Bank Earnings Bonanza, China Trade Disruption, Rare Earths Rumble

It's game on for quarterly reports as Citigroup, JPMorgan, Wells Fargo and more report; also rare earths names jump higher and guess what Dimon's planning....

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I can almost hear the 1970s era pre-game music from "Monday Night Football." All we'd need are the familiar voices of Dandy Don Meredith, Frank Gifford and of course, Howard Cosell and we would be all set. Third-quarter earnings reporting season, though a few names have already gone to the tape, will begin in earnest ahead of this morning's opening bell.

Before the bell signals the start of Tuesday's regular trading session, some of the nation's largest financial institutions will post their quarterly numbers. We'll hear from BlackRock (BLK) , Citigroup (C) , JP Morgan (JPM) , Wells Fargo (WFC) and Goldman Sachs (GS) . Just to change things up, we'll also hear from Johnson & Johnson (JNJ) and Domino's Pizza (DPZ) one day after Domino's competitor Papa John's (PZZA) ran more than 9% on a report that Apollo Global (APO) may have made a bid for the company.

Asian stocks, however, traded lower on Tuesday, European stocks have opened lower and U.S. equity index futures are trading lower. What gives? Profit taking ahead of those big bank earnings? No. The action in the U.S. did take back some ground lost on Friday, but not all that much, really. It's about U.S.-China trade relations. Again.

On Thursday, China threw a rare earth-related punch ahead of upcoming U.S. / China trade negotiations. On Friday, Pres. Trump punched back. Equities sold off hard. On Sunday, Pres. Trump tried to ease tensions. Equities rallied. Now, Beijing has announced a probe into and sanctions on the five U.S.-based subsidiaries of South Korean shipping giant Hanwha Ocean. The order will prohibit Chinese organizations and individuals from doing business with the sanctioned companies. Shares of Hanwha were trading more than 8% lower in South Korean trade.

On Top of That...

Beijing confirmed that it had begun collecting additional port fees on U.S.-linked vessels while clarifying that Chinese vessels are exempt from those charges. This particular move came in response to a US decision to impose fees on Chinese vessels at American ports starting this morning as well. Hence, all is not really "fine."

Of Course...

Monday's rally was not just about a president's social media post, a peace deal in the Middle East, or a simple rebound coming off of Friday's market smackdown. JPMorgan had a little something to do with it, too. The nation's largest bank by assets and market cap, according to Reuters, announced a broad $1.5 trillion (with a T), 10-year long initiative aimed at investing in industries that are core to U.S. economic strength and national security.

The plan will fund four core areas including aerospace & defense, frontier technologies such as AI & quantum computing, supply chain & manufacturing to include pharmaceuticals and critical minerals, and energy independence. JPMorgan has committed up to $10 billion of its own capital in the form of direct equity and venture capital investment toward select U.S. companies.

JPMorgan Chair and CEO Jamie Dimon stressed that "This is a JPMorgan initiative" and "not driven by the Trump administration." Dimon explained, "It has become painfully clear that the U.S. has allowed itself to become too reliant on unreliable sources of critical minerals, products and manufacturing -- all of which are essential for our national security. Our security is predicated on the strength and resiliency of America's economy. America needs more speed and investment."

Dimon wasn't done. America's most powerful banker added that needs for changed policies include removing "excessive regulations, bureaucratic delay, partisan gridlock, and an education system not aligned with the skills we need." Dimon exclaimed, "We need to act now."

Relentless

Led by MP Materials (MP) , which has the backing of the Department of Defense / War, rare earth miners jumped on both Friday and Monday after last week's move by China to tighten export controls over these critical metals and minerals. MP was up 8.4% on Friday and another 21.3% on Monday.

Among smaller companies, U.S. Rare Earth (USAR) ran 5% on Friday and 18.6% on Monday and Ramaco Resources (METC) popped for a gain of 1.9% on Friday and 11.1% on Monday. Ramaco Resources, which is a Sarge name and "Stocks Under $10" name here at TheStreet Pro, is up 58% October to date. The stock is up 214% since I mentioned my position to readers in July and up 732% from its April low.

Marketplace

So, was that the "pause?" Maybe. Readers will recall that I wrote to you warning that "they" would try to shake us out of our long positions in October. While the feeling is not one of love and warmth, surprise is not the emotion felt as the market tries to find its way through this period. The screen was greener than a Christmas tree on Monday and greener than a New York Jets fan might be with envy looking at the current NFL standings.

