.

- The Russell 2000 dropped 0.5% on Friday but gained 0.19% for the week.

- The S&P Smallcap 600 gave up 0.4% and 0.35% for the week.

- The S&P Midcap 400 lost 0.54% on Friday to lose just 0.06% for the week.

- The Dow Transports gained just 0.01% on Friday, but still lost 1.22% for the week.

- The Philly Semis gave back a nasty 3.15% on Friday to drop 1.49% for the week.

- The KBW Bank Index gained just 0.07% on Friday and much nicer 1.89% for the week.

On Friday, six of the 11 S&P sector SPDR ETFs closed out the session in the green, led higher by defensives for a change. Health Care XLV and the Staples XLP were the day's winners. Technology XLK had a rough day as Marvell Technology MRVL was pasted for an 18.6% loss and Dell Technologies DELL took a beating of 8.9%.

For the week, just five of the eleven S&P sector SPDR ETFs traded higher. Cyclicals led the way for the week as Energy XLE gained 2.55%. Defensives may have had a nice Friday, but they had a rough week. The Staples and the Utilities XLU both surrendered 2% or more for the five-day period.

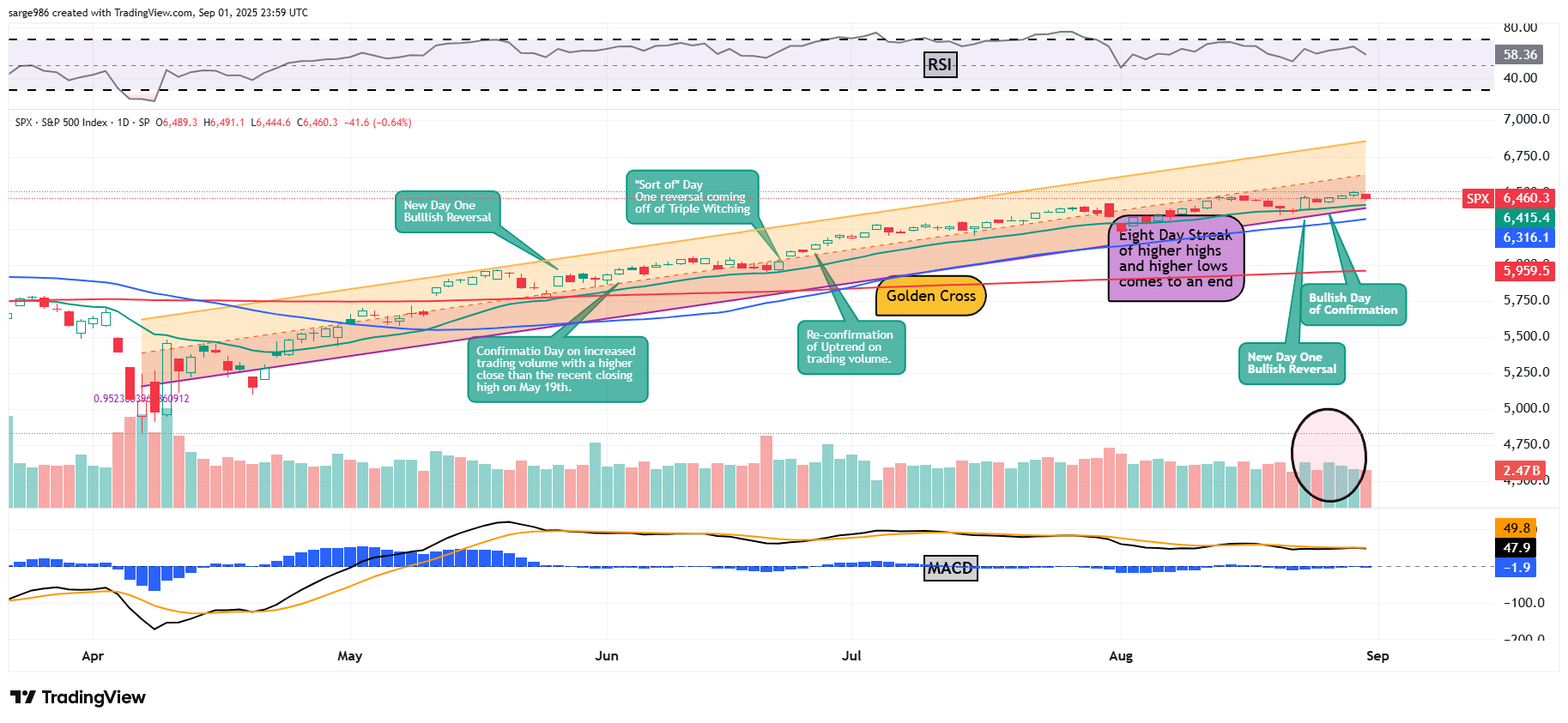

The Chart

Readers will note that trading volume ebbed over the final three days of the past week as those folks who found time for the beach hit the road. The uptrend confirmed last Tuesday remains in effect until it doesn't. That's really all you need to know right now. Friday did not undo the set-up created earlier in the week.

Readers will note that support for the S&P 500 has consistently been found at the 21-day exponential moving average. The swing crowd is still buying any market weakness at that line. As I mentioned last week, professionally managed money remains invested and has been quiet. Relative Strength has remained robust without getting close to being technically overbought. That's a continuing positive.

