'Big' Bill Barely Squeezes Through Senate, Trade Deals Stalled, New Orders Shrink

Bill now gets hammered out in House, Japan proves a sticking point, Institute for Supply Management reveals disappointing data ... and a 'Golden Cross' charts on the S&P.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday, Senate Republicans passed President Trump's "big, beautiful" tax and spending mega-bill after a marathon overnight session of dealmaking, votes on amendments, and efforts to win over fence-sitters who needed some convincing. The end result was a 51-50 vote where Vice Pres. JD Vance, as President of the Senate, was needed to cast the tie-breaking vote.

Kamala Harris is the all-time record holder, casting tie-breaking votes as President of the U.S. Senate a jaw-dropping 33 times in just four years. Mike Pence cast 13 such votes during the first Trump administration. Prior to the past eight plus years, such votes had become less and less common than they had been during the 19th century. Interestingly, 12 of the 50 Vice Presidents never cast a single tie-breaking vote in the Senate (including Joe Biden, who served eight years in that capacity) and only eight of the 50 have cast tie-breaking votes more than ten times.

What Now?

The House Rules Committee met on Tuesday afternoon to set up debate and a potential vote on the Senate adjusted version of this bill as soon as later today (Wednesday), if passage is deemed possible. Speaker Mike Johnson of Louisiana said that House membership would work toward passing the bill by the president's self-imposed July 4 deadline. That, however, may be difficult as the original version of the bill passed in the House back in May by a 215-214 margin. Should the House have to change anything in the Senate-adjusted version, the bill goes back to the Senate and not to the president's desk for an autograph.

The bill includes many of the Trump administration's top legislative priorities such as extending the 2017 tax cuts, and new tax breaks for corporations, those working overtime, those working for tips and those surviving on social security. The bill also increases defense spending, and spending on border security, while reducing spending on Medicaid and other social safety net programs.

The Congressional Budget Office projects that this bill, as law, would increase the federal budget deficit by $3.3 trillion over 10 years. While daunting, it would be unfair not to mention that the CBO used a (probably) unrealistically low rate of economic growth in the modeling over a decade, and did not for some reason use its own projection of $2.8 trillion in tariff-driven revenue over ten years as an offset. House Republicans, if all are present and all vote, can lose no more than three votes and still pass this bill along party lines.

Trade Trouble?

On Tuesday, President Trump was asked by a member of the media aboard Air Force One, if he might consider extending his 90-day pause on reciprocal tariffs on all nations outside of China, so that there could be a period of negotiation. That 90-day period comes to a close a week from today, on July 9. The president responded, "No, no I'm not. I'm not thinking about the pause. I'll be writing letters to a lot of countries."

The president expressed some concern over getting to a deal with Japan. There had been increasing confidence that a trade deal between the U.S. and Japan was a realistic possibility only a week ago. The president commented, "I'm not sure if we're going to make a deal, I doubt it, with Japan. They're very doubtful. You have to understand, they're very spoiled. They and others are so spoiled from having ripped us off for 30, 40 years, that it's hard for them to make a deal."

Pres. Trump added, "On trade, they've been very unfair and those days are gone. So, what I'm going to do is, I'll write them a letter, say 'we thank you very much. We know you can't do the kind of things that we need... and therefore, you'll pay a 30%, 35%' or whatever the number is that we determine because we also have a very big trade deficit with Japan."

As for reaching a deal with India, the president was much more positive: "I think we're going to have a deal with India. Possibly, and that's going to be a different kind of deal. It's going to be a deal where we are able to go in and compete. Right now, India doesn't accept anybody in. I think India's going to do that and if they do that, we're going to have a deal for much less tariffs."

Still Sluggish

The Institute for Supply Management, also known simply as the ISM, released its May survey of purchasing managers from across the manufacturing sector on Tuesday. The headline print crossed the tape at 49, up from 48.5 in May, but still in a state of contraction. In these surveys, 50 is the line between expansion and contraction. The single most important component in any manufacturing survey is new orders, and new orders printed at a badly disappointing 47.6, a fifth consecutive month of contraction that appears to be accelerating to the downside.