The S&P 500 gained a sharp 1.56% on Monday, which was exceeded by a red-hot Nasdaq Composite at +2.21%. The Philadelphia Semiconductors roared, gaining 4.93% led by Arm Holdings (ARM) and Broadcom (AVGO) , while all of your favorite small to mid-cap indexes added between 1.96% and 2.79%. Even the KBW Banks gained 1.96% ahead of earnings. Gold reached yet another new record as silver traded above $50 per ounce. The U.S. Ten-Year Note, which paid as much as 4.15% late last week, is paying just a smidgen above 4% this morning as the wind continues to howl but the rain has stopped.

Breadth

Nine of the 11 S&P sector SPDR exchange-traded funds closed out the Monday session in the green as well, led by Technology (XLK) and followed closely by the Discretionaries (XLY) . Now, we get to the issue. Winners beat losers by a rough 15 to 4 at the NYSE and by about 8 to 3 at the Nasdaq. Advancing volume took a commanding 83.8% share of composite NYSE-listing volume and a 70.6% share of composite Nasdaq-listed activity. All good, right? No. Not all good.

Aggregate trade across NYSE-listings was down 19.6% on Monday from Friday and down 22.5% across Nasdaq-listings day over day as well. Trade was down sharply across the membership of the S&P 500 as well. Now, check this out...

