Asian Markets Respond to Tariffs. But Not How You’d Expect.

We may see tariffs hurt U.S. economic data first.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In my last column, I described the calm as Asian markets hunkered down ahead of an oncoming tariff typhoon.

Today, the storm …

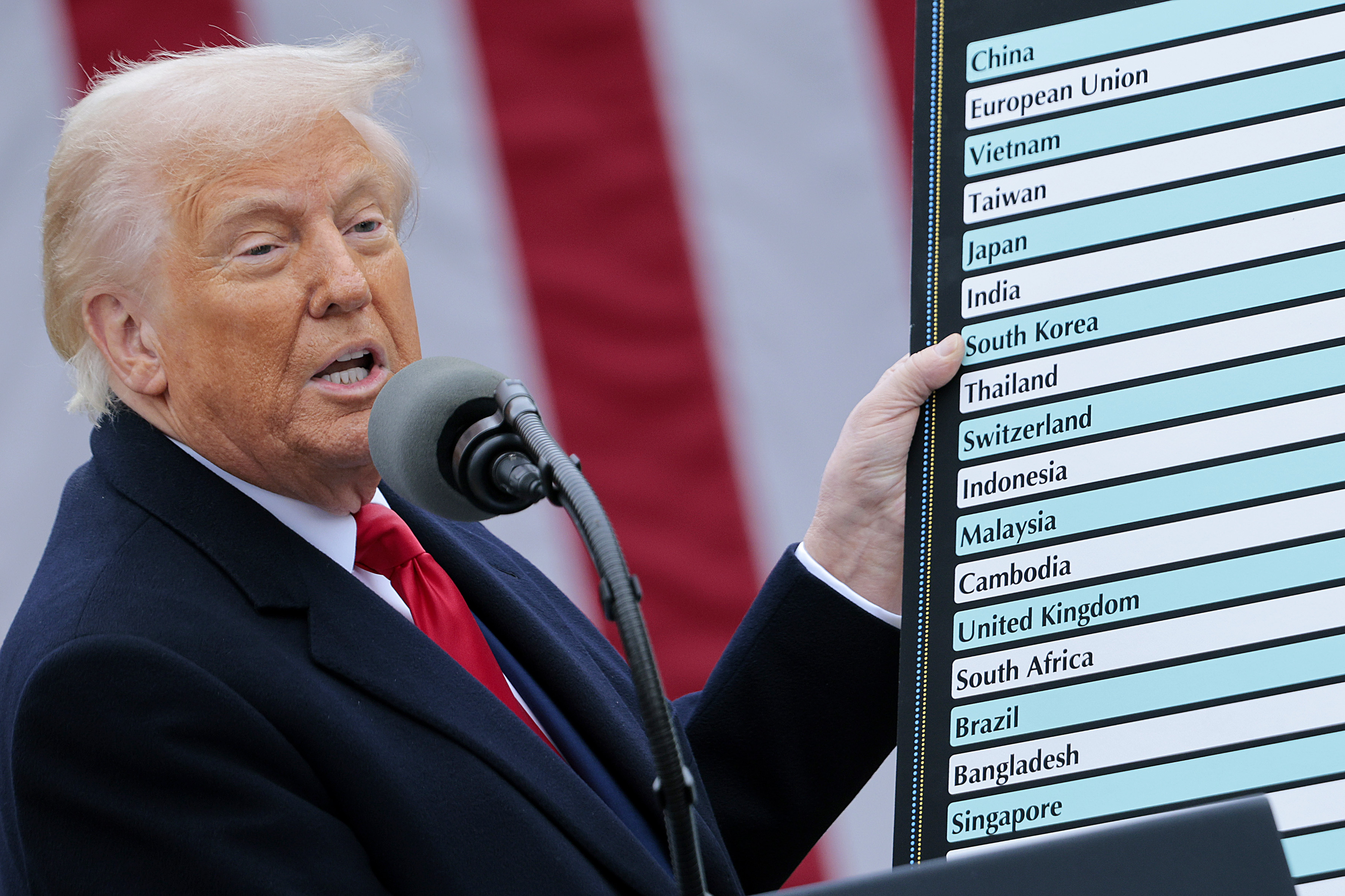

Asian markets are being buffeted by the bluster from the White House. The so-called “reciprocal” tariffs announced by U.S. President Donald Trump came out overnight, for those of us on Asia time.

