All Eyes on Oil, a Clue in Banks' Beating, the SanDisk Lift

Let's check the latest in Crude, JP Morgan Chase's reported loan reveal and how SanDisk and Micron are doing some heavy lifting.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Market_Recon_TSP1_KL

Market_Recon_TSP1_KL

Saved by Zero

Maybe someday, saved by zero

I'll be more together

Stretched by fewer thoughts that leave me

Chasing after my dreams, disown me, loaded with danger

So maybe I'll win (saved by zero)

Maybe I'll win (saved by zero)

Holding onto words that teach me

I will conquer space around me

So maybe I'll win (saved by zero)

Maybe I'll win (saved by zero)

- Woods, Agius, Curnin, Oram, Greenall (The Fixx),1983

Where's Oil Headed?

Front month WTI Crude oil futures have largely traded sideways since Monday afternoon. Same for Brent Crude. Equities haven't done much either. Sure, there was a mild rally mid-day on Tuesday that markets managed to give back late in a moderately negative session. U.S. equity index futures then took back most of these moderate losses overnight and then re-lost them.

Though the Bureau of Labor Statistics will release its February data for consumer prices this morning and those numbers are important, the impact of the war on crude prices and subsequently, gasoline prices, will not be visible in that data. The same can obviously be said for this Friday, when the Bureau of Economic Analysis releases its January data for consumer prices. We still have to wait a month or so, to see trailing numbers that will illustrate just what these gyrations in oil prices have done to U.S. consumers.

Headline? Oh, there are enough headlines that could or even should impact crude prices. The International Energy Agency (IEA) is reportedly preparing the largest release of strategic oil reserves in the history of that organization. That's 32 nations for those counting. The U.S. Navy has been reported as having escorted a tanker ship through the Strait of Hormuz, though the Navy itself denies that this even happened. The confusion started with a now-deleted tweet posted by U.S. Secretary of Energy, Chris Wright,

The Pentagon is, however, reporting that 16 Iranian minelayers have been destroyed either in or close to the strait. That said, the Financial Times is reporting that on Tuesday, three cargo vessels were struck by projectiles off of the coast of Iran. That makes 14 cargo vessels that have been hit with something since the start of the war.

JPM's Loan Markdown

For those wondering why bank stocks have been slapped around for weeks now, overnight, the Financial Times also reported that JP Morgan Chase (JPM) had informed private credit lenders that it had marked down the value of certain loans in its portfolios. These loans serve as collateral that these funds use to borrow from this bank and others, which is why this matters so.

The loans devalued are said to in many cases, have been made to software companies. That group has been seen of late as particularly vulnerable to the advance of agentic artificial intelligence. JP Morgan Chase declined to comment. JP Morgan has something of an advantage over its competitors as a private credit financier. JP Morgan reserves the right to revalue these assets at any time. Most banks require that stated triggers are met, such as having missed payments in order to do so.

Related: People Love to Hate the Dow—But Its Latest Move Deserves Attention

On That Note...

The Wall Street Journal is reporting that a number of well-known hedge funds have suffered large losses as oil prices surged and bonds sold off in response to the war in the Middle East. The piece at the Journal names Citadel, Millennium Management, Point72, Balyasny Asset Management, and ExodusPoint Capital Management as being among the funds that have suffered significantly after having gotten 2026 off top solid start.

Supposedly, Millennium and Point72 were each tagged for losses of as much as $1.5 billion just last week. The article says that Citadel and Balyasny each lost about $1 billion last week and that ExodusPoint lost "a couple hundred million dollars on bond market bets." While these numbers appear to be startling, the piece makes sure that readers understand that several of these managers reportedly remain up year to date.

