All That Cash on the Sidelines Probably Isn't Going to Do What You Think It Will

There's currently $7.4 trillion sitting in money market funds. But what's happened with previous parabolic rises in cash accounts may surprise you.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There is a consensus theory that the record amount of cash on the sidelines will be put to work in risk assets, namely stocks, as interest rates on cash deposits are reduced by a lower Fed Funds rate. Yet, we would argue that those with cash on the sidelines aren’t doing so for the 4% yield they are likely enjoying. Instead, they are attempting to avoid the characteristic risk assets are named after.

In other words, earning less than 5% annually sounds quite boring in a post-2020 world that has seen an average of 15ish percent in equity indexes. But those sitting on cash are willing to give up 15% to save themselves 30% to 50% and give them the optionality to be an aggressive dip buyer should the bottom fall out.

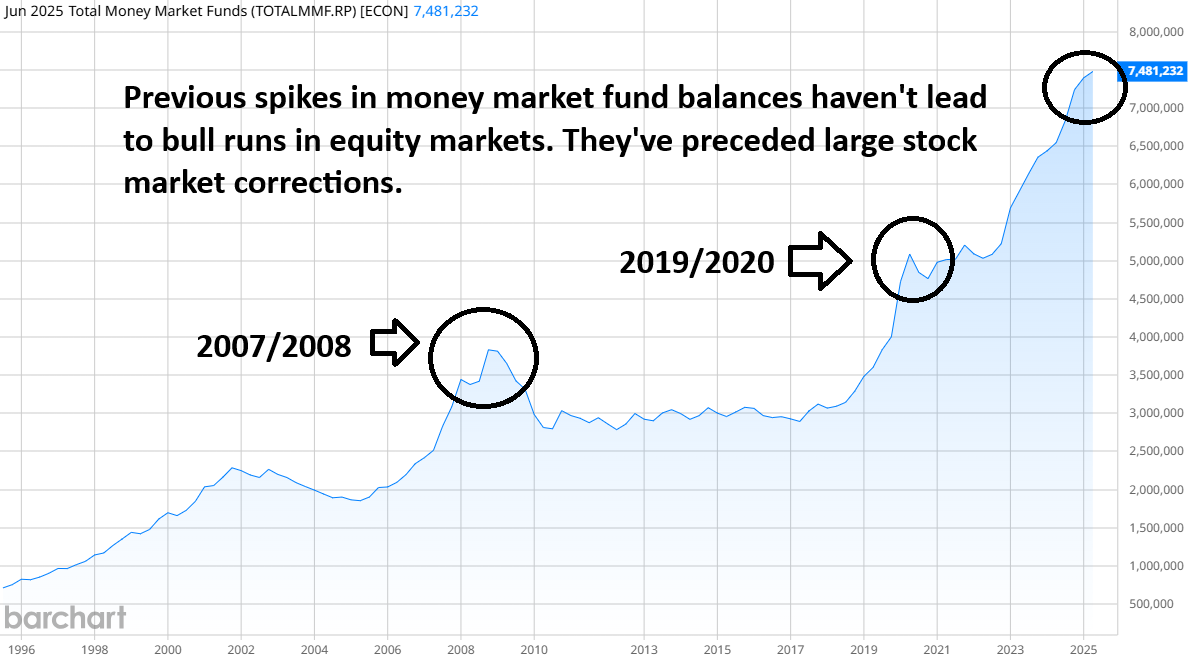

We have never seen this much cash in savings and money market accounts. There is currently $7.4 trillion sitting in money market funds collecting 3% to 4%. Stock market bulls will tell you that this equates to over $7 trillion in cash on the sidelines, waiting to be invested in the stock market in a FOMO-type melt-up.

While this might be the case, it doesn’t have to work that way. In fact, previous parabolic rises in cash accounts have not led to sustained bull markets. Instead, they have been a precursor to large equity market corrections.

In 2007/2008, cash was hoarded in money market accounts at a parabolic rate. Did these people see what was coming around the corner? Maybe, but it was probably just prudent risk management in a world in which asset prices (stocks and real estate) had been melting up for years.

Similarly, from 2019 to early 2020, there was another stockpiling of cash-like assets. Shortly after, the pandemic triggered a quick but massive stock market correction. Lastly, in the current cycle, cash stockpiles have grown sharply since 2023.

Will this time be different? Or is this another signal that the smart money knows this is a time to tap the brakes on risk-taking rather than go pedal to the metal?

Keep in mind, Warren Buffett and his fund are holding the largest cash allocation ever. Thus far, his slow-motion patient strategy has paid off. Perhaps cash on the sidelines isn’t bullish; maybe it is bearish.

The old money knows the best way to have the capacity to play offense on large market swoons is to have a rainy-day fund that can be employed when the opportunity presents itself. Perhaps sidelined cash will act as a put option on any potential correction rather than a tailwind for the current rally.

I’ll add another plot spin. Since the financial crisis, the futures markets have become more accessible to casual retail investors. The CME Group has created micro-sized contracts with smaller contract sizes, lower margins, and reduced risk compared to the original products. Further, the internet and social media have provided opportunities for the masses to be introduced to relatively sophisticated products and strategies with very low barriers to entry.

These conditions have created a scenario in which sidelined cash might not necessarily be free from risk asset exposure. For instance, a trader who puts $35,000 into a money market fund to earn 4% per year might also open a futures trading account to purchase a single Micro E-mini S&P 500 futures contract. She can do so in an account with as little as $2,500.

This strategy enables the investor to earn 4% interest on $35,000 while also generating capital gains from the S&P 500 in the form of futures profits. This assumes the stock market goes up; if it goes south, the investor would be required to wire funds from the money market account to meet the margin deficit in the futures account. At this time, the investor would be earning interest on a smaller balance but would still enjoy the benefits of both worlds, albeit with some potential inconveniences should a market downturn occur.

This is not only an income-efficient strategy, but it is a tax-efficient strategy. Futures profits, assuming they are profits, are taxed as 1256 Contracts at a 60/40 blend between long-term and short-term capital gains.

Bottom Line

Historically, cash on the sidelines hasn’t propelled stocks higher; it has been a sign of old money, or maybe smart money, practicing risk aversion to extended bull markets.

Lastly, even if this wasn’t the case, a good chunk of that cash on the sidelines might already be in the market via derivatives (long futures). Thus, if your bullish thesis is mainly relying on the theory of money market funds being reallocated to stocks, you might want to reconsider.