It gets worse. Employment hit the tape at 45, also a fifth consecutive month of contraction, while backlog of orders landed in a state of contraction for an incredible 33rd consecutive month. Perhaps, scarier than these numbers is one of the few components that make up this survey that printed in state of expansion: Pricing, or simply, inflation. Prices hit the tape at 69.7, up from 69.4 in May and a ninth consecutive month of upside growth.

Marketplace

Tuesday was a sloppy day for the markets if anything. As the Senate was busy passing the "big, beautiful" bill, Fed Chair Jerome Powell spoke before the ECB Forum and stuck to his guns as far as his "wait and see" stance on monetary policy is concerned. This put mild upward pressure on yields across the slope of the Treasury curve. The U.S. Ten-Year Note paid 4.26% by day's end (+3 bps), while the yield on the U.S. Two-Year Note popped 7-basis points to 3.79%.

Additionally, the war of words broke out again between Pres. Trump and former DOGE boss Elon Musk. Tesla TSLA surrendered more than 5% in response. Investors expect to hear quarterly delivery numbers from that firm later today. Musk has been critical of the bill now before the House as it strips subsidies for firms like his and is now threatening to launch a political party meant to compete with the Democrat / Republican duopoly in American politics.

The S&P 500 gave up just 0.11% on Tuesday as the Nasdaq Composite gave back 0.82%. Both of those indices failed to set new all-time record highs for the first session since last Thursday. Capital flowed into the Dow Transports, the Dow Industrials, and small to midcap stocks as a severe bout of profit-taking hit the market's recent high-fliers.

