Bitcoin's on the Move, Banks in Focus, Trump Sets Sights on Mexico

President plays hardball on tariffs, crypto's in the spotlight, Apple just can't keep pace with Nvidia and Microsoft and check out my Ramaco Resources play.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

None of us were taken by surprise. It was the main reason why there was some mild pressure on U.S. equity prices this past Friday. It was the primary reason why those same equities, for the most part, experienced a "down" week over the past five trading sessions despite some record setting high closes for both the S&P 500 and Nasdaq Composite. Throughout the week, Pres. Trump issued letters outlining his "deals" or tariff rates for nations that had not reached out and made agreements on trade with the U.S. by the self-imposed July 9 deadline.

The president addressed those letters to the heads of state of Japan, South Korea, Canada, Brazil, the Philippines and others, more than two dozen nations in total. Tariff rates of 25% to 40% were "threatened" to be implemented on Aug. 1st if agreements are not reached with those respective nations by then. The president also targeted imports of copper. The "red" metal will face tariffs of 50% when imported, also by Aug. 1.

All of that, U.S. financial markets handled with a certain level of grace, as if they either did not believe that these tariffs would ever go into effect, might not be as daunting as advertised or somehow, the U.S. economy would wind up in a better place. While the U.S. economy may or may not end up in a better place, the intent is obviously an attempt to create a more prosperous environment for lower to middle-class American laborers. The other side of that coin would be that there is almost no way to do this without harming the profit margins of U.S. multinational corporations that had become quite used to benefiting financially through the use of inexpensive foreign labor.

Hardball

So, what exactly was the not so surprising reason or reasons behind the pressure that investors started to experience late last week? That's easy. Those were the anticipated letters still to be sent to the European Union and Mexico. Those letters were made public over the weekend. On Saturday, the president revealed in letter form 30% tariffs on goods imported from the E.U. and Mexico. The letters that were posted to Pres. Trump's "Truth Social" account were addressed to Mexican Pres. Claudia Sheinbaum and European Commission Pres. Ursula von der Leyen.

For those keeping score, Mexico is the world's leading single exporter to the U.S. In 2024, imports from Mexico totaled roughly $505.9 billion resulting in a trade surplus for Mexico of $171.8 billion. For the sake of comparison, 2024 imports from China totaled about $462.6 billion, resulting in a trade deficit for the U.S. of $295.4 billion. Canada is the third largest exporter to the U.S. But the E.U., in aggregate, exported about $605.8 billion in goods to the U.S. in 2024. This resulted in a U.S. trade deficit of "just" $26.9 billion. which is much smaller than the deficits seen earlier in this paragraph.

They Said (or Wrote) What?

"Mexico has been helping me secure the border, BUT, what Mexico has done is not enough." - U.S. President Donald Trump

"Imposing 30 percent tariffs on EU exports would disrupt essential transatlantic supply chains. to the detriment of businesses, consumers and patients on both sides of the Atlantic." - European Commission Pres. Ursula von der Leyen

"Let this be a lesson to other countries - earnest, good faith negotiations can produce powerful results that benefit both sides of the table, while correcting the imbalances that plague global trade." - U.S. Treasury Sec. Scott Bessent (after praising the UK for "smartly" securing "an early deal.")

Weekly Numbers

What the major to mid-major U.S. equity indexes did last week as tensions over a potential trade war escalated. It really was not nearly as rough as one might have expected. In fact, if one was in the right stocks, it was downright good.

- The S&P 500 gave up 0.33% on Friday and 0.31% for the week.

- The Nasdaq Composite gave up 0.22% on Friday and just 0.08% for the week.

- The Nasdaq 100 lost 0.21% on Friday and 0.38% for the week.

- The Russell 2000 gave back 1.26% on Friday but just 0.63 for the week.

- The S&P Smallcap 600 surrendered 1.03% but just 0.27% for the week.

- The S&P Midcap 400 lost 0.84% on Friday and 0.59% for the week.

- The Dow Transports gave up 0.66% on Friday but gained 1.01% for the week.

- The Philly Semis gave back 0.21% on Friday making for a loss of 0.87% for the week.

