The Buffett Indicator Reveals a Lopsided Market

The towering and narrow leadership of large-cap technology is wobbling above a picture of moderating domestic economic growth.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

- Financials may be showing signs of rolling over

- Technology continues to roll higher

- The low S&P dividend yield (1.17%) represents a challenge to intermediate-term stock market returns

As we look at the market today, financials appear to be showing signs of rolling over as technology continues to rocket higher. And the low S&P dividend yield of 1.17% represents a challenge to intermediate-term stock market returns.

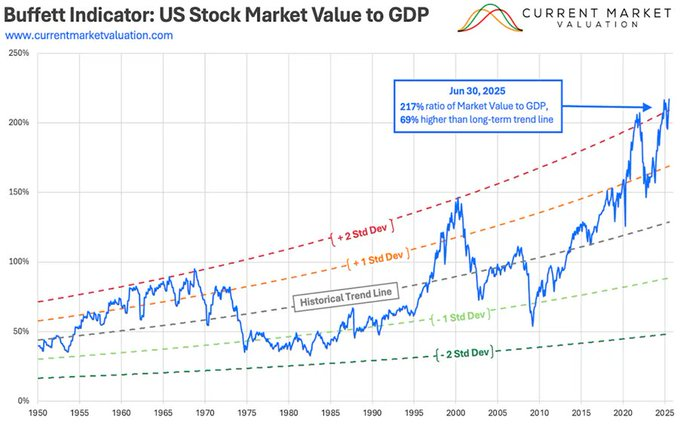

But there's something else worth watching: The ratio of the total U.S. stock market to the nation's gross domestic product. I'm talking about the Buffett Indicator (U.S. total stock market value/GDP), which now stands at two standard deviations above its long-term trendline. The indicator is now at a record high of 217%:

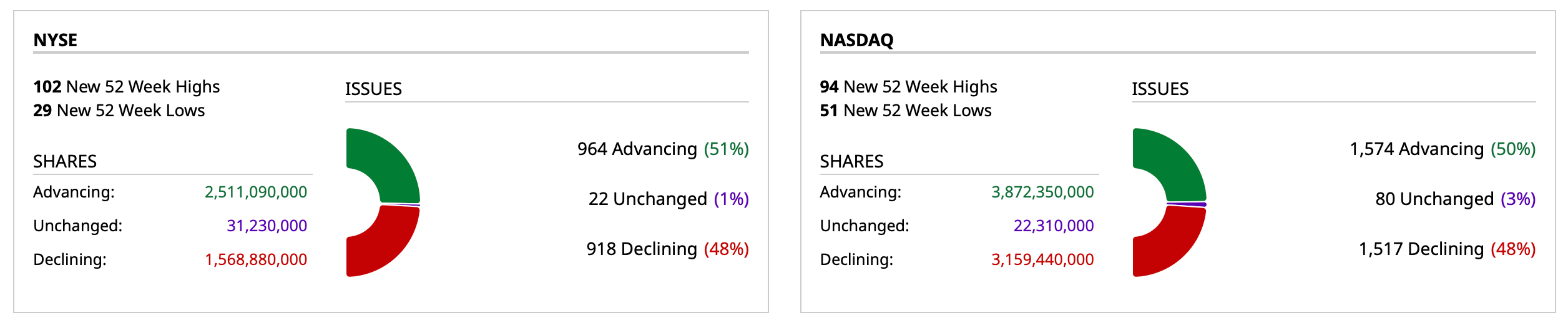

Meanwhile, financials have been notably weak in recent days and market breadth has eroded (yesterday advancers were again flat with decliners — though the averages rose nicely):

The narrow leadership of large-cap technology continues in a market dominated by passive products and strategies that worship at the altar of price momentum.

This is occurring amid continued signposts that domestic economic growth is moderating, inflation remains sticky (and cumulative or stacked inflation since 2020 piles up) and our politicians (on both sides of the aisle) are indifferent to rising deficits and expanding debtloads.

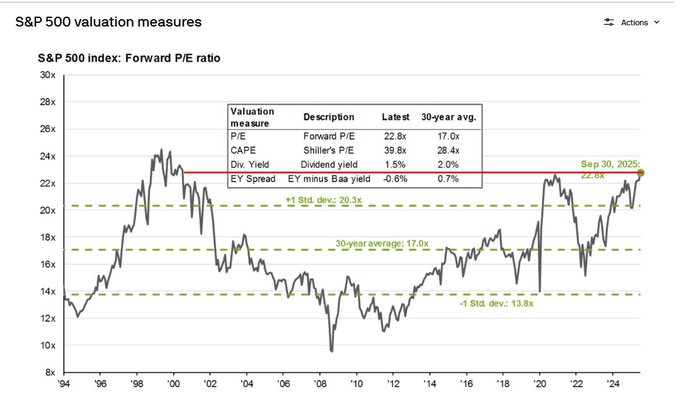

And this is happening at a point in time in which most traditional valuation metrics approach the 98th percentile. Today's price-earnings multiple on the S&P Index is 23-times — the highest in 26 years and compared to the 30-year long-term average of only 17-times:

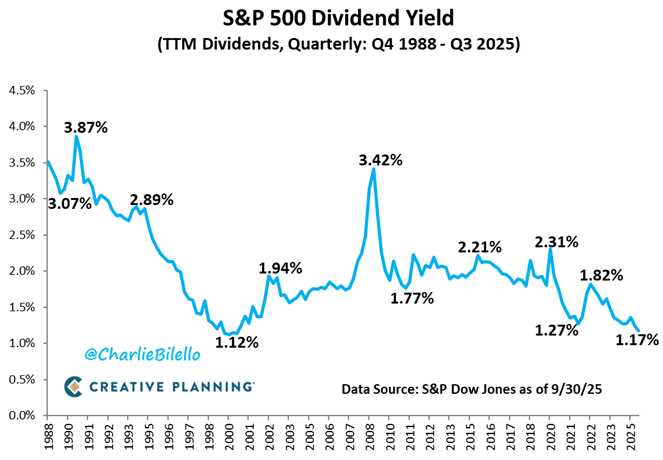

Finally, I would note (as few have noted!) that, over time, dividends have contributed about one third of the total return for stocks — with the rest coming from capital appreciation. Today the S&P Dividend Yield is only 1.17% — the lowest read in 2 1/2 decades. The difference between the S&P dividend yield (1.17%) and the risk free rate of return (on the 10-year Treasury note, which yields 4.10%) is also at a multiple-year wide level. By definition, an extremely low market dividend yield becomes a bonafide hurdle to intermediate-term stock market returns:

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.