Marketplace

The field slanted into the red on Tuesday, but not significantly so. While the S&P 500 gave up 0.21% for the session, the Nasdaq Composite essentially closed unchanged (+0.01%). The small to mid-cap indexes suffered the most, all losing from between 0.22% to 0.54% for the day. The Philadelphia Semiconductor Index again led the mid-majors, with a gain of 0.7%. That group itself was again led by SanDisk (SNDK) and Micron (MU) as the focus was on memory chip design. The Dow Transports again were the losers, down 0.88% on Tuesday as the airlines again landed in the red.

Breadth

Ten of the 11 S&P sector SPDR exchange-traded funds closed out the regular session on Tuesday in the loss column. Energy (XLE) was the biggest loser, followed by Health Care (XLV) . There were no winners among these 11 funds. Technology (XLK) closed flat on the day as a 1.86% loss for the Dow Jones US Software Index offset those gains made by the semis. Applovin (APP) was bludgeoned for a loss of 7.7% to lead that group in a southerly direction.

In the broader sense, market breadth was not really all that ugly on Tuesday. Losers beat winners at the NYSE by a seven-to-six margin and by less than a smidgen at the Nasdaq. While advancing volume took just a 42.4% share of composite NYSE-listed trade on Tuesday, advancing volume easily took a majority share (55.7%) of composite Nasdaq-listed activity. Interestingly, aggregate trade was sharply lower on Tuesday from Monday's levels.

Activity ebbed across NYSE-listings, across Nasdaq-listings and across the membership of the S&P 500. This essentially rendered the day's price discovery results or technical activity somewhat less significant than it might have been otherwise.

The Tuft of Flowers

(excerpt)

I thought of questions that have no reply,

And would have turned to toss the grass to dry;

But he turned first, and led my eye to look

At a tall tuft of flowers beside a brook,

A leaping tongue of bloom the scythe had spared

Beside a reedy brook the scythe had bared.

I left my place to know them by their name,

Finding them butterfly weed when I came.

The mower in the dew had loved them thus,

By leaving them to flourish, not for us.

- Robert Frost (1913)