- The KBW Bank Index gave up 0.52% on Friday and a nasty 1.43% for the week.

On Friday, nine of the 11 S&P sector SPDR exchange-traded funds closed out the session in the red, led lower by the Financials XLF and Health Care XLV ahead of this week's upcoming banking earnings releases. Energy XLE was the top performing sector of the day.

For the week, only five of the 11 S&P sector SPDR ETFs traded higher, led by again by Energy and the Utilities XLU. The Financials, Communication Services XLC and the Staples XLP all surrendered at least 1.6% for the five-day period.

It is notable that during the week, chip designer Nvidia NVDA became the first publicly traded company ever to hit a market cap of $4 trillion. As Friday's closing bell finished ringing, Nvidia was worth $4.02 trillion, Microsoft MSFT was in second place at $3.74 trillion and Apple AAPL had all but fallen completely out of contention for the top spot at $3.153 trillion.

Interesting Surplus ...

On Friday, the U.S. Treasury Department reported a budget surplus of $27 billion for June, beating expectations for something close to a loss of $42 billion. This was the second month in three that the U.S. government produced a budget surplus. What is absolutely incredible is that this is the first time that the U.S. government has been on such a "hot streak" (if two of three can be called hot) since the year 2014.

Earnings

Second quarter earnings season will begin in earnest this Tuesday when many of the big banks go to the tape with their numbers. According to FactSet, for the second quarter, consensus for S&P 500 earnings growth is currently at 5%, which is up from 4.8% last week. Second-quarter revenue growth is still seen at growth of 4.2%, which is where that number has been.

For the second quarter, communication services are projected to lead the way having grown earnings a whopping 29.6%, followed by tech at +16.6%. Four sectors are currently projected to have suffered a year-over-year contraction in earnings, easily led lower by energy (-25.8%).

For the full calendar year of 2025, Wall Street sees S&P 500 earnings growth at 9.0%, which is where this number has been for weeks. Expectations for full year revenue growth have stood at 5.0% for a few weeks now.

Valuation

Still using data provided by FactSet, the S&P 500 went into the weekend trading at 22.3-times forward looking earnings, up from 22.2-times the week prior. This is well above the five-year average of 19.9-times and the ten-year average of 18.4 times for the index. The S&P 500 is also trading at 27.5-times trailing earnings, up from 27.3 times last week. This is also well above the five-year and 10-year averages of 24.9-times and 22.5-times respectively.

Banks in Focus

On the surface, everything looks sort of iffy. Once we dig in, it gets a little sloppy. The Financial sector is projected to produce Q2 earnings growth of 2.4% on revenue growth of 4.7%. The positive earnings growth is largely expected to be the result of decent to better than decent quarters by several industries within the sector including consumer finance, insurance, capital markets and financial services. The banks as an industry, according to FactSet, are looking at a possible year-over-year earnings contraction of 11%. This is despite expectations for double-digit earnings growth by the Regionals in aggregate. Yes, I remain long both JP Morgan JPM and Wells Fargo WFC. Of the two. I favor WFC as JPM is up against tougher comps.

Did You Know?

Over the past four quarters, actual earnings growth reported by the S&P 500 in aggregate have exceeded the projected growth rate at the start of the reporting season by 4.6 percentage points. Right now, as mentioned above, the consensus view is for Q2 earnings growth of 5%. Where does that leave us at season's end? Maybe with growth of 9.6%. Again, I credit FactSet as my source for much of this info.

Fed Funds Futures

The next Federal Open Market Committee policy decision looms on July 30, a little more than two weeks out and at least five Fed officials (two governors and three regional presidents) have openly, but politely, mentioned that perhaps Powell is behind on reducing short-term rates. Going into the weekend, Fed Funds Futures trading in Chicago were pricing in a 93% probability for no changes to be made to interest rate policy on that date.

Will the FOMC, however, use the July 30 statement to set up a rate cut at the following meeting in September? We have some consumer price index and producer price index data due this week that will change the math, but at last glance, a 64% likelihood for a quarter-point rate cut is being priced in for Sept. 17 and a 74% probability is being priced in for a second quarter-point rate cut this calendar year.

