Bond Markets Flash a Global Warning

Let's see how reckless fiscal policy across developed economies is getting punished, why tariff-driven federal revenues are in question, and how Arm Holdings and Lam Research just took the semis into the abyss.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The bond market is telling us something. Not just here. The bond market "meltdown," or if one works in financial media, the "yield rally," is not unique to U.S. markets. Yes, yields are rising across the slope of the U.S. Treasury curve for specific reasons. That said, reckless fiscal policy across developed economies is being punished on a global scale. Oh, and seasonality is a part of this as well. We all know that September is, on average, our toughest month. Since 1950, September has returned an average of -0.7% to the S&P 500.

Additionally, still since 1950, the S&P 500 has posted a gain for the month only 44% of those years. This is significantly worse than February's positivity rate of 54% over that same time frame, which is second worst. Well, bonds have a rough go of it this time of year, as well. According to Barron's, the iShares International Treasury Bond ETF IGOV, which holds sovereign debt securities from across the developed world, has lost 1.46% on average in September over the past ten years. Stay domestic? The iShares 20+ Year Treasury Bond ETF TLT has lost an average of 2.6% for the month of September over those same ten years.

This Year Is Different?

Well, this year, domestically at least, there was a catalyst, but the long end of the curve has been waving for help for a few months now. On Friday evening, an appeals court upheld a ruling by the U.S. Court of International Trade that the lion's share of Pres. Donald Trump's tariffs was an overreach of executive authority and violated the law. Return those tariff-driven federal revenues? That could be problematic for a nation already showing signs of fiscal distress.

From just April's "Liberation Day" through the end of July, tariffs have provided the Treasury with revenue of $94.4 billion, up 293% over the same period a year ago. The Congressional Budget Office has estimated that tariffs, if left in place, would reduce federal budget deficits by $4 trillion over ten years. That's not even close to chump change and would be helpful in creating budgets for not just this administration but for those that follow... as long as U.S. consumers remain the force that they have been.

Keep in mind, also, as mentioned above, that this is global. If investors are losing faith in mature economies around the planet to be able to properly service their debt while carrying on with their increased deficit spending habits, then capital will come out of those markets. If the U.S. is about to lose a source of revenue that investors had started to price in, there will be a partial loss, at least for the time being of some safe haven status.

The president has said that his administration will take the Friday night ruling to the Supreme Court. A lot is riding on that outcome. While we await such a final decision, the U.S. Thirty Year long bond presses up against a yield of 5%, which has been a key level of support (not resistance) for that instrument for nearly 20 years. Globally, U.K. 30-year paper is trading at its lowest levels since 2006, French 30-year paper is trading at its lowest levels since 2009, and German 30-year paper is trading at its lowest level since 2011.

A Bright Spot?

The Institute of Supply Management released that agency's Manufacturing PMI for August on Tuesday. While the headline print crossed the tape at 48.7, which was a sixth consecutive month of overall decline and a 32nd month of overall decline in the past 34, the single most important component actually landed in a state of expansion. The "New Orders" component crossed the tape at 51.4. The "50" level is the border between expansion and contraction in these surveys and this was the first month where New Orders printed on the right side of 50 since January.

Are we any closer to getting ourselves out of the woods and ending this long U.S. manufacturing sector recession / depression? The New Orders print doesn't hurt, but there is plenty of capacity available as Backlogged Orders fell to an anemic 44.7 and have printed in s state of contraction for 35 months in a row. Manufacturing-based employment also contracted for a seventh straight month while manufacturing prices remained red hot at 63.7. The ball did indeed roll in the right direction, but just by an inch.

Marketplace

Domestic equity markets sold off hard from the get-go on Tuesday morning. In fact, I was fairly sure early on that U.S. markets were headed for a rather ugly session and that we would have to mark a "Day One" bearish reversal. Just around lunchtime, investors, and traders, spurred on by algorithmic bottom-feeders bought the dip. Stocks rallied sharply over the final four hours of the regular session to still close down for the day. That said, in no way was Tuesday the bloodbath that the financial media made it out to be.