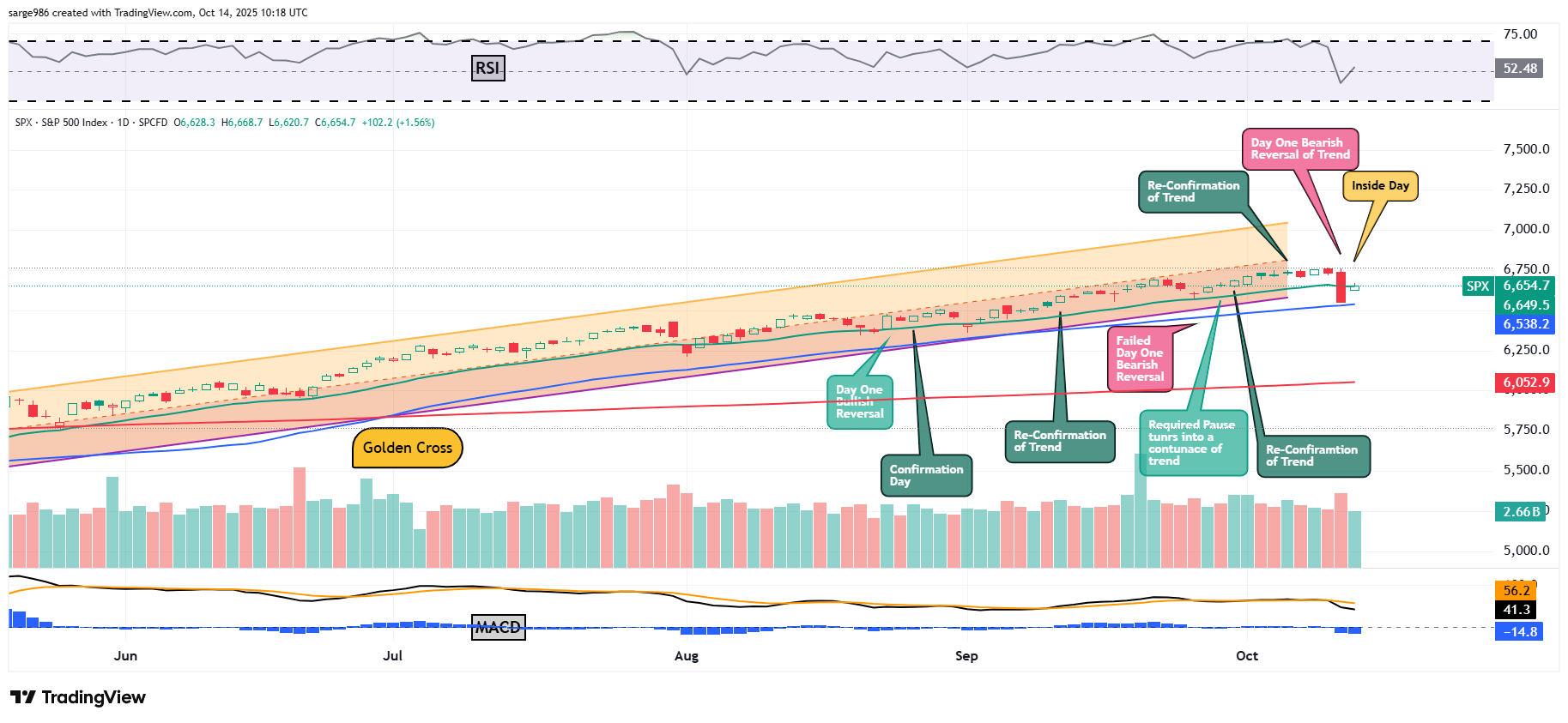

Take a look at Monday's candlestick. Not only did the rally fail to take and hold its 21-day exponential moving average, but the day clearly ended as an "Inside Day," which often signals reduced volatility going ahead. In this case, it may have signaled nothing more than the required pause that I often mention must occur in between a "Day One" of trend reversal and a subsequent "Confirmation Day" of change in trend.

Just take a look at the trading volume on that chart. Monday was a continuation of decreasing activity that began last week with Friday's selling pressure sticking out like a sore thumb. Clearly, enough professionals must have sat out or barely dabbled in Monday's rally. I do not like the look of the daily Moving Average Convergence Divergence (below the chart) for the S&P 500.

Nvidia News

Nvidia (NVDA) announced late Monday that it will now start shipping its Nvidia DGX Spark. The DGX Spark is the world's smallest AI supercomputer. DGX Spark will deliver a petaflop of AI performance and 128 gigabytes of unified memory in a compact desktop form factor. This gives developers the power to run inference on AI models with up to 200 billion parameters and fine-tune models of up to 70 billion parameters locally. I could go on, but I think we both know that I don't know what the hockey puck I am writing about here. The point is that once again, Nvidia is ahead of the crowd and has created a "next best thing" and that next best thing is ready to rock.

Petaflop Vs. ... Us?

I looked it up so you don't have to. A petaflop is a measurement of speed representing one quadrillion floating-point operations per second. According to the AI overview that I am reading, which has been provided by Alphabet's (GOOGL) Google: "It would take about 8 billion people, each performing one calculation per second, roughly four years to achieve what a single petaflop system can do in one second."

On that note, I still believe that those of us still reliant upon natural intelligence can win. Not on speed. We lost that fight once "they" fine-tuned the third generation of trading algorithms. NI can beat AI or at least other humans as humankind becomes more and more reliant upon AI. Diversity in both interpretation and opinion over time, will diminish as cognitive and intellectual sloth increases.

Most of us will, without realizing it, regress to mean. Average to well above average IQ types won't be able to help it. They won't even realize it's happening. There will, however, be opportunity when seeing where that hockey puck is going before it gets there. Instead of simply hitchhiking aboard consensus view, instead we will counter that view with strategies that better time and pinpoint target prices, pivot points and panic levels.

Will beating Wall Street remain difficult? Of course. One must admit that beating Wall Street is not as difficult in recent years as it used to be. Even as technology improved. If you're playing the game at this level, you never were average anyway. You were always "that" guy or gal. Don't give up the fight. You have to work on maintaining your natural intelligence as you do your muscle mass and cardiovascular health. We shall persevere and we shall rise above. Count on it.

Economics

(All Times Eastern)

06:00 - NFIB Small Biz Optimism Index (Sep): Expecting 100.5, Last 100.8.

08:55 - Redbook (Weekly): Last 5.8% y/y.

The Fed

(All Times Eastern)

08:55 - Speaker: Reserve Board Gov. Michelle Bowman.

12:20 p.m. - Speaker: Federal Reserve Chair Jerome Powell.

3:25 - Speaker: Reserve Board Gov. Christopher Waller.

3:30 - Speaker: Boston Fed Pres. Susan Collins.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open:

(ACI) (.40), (BLK) (11.32), (C) (1.93), (DPZ) (3.97), (ERIC) (1.91), (GS) (10.63), (JNJ) (2.76), (JPM) (4.87), (WFC) (1.54)

At the time of publication, Guilfoyle was long JPM, WFC, METC, NVDA, GOOGL equity.