Bombs Dropped, So Did Oil. Are Gold and Silver Next?

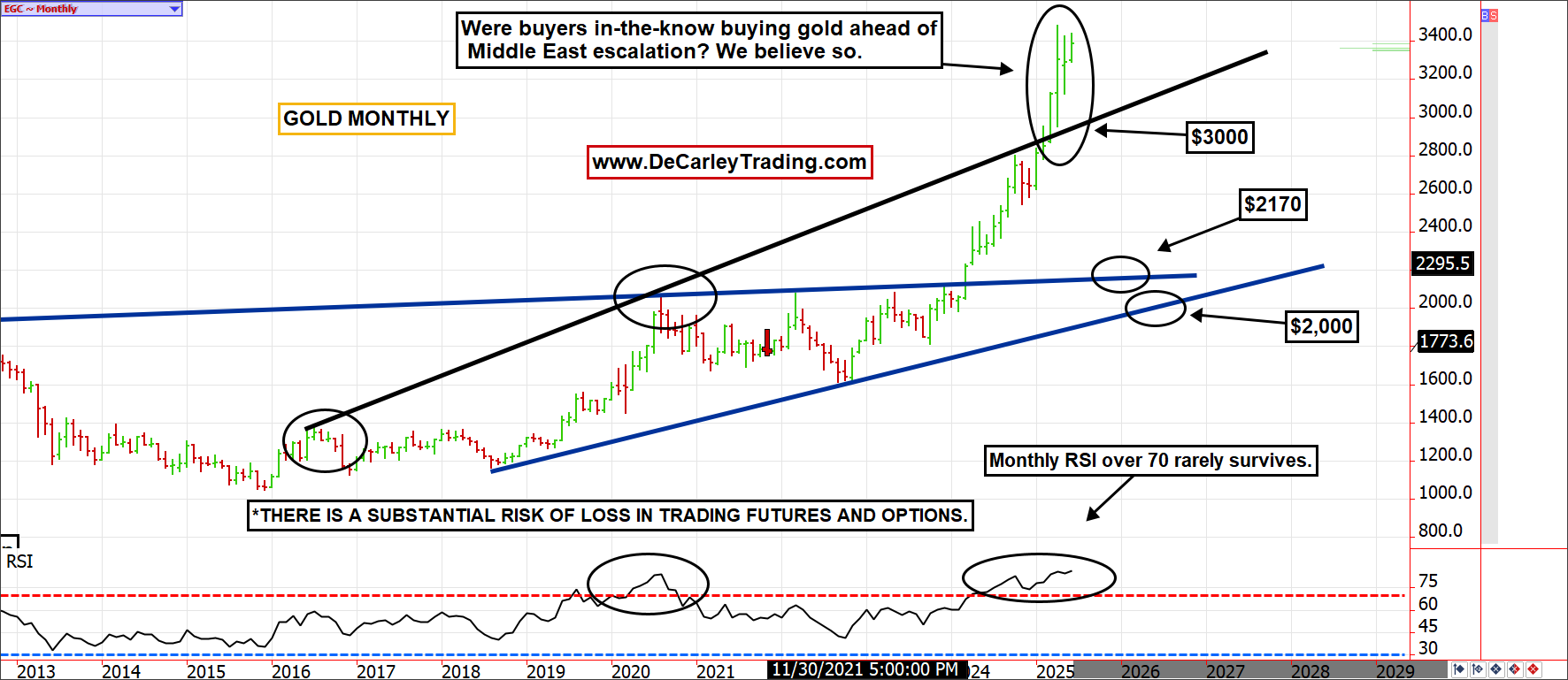

Were buyers in the know buying gold ahead of the Middle East escalation? We believe so. Markets coloring outside of the lines generally come back into line.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A muted response by the oil and precious metals markets to last weekend’s events in the Middle East may seem surprising at first, but this is a common occurrence. Markets are forward-looking and habitually suffer from buy-the-rumor-sell-the-fact price action.

Another way to look at this is to consider market prices in what is believed to be a worst-case scenario; however, reality is generally less severe than the most pessimistic view, allowing the market to revert to a more fundamentally sound price.

What's more, just because we, or the public, aren’t aware of a particular event brewing beneath the surface, others are likely cognizant and are acting before the news hits the airwaves.

Silver

We don’t often discuss silver. This isn’t because it is an unpopular commodity; it is because it is a miserable and uncivilized market.