By day's end, the S&P 500 had surrendered 0.69%, while the Nasdaq Composite gave up 0.82%. Among the mid-majors, the Philly Semiconductors lost 1.12% and the KBW Banks gave up 1.06%. Arm Holdings ARM and Lam Research LRCX led the semis into the abyss while Goldman Sachs GS led the banks lower.

Breadth

Nine of the 11 S&P sector SPDR ETFs closed out the Tuesday session in the red, led lower by the REITs XLRE and Technology XLK. Only Energy XLE and Health Care XLV finished the day in the green and not by much. The market did not appear to show favor toward any type of sector such as growth, cyclicals or defensives.

Losers beat winners by a rough 2-to-1 margin at both the NYSE and at the Nasdaq. Advancing volume took a 40.1% share of composite NYSE-listed trade on aggregate trading volume that increased 12.1% on day over day basis. That sounds like a "Day One" bearish reversal of trend to me, right? Check this out...

Advancing volume took a 49.8% share of composite Nasdaq-listed activity on aggregate trade that increased 6.1% on a day-over-day basis. Do we have a "Day One?" Not so fast my friend. Declining volume took just a 48.9% share of Nasdaq-listed trade. (No, that does not equal 100%. The rest of the volume was sideways.)

Hence, according to what we saw at the NYSE and across the membership of the S&P 500, we would have such a "Day One" but the fact that advancing volume outweighed declining volume across the Nasdaq does throw some serious doubt into that thinking. That does not mean that we do not have a downtrend in place that actually started Friday. This does, however, decrease the statistical probability of such an event. If only there were an even greater catalyst scheduled for later this week. Hmm...