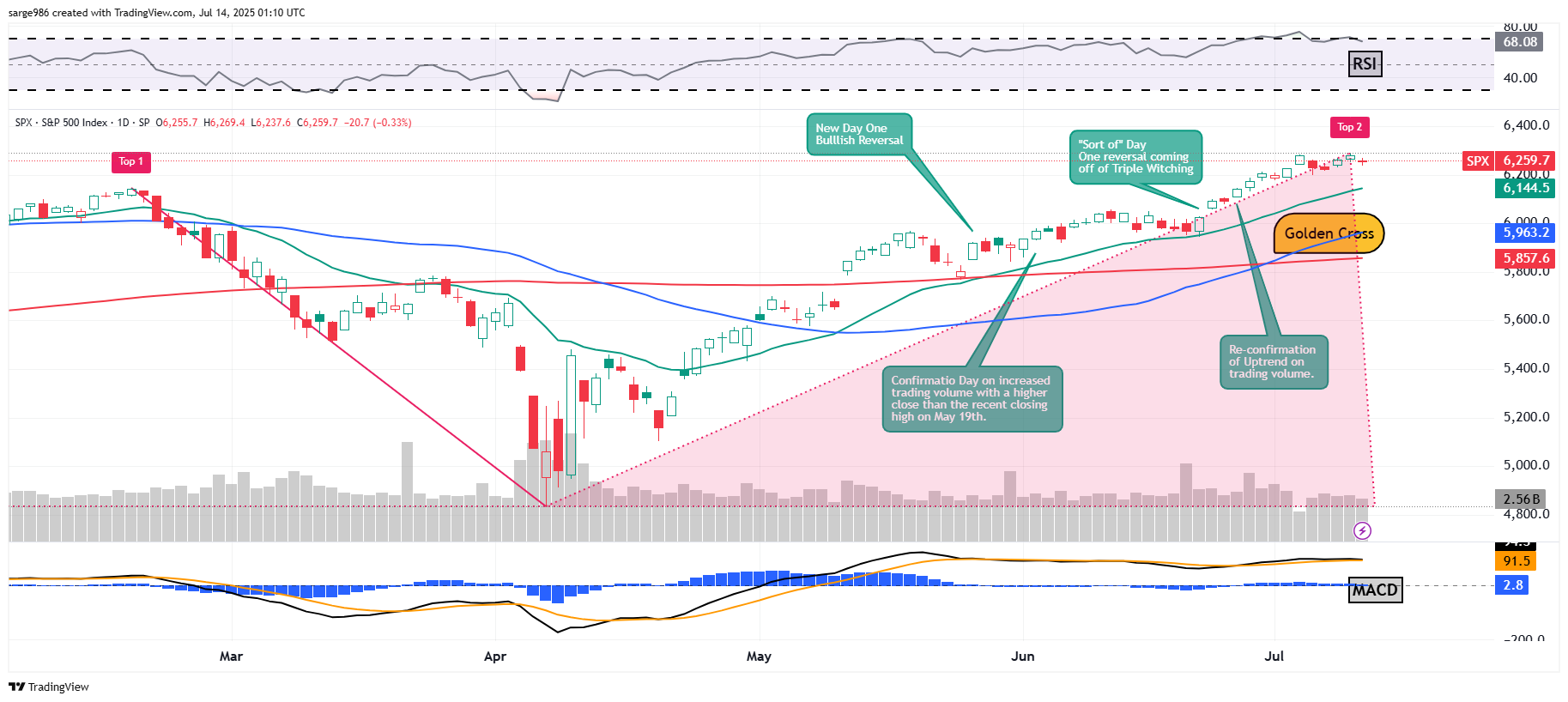

The Chart

If this looks like the same chart I showed you a week ago, it basically is.

The one main difference is that the apex for the second top of our potential Double Top pattern of bearish reversal has been moved to this past Thursday from the Friday prior. Not that I am expecting this Double Top to come to fruition, but the possibility cannot be completely disregarded. I still see the twice confirmed uptrend as valid. Friday's mild to moderate sell-off did not produce a "Day One" reversal as there was a significant drop in aggregate trading volume across the listings of both of New York's major exchanges that day.