I’ve been in the futures and options brokerage business for over two decades, and I can’t recall too many traders finding a way to pull money out of the silver market successfully. It is the exact opposite. To be clear, I’ve seen traders make a massive amount of money in a short amount of time trading silver futures, but they never keep it. I’ve also seen traders slowly build their trading account with profitable silver trades, but those, too, tend to end in disaster.

There are several explanations for this, but the most glaring aspect is the nature of the price action. It tends to move all at once and for no reason. Thus, it is a market in which you can’t use stop loss orders because they are sure to be elected, but trading without stops is sure to bring catastrophic losses at some point.

Also, options are very expensive and are on the thin side. The lack of liquidity isn’t due to a lack of market participants; it is (in my humble opinion) the byproduct of the CME Group listing too many strike prices (and maybe even expirations).

One final thought: We are now discussing silver because it has recently reached a 13-year high. While many are touting this as an exciting and bullish time for silver, I can’t help but think about the fact that this means anyone who bought it 13 years ago is just getting their money back after over a decade of hardship.

Silver doesn’t pay interest to its holders, and it took a 50% haircut before returning to its 13-year high, which means the opportunity cost of an inflow yielding asset is significant. Even worse, if you were unlucky enough to have bought the 2011 highs near $50.00 per ounce, you are still down over 25%.

Despite widespread belief, silver is better as a trader's market, not a buy-and-holder’s market. Silver, like most assets, has benefited from a global economy flush with cash. Too many dollars chasing too few goods have left nearly every asset class dramatically higher in a post-pandemic economy. Thus, appreciation can only be partially attributed to fundamentals (industrial and asset diversity).

In addtion, it is currently 80% negatively correlated to the U.S. dollar. This means if the dollar recovers from multi-year lows and its long-term trendline, as we expect, it will put a knife through the hearts of the silver bulls. Summers have been historically treacherous for precious metals bulls; if you made money on the way up in silver, be sure to lock it in or protect it.

Gold

Like silver, gold’s fate will be primarily tied to the valuation of the U.S. dollar. We’ve taken multiple deep dives into this commodity this year, so we will keep our comments relatively brief.

In February and March, the gold market experienced a parabolic surge after breaking through a decade-long uptrend. At the time, in our view, it wasn’t easy to justify the move fundamentally. The bulk of the rally came before the so-called “Liberation Day,” months before the Israeli-Iran flare-up, and before anyone could have conceived of what was to happen last weekend. Yet, aggressive gold buyers were scrambling to position themselves on the long side, regardless of price or risk.

I suspect many of these buyers, who were most active in the overnight U.S. session, were overseas buyers who either knew or had reason to suspect what we all learned about in June. With the benefit of hindsight, it is obvious why gold buyers were willing to break a decade-long uptrend line to take prices parabolic. Nevertheless, markets coloring outside of the lines generally come back into line.

As is often the case, the gold rally appears to have occurred before the actual news was released. Therefore, it is likely to give some or all of it back now that the masses are aware of the new reality. In other words, the late-comer buyers, those who were compelled to buy after bombs started dropping, are adding liquidity to the market, allowing those with prior knowledge to exit comfortably. Once that process runs its course, we will likely see a fallout.

I heed the same advice for gold bulls; this is not a time for complacency or to step on the gas; protect or lock in profits. If I learned anything during the financial crisis, it was that a person’s net worth is just a number on paper unless you sell assets. In the end, cash is king.

Crude Oil

Iran is a marginal producer under significant sanctions; it is unlikely to be capable of derailing the trend of a well-supplied oil market. Trade has priced in a near elimination of all Iranian barrels of oil from the market, yet we haven’t seen a single barrel removed from supply. In short, the market has priced in the worst-case scenario for a supply disruption, but reality will likely be something far less impactful.

The outlier event would be the closure of the Strait of Hormuz; while we can never say never, it is a very low-probability event. This is something that is threatened early and often but has never actually occurred. Further, doing so would be akin to Iran shooting itself in the foot.

The vast majority of Middle East oil rallies fail, making way for new lows. We suspect that is precisely what we will see in the coming weeks or months. Remember, $65.00 has been a historically significant price point; even if this marks the beginning of a new bull market (which we do not believe), we should at least retest this level. Furthermore, if prices slip below $65.00 again, the bulls will likely begin to liquidate their positions. Despite the market taking a detour, the low-$50.00s to high-$40.00s range remains in play.