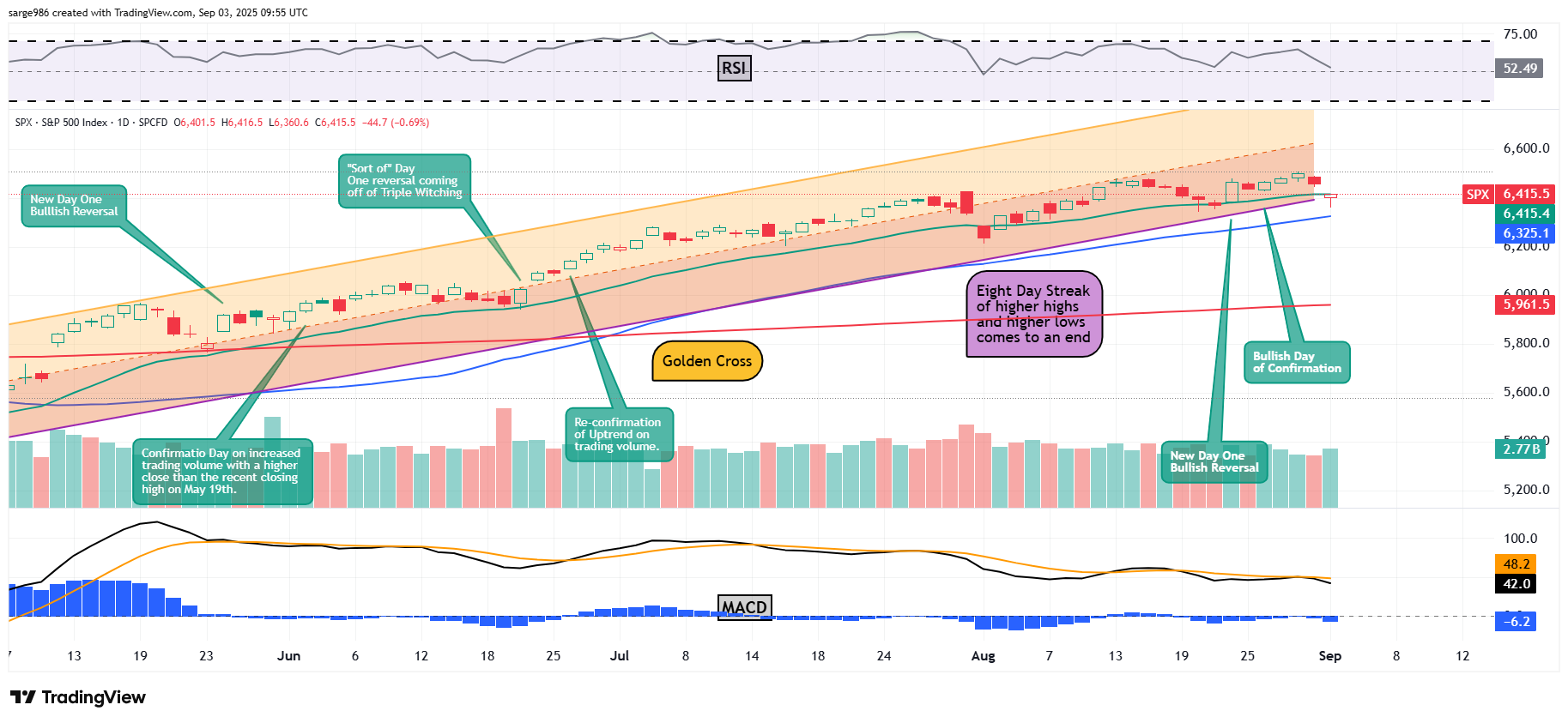

The Chart

Note that small black circle that I placed around Tuesday's candlestick for emphasis? That's called a hammer doji and it is a one-day bullish technical pattern that obviously signals a positive intraday reversal lime we saw on Tuesday but often signals some carry-through of that positivity into the next morning.

I think it also key that the index, while losing the 21-day exponential moving average, did in fact, maintain contact with that line. That may keep the swing crowd engaged. Key, too, is that at the lows, Tuesday did not take out the lows of Aug. 21 that produced the bullish Day One on the 22nd. That may have been crucial. Like a good pundit, I'll let you know after the fact and pretend I knew what was happening all along.

Google This!

Shares of Alphabet GOOGL popped overnight as a federal district court decided that in order to remedy Google's supposed monopoly on internet search, the actions to be taken were not nearly as severe as had been feared. Alphabet will not have to sell its Chrome browser, won't be barred from paying Apple AAPL to make Google the default search engine on its devices and will not be prevented from making payments to distribution partners to preload Google Search, Chrome or the firm's GenAI products.

Alphabet will, however, be barred from entering Google into exclusive contracts that relate to the distribution of Google Search, Chrome, Google Assistant and the Gemini App. Google will also have to share its search data with competitors. Readers will see in the disclosure below that I am long GOOGL. That is not some kind of investment that I haven't written about. That position is very small and just the result of overnight day-trading.

Nvidia Rumor: Denied!

Nvidia's NVDA verified X (Twitter) account, Nvidia Newsroom, posted a public denial on Tuesday of rumors that the chip designer was becoming supply constrained and had sold out of H100 and H200 chips.

The post reads: "As we noted at earnings, our cloud partners can rent every H100 / H200 they have online - but that doesn't mean we're unable to fulfill new orders. We have more than enough H100 / H200 to satisfy every order without delay. The rumor that H20 reduced our supply of either H100 / H200 of Blackwell is also categorically false."

Look For the Fed to ...

The Fed is expected to suspend its quantitative tightening program on Sept. 17 in addition to the making a quarter-point cut to the target range for the Fed Funds Rate as a means toward preserving liquidity with bank reserves still above levels that might make economists uncomfortable and as the economy transitions toward something different with a steeper yield curve in place. The Fed might be smart to leave its $6.6 trillion balance sheet as is for at least a little bit. Equities would like that.

Economics

(All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.69%.

07:00 - MBA Mortgage Applications (Weekly): Last -0.5% w/w.

10:00 - JOLTs Job Openings (Jul): Last 7.437M.

10:00 - JOLTs Job Quits (Jul): Last 3.142M.

10:00 - Factory Orders (Jul): Expecting -1.2% m/m, Last -4.8% m/m.

4:30 - API Oil Inventories (Weekly): Last -974K.

The Fed

(All Times Eastern)

1:30 p.m. - Speaker: Minneapolis Fed Pres. Neel Kashkari.

2:00 - Beige Book.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: CPB (.57), DLTR (.41), M (.19)

After the Close: AEO (.20), GTLB (.18), HPE (.41), CRM (2.78)

At the time of publication, Guilfoyle was long LRCX, GOOGL, NVDA equity.