Above the chart, readers will see that the reading for Relative Strength has just come out of technically overbought territory, but remains quite robust. Below the chart, readers will see that within the daily Moving Average Convergence Divergence of the S&P 500, the histogram of the 9-day Exponential Moving Average remains well above the zero-bound, which is short-term positive. The 12-day and 26-day Exponential Moving Averages are also well above the zero-bound with the 12-Day line above the 26-day line. That's just as bullish a posture as it was last week. Keep your eyes on that black line. That line dips below the gold line and we'll have a rough go of it for a bit.

Heads Up, Bitcoin Traders

Bitcoin has been trading just below $123,000 per token through the zero-dark hours on Monday morning, up from a $118,000 handle on Sunday evening. This is ahead of expectations that the U.S. House of Representatives will be tackling three separate pieces of crypto-currency related legislation perhaps as soon as this week. On the docket is the regulation of stablecoins, moving the jurisdiction for cryptocurrencies to the Commodity Futures Trading Commission and potentially outlawing a central bank-issued digital currency.

Investors and traders should note that the broad appeal of U.S. dollar-pegged stablecoins not only threatens to eventually supplant actual cash should the Fed be taken out of the picture, but on the bright side, helps to pressure short-term interest rates, as the peg requires a hefty anchor that is most often and most easily provided by heavy investment in T-Bills.

My METC Play

Readers may recall that last week, I had let on that I had initiated a long position in Ramaco Resources METC on Friday in response to the Department of Defense having taken a major stake in MP Materials MP. MP was up 50.62% on Thursday before shaving 0.27% on Friday. In sympathy with MP, METC had rallied 30.94% on Thursday before shaving a mere 0.06% on Friday. As I work my way through the wee hours of Monday morning, I see METC up 12.21% overnight while MP is up 3.7%. What I do not see is new news. I have no idea if this rally is real or simply algorithmic forced momentum.

What's Ahead?

Get ready for an intense week of heavy activity. No way around it. This week, you and I are going to be busier than we have been in at least a month.

- The domestic macroeconomic calendar is extremely heavy and littered with what will likely be highly impactful releases. You, I and the Fed will be watching as the Bureau of Labor Statistics publishes its June CPI and PPI data on Tuesday and Wednesday morning respectively. In addition to those numbers, the Fed will release data for June industrial production on Wednesday morning and the Census Bureau will release its numbers for june retail sales on Thursday. As we traverse the week, both the New York and Philadelphia Feds will also release their respective regional manufacturing sector survey results for July. Finally, June housing starts and building permits will hit the tape on Friday. Expect the Atlanta Fed to update its Q2 estimate for gross domestic product growth on both Thursday and Friday after those releases have been made public.

- The Federal Reserve will be more visible than it has been as a group in several weeks as we approach the media blackout period ahead of the July 30 policy statement. That blackout period begins this Saturday, the 19th. Before we get there, I have at least 12 Fed speakers on my radar this week. Among those 12 are appearances to be made by Govs. Michelle Bowman and Christopher Waller. Both are first-term Trump nominees that have been openly supportive of considering the reduction of the Fed's target range for the Fed Funds Rate as soon as this upcoming policy meeting. The Fed will also release its Beige Book this Wednesday afternoon.

- The earnings calendar kicks into high-gear this Tuesday as the large banks crank up the start of another earnings season. Among the many financials reporting this week will be BlackRock BLK, Citigroup C, JP Morgan Chase JPM, Wells Fargo WFC, Bank of America BAC, Goldman Sachs GS, Morgan Stanley MS, PNC Financial PNC, American Express AXP and Comerica CMA. Non-financial firms posting quarterly performance numbers this week will be JB Hunt JBHT, Johnson & Johnson JNJ, United Airlines UAL, Abbott Labs ABT, GE Aerospace GE, PepsiCo PEP, Netflix NFLX and Schlumberger SLB.

Economics

(All Times Eastern)

No significant domestic macroeconomic data scheduled for release.

The Fed

(All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: FAST (.28)

At the time of publication, Guilfoyle was long NVDA, MSFT, JPM, WFC, METC, GE equity.