Copper and Crude Oil Prices Offer Clues on Future of Inflation

We can’t see into the future better than anyone else can, but overcrowded trades are always temporary.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

According to the "Commitments of Traders Report," market participants are overwhelmingly positioned for higher inflation (long commodities), higher interest rates (short treasuries and short yen) and higher growth (long stocks). But with everyone on the same side of the boat, what if something tips it the other way, causing simultaneous position squaring?

We can’t see into the future better than anyone else can, but overcrowded trades are always temporary, and their unwinding can cause uncivilized markets. We saw a mini version of this play out late last summer. We don’t know if we will get a repeat or something much worse, but we know the circumstances are ripe. Two markets that might give us clues are those for crude oil and copper.

These commodities offer clues into economic strength and demand for goods and services. Further, they tend to be market leaders. For instance, before the pandemic, crude oil futures began to plummet. It was a bit of a mystery at the time, and many analysts couldn’t offer reasonable explanations. However, soon after, governments began shutting down their economies and the rest of history. Similarly, oil futures rallied sharply well before Russia ever invaded Ukraine. Lastly, in May 2024, the copper market reversed from all-time highs, suffering one of the most significant sell-offs in history; other risk assets followed just a few months later.

Crude Oil

In a previous article, we noted that the sudden and swift rally in oil futures in early January was likely the result of inflation hedges coming into the market. For instance, portfolio managers or wealthy investors wishing to hedge their inflation risk often put money to work in commodity funds; those investment dollars are then used to purchase futures contracts into commodities such as corn, crude oil and cattle. The result is that the beneficiary commodities rally as a single asset without reverting to underlying fundamentals. Ironically, inflation hedges can cause the same inflation they aim to hedge.

The oil market is approaching a critical crossroads. Since peaking in March 2022, it has consistently made lower highs. The recent rally was stopped in its tracks by the 200-week moving average at $80.00, a telltale sign of a resumption of the downtrend. The previous downtrend line from which oil broke out earlier this month will now become supportive at $73.00. If prices slip below this level, I suspect we will quickly see the mid-to-low $60.00s again in short order.

Support at $65.00 has managed to reject each sell-off since the March 2022 euphoria, but the more times we knock on the door, the more likely it is to open. A sluggish relative strength index and weak fundamental backdrops lead us to believe the most likely scenario will be a slide to a multi-year pivot line near $50.00! If oil prices retreat to such levels, it would signal underlying economic weakness and deflation. On the other hand, if $73.00 holds, the inflation bulls might be on the right side of history.

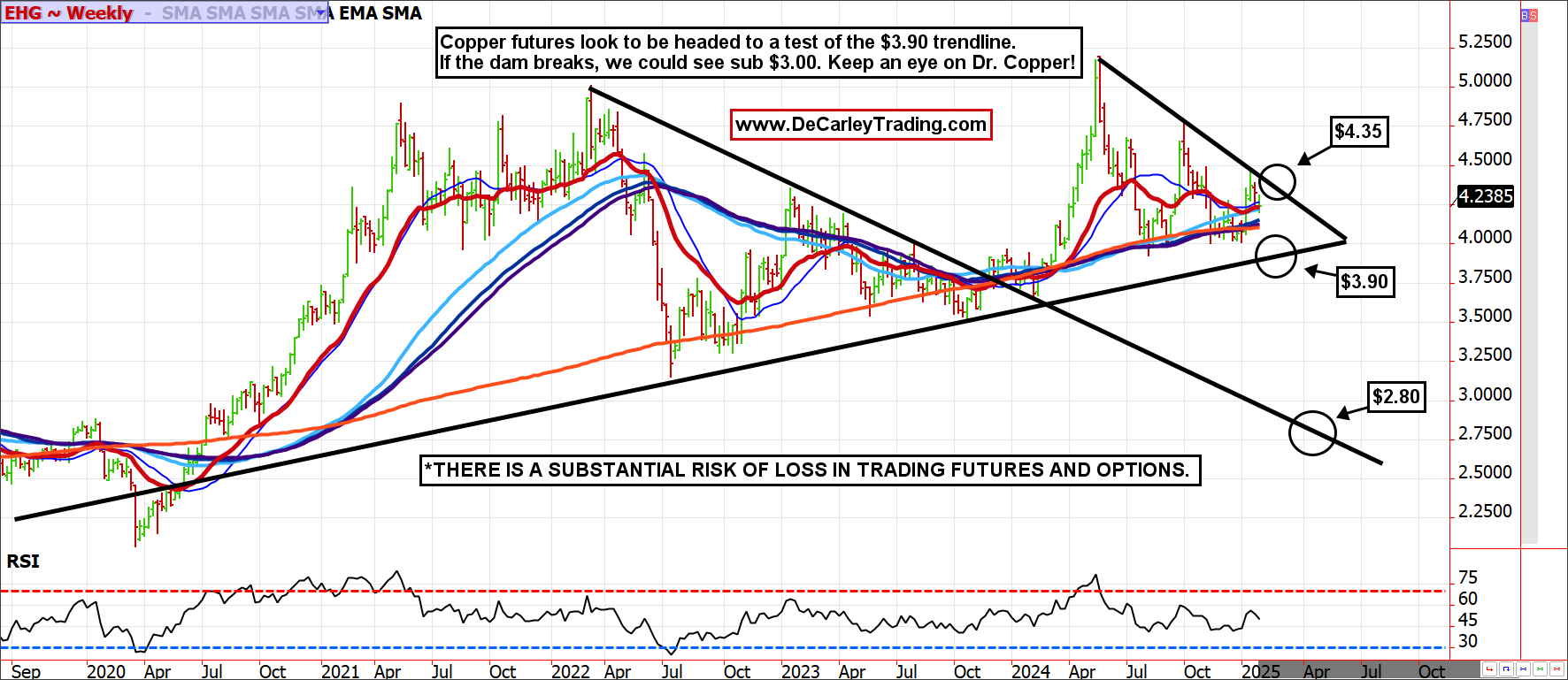

Copper

The recent copper rally was met with selling at a downtrend line near $4.40. Assuming this high holds, as expected, we should see prices retest the lower end of the technical pattern just under $4.00. What the market does at this level would be quite telling. Should prices break below $3.90, the door would be open for vastly lower prices. More importantly, such a breakdown would signal slower economic growth and deflation.

Conclusion

If this is an inflationary environment, as traders are positioned for, we should see copper climb above $4.35 and oil hold $73.00 (and eventually break above $80.00).

Yet, if market participants have their macro thesis wrong, the talking points will shift from inflation to deflation on a break below $3.90 in copper and $65.00 in oil.

At the time of publication, Garner had no positions in any securities mentioned.