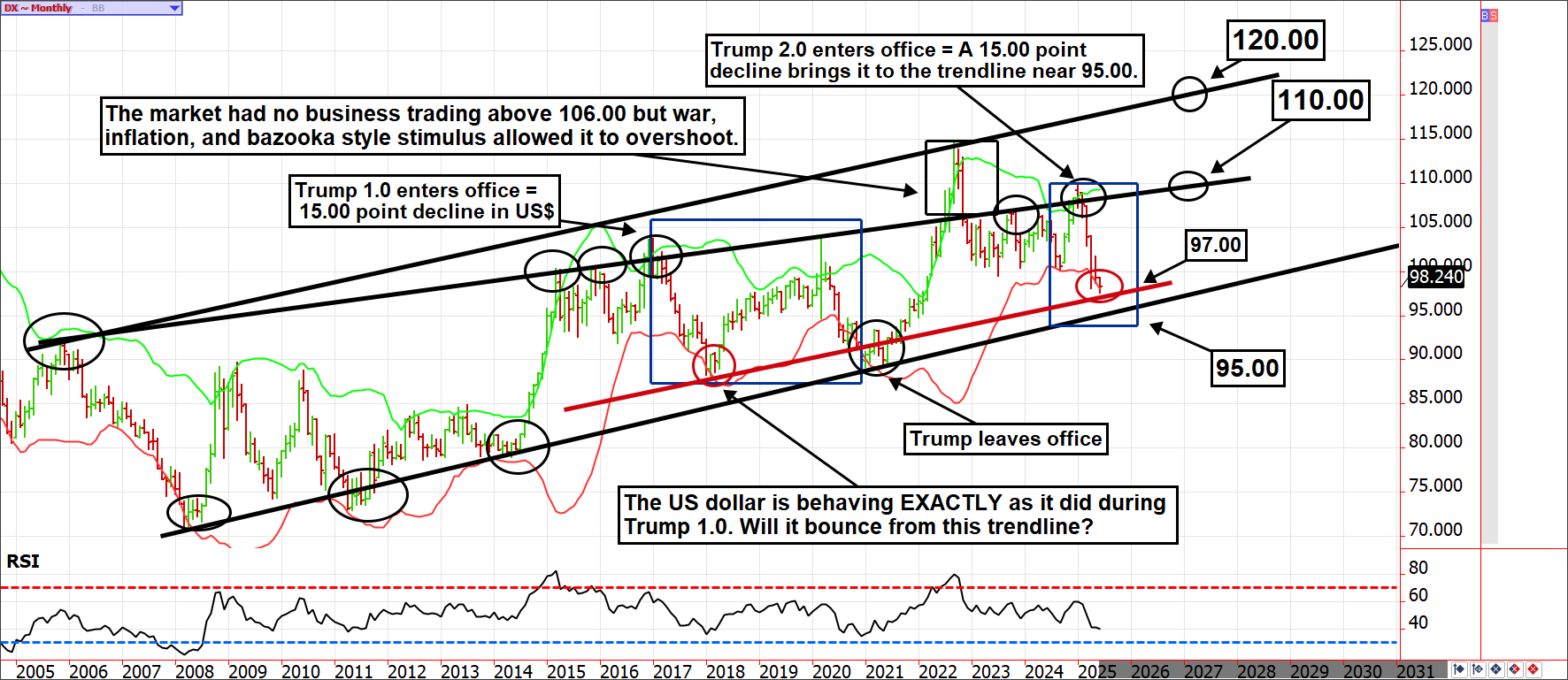

U.S. Dollar

We’ve recently written a detailed analysis on the dollar, outlining why we believe the bearish sentiment is becoming too saturated to allow for lower prices (all the sellers have already acted), so we will keep it brief.

It is worth noting that the path of the greenback during Trump 2.0 is nearly identical to that of Trump 1.0. If we are to continue mimicking 2017, the dollar should fund support on the red trendline in the accompanying monthly chart near 97.00, triggering a significant rally. But if that level fails, the odds of support near 95.00 holding to pave the way for a stunning dollar rally as the overcrowded short position on the dollar is unwound. Once the process begins, we expect the dollar index to reach heights in the 110.00 area. This would cause significant damage to asset prices, particularly commodities such as gold, silver, and crude oil.