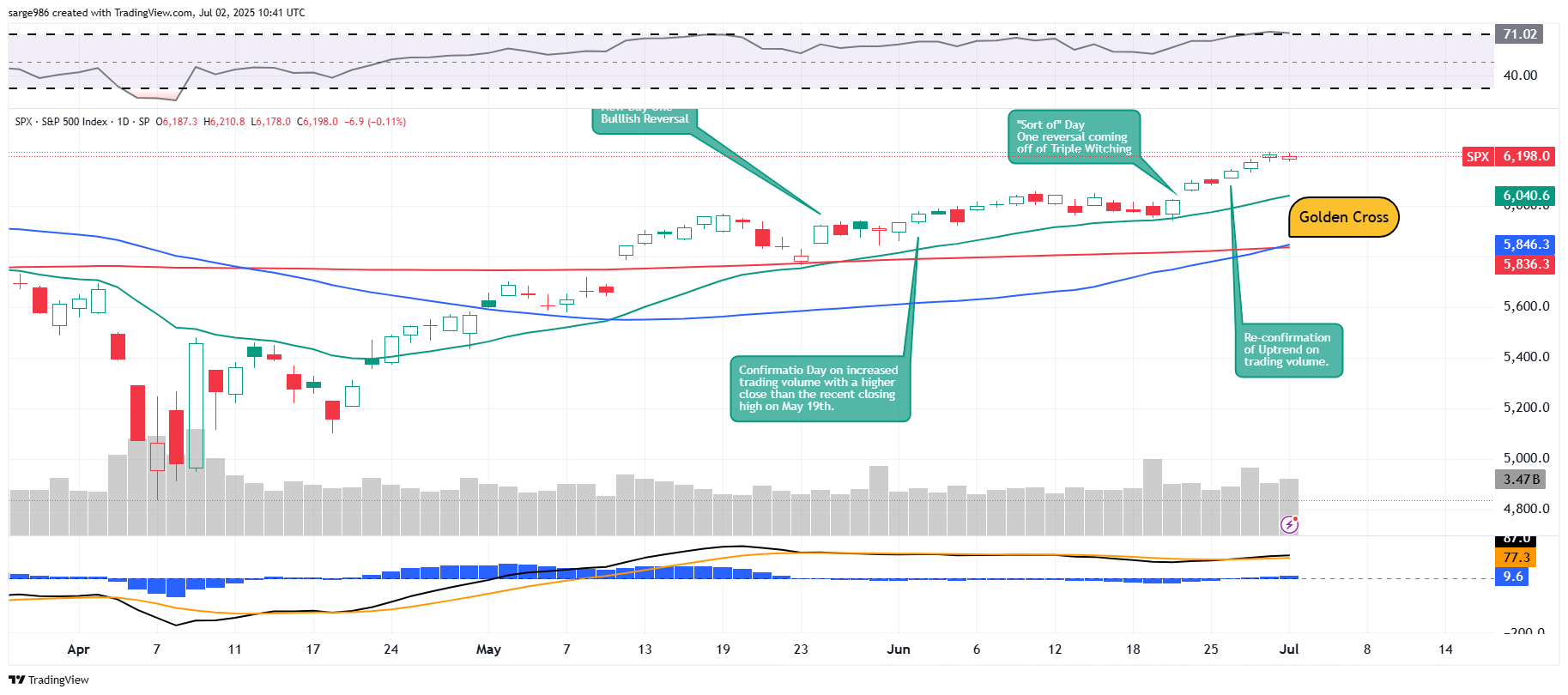

Golden Cross

The S&P 500 experienced what is known as a "golden cross" on Tuesday. This is when an accelerating 50-day simple moving average crosses above an also rising 200-day SMA.

Historically, this was seen as a positive signal, but in recent years, it really has just become a visible but lagging indicator of a market that is trending upward. It's worth noting. I don't get too excited about such things, unless of course, the algorithms that control price discovery in this modern era do.

Breadth

Still, nine of the 11 S&P sector SPDR exchange-traded funds shaded into the green on Tuesday. Materials XLB led the way, at +2.59% as the U.S. Dollar Index weakened. Defensive sectors were three of the top five performing sector funds for the day in a sharp reversal from last week, while the two growth sectors were the two losers. The Technology XLK SPDR gave up 0.89% and the Communications Services XLC SPDR lost 0.71%.

Within those two funds, the Dow Jones U.S. Semiconductor Index and Dow Jones U.S. Software Index surrendered 2.46% and 1.14% respectively, while the Dow Jones U.S. Internet Index lost 1.14%. Some examples of profits being taken where profits were on Tuesday were many. From the semis, Advanced Micro Devices AMD and Broadcom AVGO gave up 4.08% and 3.96% in that order. Among Software names, MicroStrategy MSTR or Strategy gave up 7.65% as Cloudflare NET gave back 5.56%. From the internet, Spotify SPOT lost 5.86%, as Netflix NFLX lost 3.4%.

Winners still beat losers on Tuesday, by an impressive 3-to-1 margin across the NYSE, and by a rough 4 to 3 across the Nasdaq. Advancing volume took a 69.1% share of composite NYSE-listed trade, but just a 49.2% share of composite Nasdaq-listed activity. Aggregate trade did increase across NYSE-listings, Nasdaq-listings and the membership of the S&P 500. However, with the major indexes lower, I am not sure just how meaningful generally positive breadth is. This could really just be a reflection of a rotation out of year-to-date winners and into year-to-date strugglers.

By the Way...

After Tuesday's "not so hot" release of the June version of the ISM Manufacturing PMI Survey and the negative (and worse than expected) May print for construction spending, the Atlanta Fed revised its GDP Now model for the second quarter down to growth of 2.5% from growth of 2.9% (q/q, SAAR).

Fed Funds futures markets are still pricing in a 55% probability for a three-quarter point worth of rate cuts by year's end. This market is also pricing in a likelihood of 53% for 1.25 percentage point worth of rate cuts by July 2026.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.88%.

07:00 - MBA Mortgage Applications (Weekly): Last 1.1% w/w.

08:15 - ADP Employment Report (Jun): Expecting 93K, Last 37K.

10:30 - Oil Inventories (Weekly): Last -5.836M.

10:30 - Gasoline Stocks (Weekly): Last -2.075M.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: UNF (2.09)

At the time of publication, Guilfoyle was long AMD equity.