The daily Moving Average Convergence Divergence, below the chart, still paints a less than bullish picture, but is looking better than it has. The histogram of the 9-day exponential moving average is still in negative territory, but not by much. That remains a potentially bearish short-term signal. The 12-day EMA is still slightly below the 26-day EMA. Those lines remain poised for a bullish crossover, but that trigger has not yet been pulled. This is a positive chart. Just not overwhelmingly so.

Earnings

Second-quarter earnings season has just about, with a few exceptions, wrapped up. According to FactSet, for the second quarter, with 98% of S&P 500 member companies having already reported, 81% of member companies have beaten earnings expectations, while 81% have also surprised the street on revenue generation.

To date, year-over-year earnings growth across the S&P 500 is currently standing at 11.9%, which is up sharply from just 4.8% a couple of months ago. Q2 revenue growth now stands at growth of 6.4%, up nicely from 4.2% a couple of months back. For the second quarter, Communication Services easily led the way, having grown earnings by a stunning 45.6%, followed by Tech at +22.6%. Three sectors suffered a year-over-year contraction in earnings, easily led lower by Energy (-18%). The Materials and Staples also finished on the wrong side of the growth ledger.

For the full calendar year of 2025, Wall Street now sees S&P 500 earnings growth at 10.6%, up from 9.9% a month ago. Expectations for full year revenue growth are now at 6%, up from 5.6% over that same time frame.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 22.4-times 12 months' forward looking earnings. That stands well above the five year average of 19.9-times for the index and its ten year average of 18.5 times. The S&P 500 also ended last week trading at 27.9 times trailing 12 months' earnings. That also stands well above the five-year (25-times) and ten-year (22.6-times) averages for the index.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the third quarter up to growth of 3.5% (q/q, SAAR) from 2.2% earlier. Among other regional central bank district branches running close to real-time gross domestic product models, the New York Fed's estimate for Q3 growth now stands at 2.22%, up from 2.01%. The Cleveland Fed's model for the third quarter was actually revised. I guess someone is home. The Cleveland model stands at growth of 1.94%, up from 1.93%. I kid you not. The St. Louis Fed model now stands at a paltry 0.54%. Safe to say that there is no consensus.

Fed Funds Futures

Coming out of the personal consumption expenditure data, Fed Funds futures trading in Chicago are now pricing in a 90% probability for a quarter-percentage point rate cut on Sept. 17. According to these markets, there is now just a 48% likelihood for a second quarter point rate cut on Oct. 29. That second cut has now been pushed back out to Dec. 10 with an 86% probability. There is currently an additional three-quarters of a percentage point worth of rate cuts priced in (72% likelihood) for calendar year 2026.

On The Docket...

On to the workweek, gang as we focus on August job creation. The Fed will be out and about, but not in force. There are some earnings to be fully aware of. That said, the week will build, and trading volume may remain light as we approach this Friday's numbers.

......The domestic macroeconomic calendar will build into Friday but isn't exactly thin ahead of the big day. This morning, the Institute for Supply Management will release its Manufacturing PMI for August followed by the Census Bureau's release of Construction Spending for July. Wednesday will bring us the JOLTs data for July job openings and July job quits.

After that, "Jobs Week" kicks into high gear with the ADP Employment Report's publication for August on Thursday morning. This will be followed by a final revision to Q2 Non-Farm Productivity and Q2 Unit Labor Costs as well as the ISM's Service Sector PMI for August. Then comes Friday, when the BLS will go to the tape with its labor market survey results for August. In focus will be job creation followed by participation and wage growth. The U-3 Unemployment Rate will garner some attention as well as an increase is expected.

..... The Fed won't be everywhere this week. That's normal for them during holiday-shortened weeks. On Wednesday afternoon, we'll hear from Minneapolis Fed Pres Neel Kashkari who is someone we have not heard from in a long while. His opinions will be welcome. Minneapolis does not vote on policy this year, but will in 2026. On Thursday afternoon, New York Fed Pres John Williams will speak publicly followed by Chicago Fed Pres. Austan Goolsbee that evening. In addition to public appearances, the Fed will publish its eight times a year Beige Book on Wednesday afternoon.

..... The earnings calendar is rather light this week but will heat up to a mild degree on both Wednesday and Thursday. Among high-profile firms that will report their quarterly numbers this week, Zscaler ZS will bat lead-off this evening. Wednesday morning will bring us results from Campbell's Soup CPB, Dollar Tree DLTR and Macy's M followed by American Eagle AEO and Salesforce CRM on Wednesday afternoon. Thursday morning, we'll hear from the likes of Toro TTC, followed by Broadcom AVGO, DocuSign DOCU and Lululemon Athletica LULU after that day's closing bell.

Economics

(All Times Eastern)

08:55 - Redbook (Weekly): Last 6.5% y/y.

09:45 - S&P Global Manufacturing PMI (Aug-F): Flashed 53.3.

10:00 - ISM Manufacturing Index (Aug): Expecting 48.7, Last 48.0.

10:00 - Construction Spending (Jul): Expecting 0.1% m/m, Last -0.4% m/m.

The Fed

(All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: SIG (1.24)

After the Close: ZS (.80)

At the time of publication, Guilfoyle had no position in any security mentioned.