While stocks are hurt Thursday, almost all markets in Asia down, the impacts are far from uniform. Again, I would expect worse selling – if the tariffs actually go ahead. Markets doubt that.

Japan is taking a heavy stock-market hit Thursday, faced with an added 24% U.S. tariff tax. The broad-market Topix is down 3.1% in Tokyo, with the blue-chip Nikkei 225 (perhaps surprisingly, given its export-heavy mix) slightly better off with a 2.8% drop.

South Korea is also an export-heavy market, and now faced with an extra 25% U.S. duty. The Kospi has just eased slightly, down 0.8% Thursday. Market heavyweight Samsung Electronics (KR:005930) sank 2.0%, with defense contractors and domestic industrials up on the day, offsetting that weakness.

We’ll have to wait until Friday to see the effect in Taiwan (added 32% tariff), where markets are closed for a holiday Thursday.

South and Southeast Asia Hit Hardest

Some of the heaviest added tariffs are in Southeast and South Asia. Cambodia (extra 49% tariff), Laos (48%), Sri Lanka (44%), Vietnam (46%), Bangladesh (37%), Thailand (36%), Indonesia (32%) all face dramatically higher import duties into the United States. There’s a chart featuring them all here.

Vietnamese stocks are suffering the most in Asia, with the Ho Chi Minh benchmark index down 6.7%. Sri Lanka’s market is 2.1% lower, but the response in places like Thailand is measured, stocks down 1.2%.

We likely aren’t seeing the full extent of the selloff. “We think this is a clear risk-negative event for Asian stocks, and we do not see it as a market ‘clearing event,’ which some market participants were hoping for,” Nomura’s Asia ex-Japan strategy team, led by Chetan Seth, say. The tariffs appear “bigger and broader than generally expected,” Seth and team add, due to go into effect in a few days, leaving little room to renegotiate them.

What’s more, with Trump having made a big song and dance about these “reciprocal” tariffs, introducing them on the Rose Garden lawn, it’s going to be hard to retract them.

'Full-On Crazy'

Nobel prize-winning economist Paul Krugman, in his blog, calls the tariffs “full-on crazy.” The average European Union tariff on U.S. goods is less than 3%, yet Trump trotted out a chart indicating that Europe charges a 39% tax on U.S. imports.

“If you had any hopes that Trump would step back from the brink, this announcement, between the very high tariff rates and the complete falsehoods about what other countries do, should kill them,” Krugman says.

I’m sure Trump is expecting a series of groveling calls from the leaders of the hardest-hit nations, looking to negotiate a deal on trade. Are these tariffs designed to raise revenue, as Trump sometimes claims? Or force other countries to lower their tariffs? Or, preposterously, to stop drug cartels smuggling fentanyl illegally into the United States?

Who knows. The story changes every time it’s told. Drug cartels are not known for paying trade tariffs. But U.S. consumers will certainly pay a price.

Nomura will be watching, first of all, for any weakness in the U.S. economy, particularly consumer spending and employment. “Any softening of data will likely increase market concerns of a U.S. recession/stagflation, which will likely weigh further on risk sentiment in general, including on Asian stocks,” its strategists say.

A Bazooka Response?

What we can expect now is retaliation from the world’s major economies, led by the European Union (20% tariff), the leading source of U.S. imports, at 18.5%. China ranks next at 13.4% of U.S. imports, and has also pledged to respond.

China calls Trump’s attempts to rejig world trade “a typical act of unilateral bullying,” outside the existing structures on trade. “There is no winner in a trade war, and protectionism leads to nowhere,” a Chinese Commerce Ministry spokesperson said.