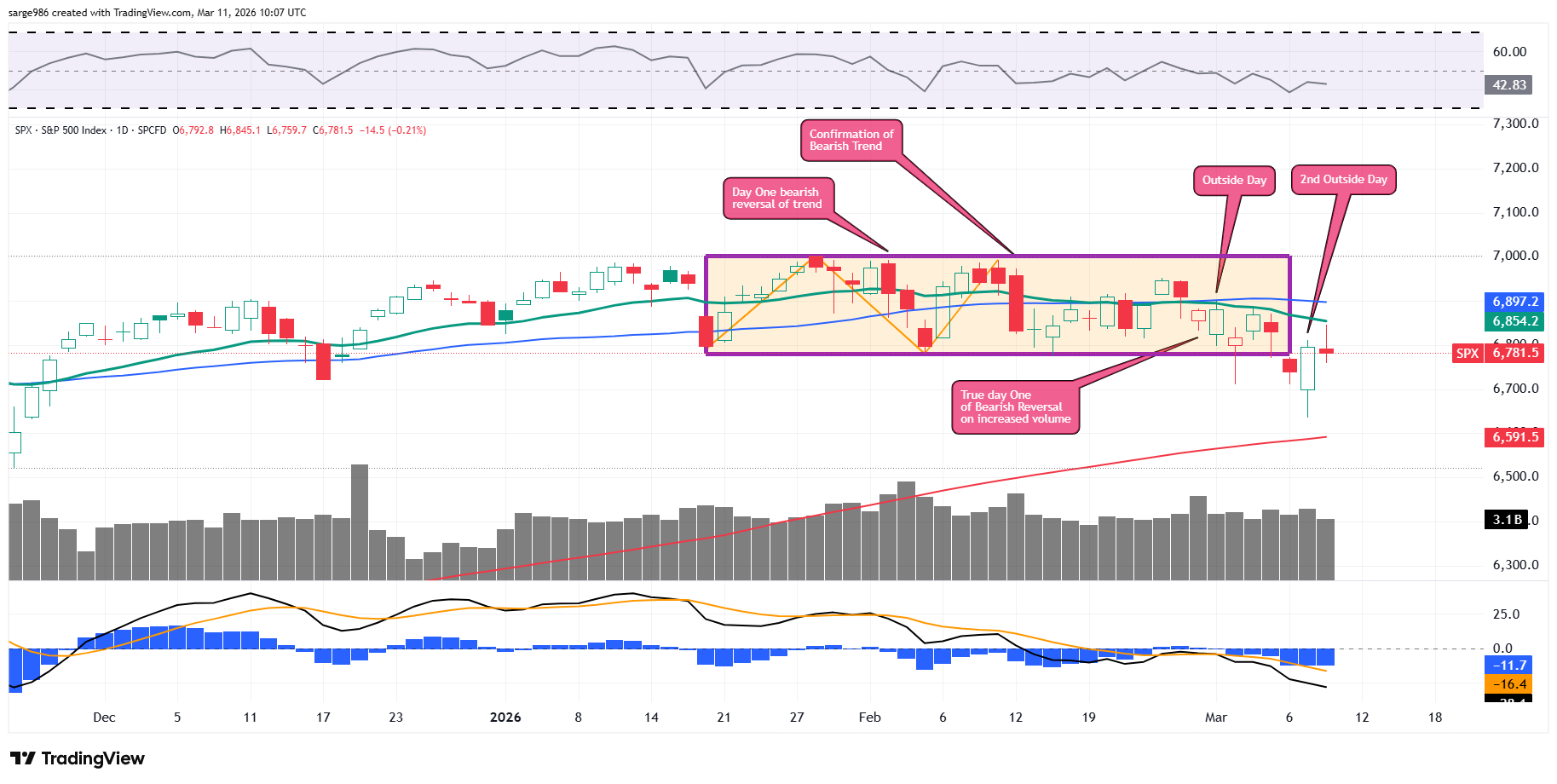

The Chart

Note that the "outside day" on Monday did indeed produce some volatility as it had signaled. Troubling? Though the activity took Tuesday's candlestick back above the lower trendline (support) the recently completed basing period, the index was again repelled at its own 21-day exponential moving average This implies that swing traders are still probably net sellers.

To make any real progress, we are going to have to see a run at that 50-day simple moving average (blue line) if we are going to get professional money to significantly increase long-side exposure. On that note, Relative Strength has been weaker than neutral for most of March. The daily moving average convergence divergence is still postured more like a train-wreck than anything else.

Key to Watch

This afternoon, the U.S. Treasury will go to auction with $39 billion worth of new Ten-Year Notes. This event will come just a couple of hours after influential Fed Gov Michelle Bowman speaks in Washington. Though Bowman is scheduled to speak on bank capital rules, she has been more of a policy dove than hawk of late and the floor will be opened to the financial media for a Q&A session. There is a distinct possibility that Bowman impacts that auction and that the auction, in turn, impacts how financial markets close this evening.

Economics

(All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.09%.

07:00 - MBA Mortgage Applications (Weekly): Last 11.0% w/w.

08:30 - CPI (Feb): Expecting 0.3% m/m, Last 0.2% m/m.

08:30 - Core CPI (Feb): Expecting 0.2% m/m, Last 0.3% m/m.

08:30 - CPI (Feb): Expecting 2.5% y/y, Last 2.4% y/y.

08:30 - Core CPI (Feb): Expecting 2.5% y/y, Last 2.5% y/y.

10:30 - Oil Inventories (Weekly): Last +3.475M.

10:30 - Gasoline Stocks (Weekly): Last -1.704M.

1:00 - US Ten-Year Note Auction (Weekly): $39B.

2:00 - Federal Budget Statement (Feb): Last $-95B.

The Fed

(All Times Eastern)

07:30 - Speaker: Reserve Board Gov. Michelle Bowman.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: (CPB) (.57)

After the Close: (PATH) (.25)

At the time of publication, Guilfoyle was long JPM equity