“The United States has drawn the so-called ‘reciprocal tariffs’ based on subjective and unilateral assessments,” the ministry added in a statement on Thursday. It says China will “resolutely take countermeasures to safeguard its own rights and interests.” Any talks on curbing fentanyl shipments will require cancelling the “unjustified tariff increase,” China’s foreign ministry insists.

Europe is considering deploying a policy tool known as the anti-coercion instrument, which went into effect at the end of 2023. Others call it a trade war bazooka. “We have the power to push back,” European Commission President Ursula von der Leyen said earlier in the week.

Japanese stocks are suffering because Tokyo may have limited scope to punish U.S. trade. Prime Minister Shigeru Ishiba is holding out hope to get Trump on the phone. “If it is deemed appropriate for me to directly engage with President Trump, I have no hesitation in doing so at the most suitable time and in the most appropriate manner,” he said, sounding a little desperate. Meantime, his ministers are mulling their retaliatory response.

We already know that tariffs of 25% on auto imports, and auto parts, are in effect as of today. Toyota Motor TM T:7203 shares fell 5.2%, and Honda Motor HMC T:7267 dropped 2.3%. In Seoul, Hyundai Motor sank 1.3%, perhaps offset by its pledge to invest US$21 billion on U.S. soil by 2028.

But many of the world’s poorest nations are targeted for the highest tariffs. The diversification strategy by multinationals to expand production outside China does little to avoid these tariffs, which are effectively global.

Poor Bangladesh

Now, I’ve got to ask you, do you really think that the citizens of Bangladesh, suddenly faced with an extra 37% tariff on their U.S. factory shipments, are getting rich at the expense of American citizens?

On the one hand, you have the world’s largest economy, forecast by the IMF to top US$30 trillion for the first time this year, resulting in a median U.S. per capita income of US$19,306.

That's the fifth-highest per capita income on the planet, outdone only by tiny Luxembourg, the oil wealth of the United Arab Emirates, and the strong social welfare networks in Norway and Switzerland.

On the other hand, you have the world No. 8 nation in terms of population, with 175.7 million citizens on low-lying, flood-prone swampy land along the coast of the Bay of Bengal.

Per capita income in Bangladesh? It’s US$1,131, just behind war-torn Yemen. Despite those millions of people, roughly half the 347.3 million population of the United States, the total Bangladeshi output ranks it only No. 36 in the world, just ahead of Denmark (population 6.0 million) and my adopted hometown, Hong Kong (population 7.6 million).

When I first moved to Hong Kong in 2001, I went on a press tour of Guangdong, China’s most-productive province. The factories across the border from me in industrial Dongguan were making cheap pleather shoes and plastic toys.

Most of those jobs have long gone. Check the labels in your T-shirts or on cheap shoes in a store. Now they’re made in Bangladesh, Sri Lanka, Laos, you name it.

And the Dongguan factories produce drones, smartphones, robotics. There’s a neutron accelerator. It’s been a wrenching change, and a lot of factories went under during the disruption of Covid-19, but the province is better off now that the sweat shops have largely left.

Here in Hong Kong, by the way, the effect is once again not quite as bad as you might expect. The Hang Seng index ended Thursday down 1.6%, but remains the world’s best-performing major market since Trump took office. It’s up 16.5% in 2025.

The CSI 300 of the largest listings in Shanghai and Shenzhen is little-changed Thursday, down just 0.6%. Mainland stocks never sold off as hard as Hong Kong earlier this decade, and so they haven’t shared Hong Kong’s rebound. The index is also little-changed this year, up 1.1%.

Likewise, Indian stocks are little-changed. The Sensex is off 0.4%, and the Nifty 50 down 0.3% as I write.

There’s a chance we’ll see selloffs followed by rallies in Asia. Even if U.S. consumers pay the direct price of tariffs, the spillover effects will ultimately follow through to Asian earnings. So it may be time to fade into any bounce in stocks.

“We suspect Asian stocks will likely have to go lower before we reach a stage where risk-reward becomes decisively more favorable for Asian equity investors to go on some bargain hunting,” Seth and the Nomura team conclude.