Ackman Aims to Be the Next Buffett, Nvidia Rises Up and More Tariff Talk

Pershing Square honcho sees Howard Hughes Holdings as 'a modern-day Berkshire Hathaway;' also we chart Nvidia and look at the reaction to Trump's latest tough talk.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

From his Mar-a-Lago club in southern Florida on Tuesday, Pres. Trump spoke of what might be his next batch of tariffs. How did domestic equity index futures seem to be reacting overnight? Ho hum. (They are flat to slightly lower.)

The president mentioned placing these duties on automobiles, semiconductors and pharmaceuticals. The tariffs would be "in the neighborhood of 25%," he said, but added that these rates could "go very substantially higher over the course of the year."

Why haven't traders, or more realistically, keyword reading algorithms reacted negatively to the president's words as they have in the past, as Tuesday evening poured into the zero-dark hours of Wednesday morning? Really, for a number of reasons. There is the more ongoing and in the long run, far more important to business, discussion in congress of extending the 2017 tax cuts. Then there is also serious progress being made globally in terms of creating, for the US, a "peace" dividend.

As within a matter of weeks, the Middle East and eastern Europe have become either safer neighborhoods, or are at least talking about it, the prospect for a refocusing of recklessly spent taxpayer funding comes closer to reality. This possibility moves from fantasy to the realm of what might be as Elon Musk's DOGE crew finds mis-allocated, fraudulent and / or irresponsible fiscal behavior throughout the federal government.

My one concern there is that as the federal government had become such a large employer over recent years, that the labor market unemployment rate had settled well below the natural rate of what economists used to consider normal at full economic (not labor market) employment. (Full employment in labor markets and full economic employment are not the same thing.)

If, after the federal government cuts the fat, and eliminates less than necessary positions, putting government employees at the same level of real-world risk as those working in the private sector, can the public... and can the media get used to the idea of a "healthy" economy where unemployment runs at 5% to 6% and not at 4% and below? This question is what runs through my head as darkness reigns. I don't know the answer. Neither do the dingbats at the Fed nor in academia.

On Peace...

Secretary of State Marco Rubio stated that sanctions on Russia would stay in place until there is, in fact, a deal where peace has been reached and the violence in Ukraine has ended. On the other side, Kremlin spokesperson Dmitry Peskov implied to his media that there could be a Trump-Putin meeting prior to the end of the month. In the meantime, U.S. Secretary of the Treasury Scott Bessent has offered and is continuing to work toward a deal with Kyiv where the Ukrainian side would trade a rough half of the value of that nation's vast mineral rights to the U.S. in exchange for past and future aid as well as a possible security guarantee.

Marketplace

Treasury debt securities suffered a little bit of a smackdown on Tuesday, even if equities were able to avoid a similar fate. As the major equity indexes traded in a narrow range for the session and had to wait for a late algorithmically driven rally to close in the green on Tuesday, the yield paid by the U.S. Ten Year Note popped 7 basis points to 4.56%, while the yield for the Two-Year Note moved 4 basis points higher to 4.31%. These yields have not strayed far overnight.

The S&P 500 bottomed for the regular trading session a little after 2 p.m. (NY time) on Tuesday and then meandered almost up to the doorstep of the closing bell when with about nine minutes left in the session. That's when the algos started buying everything in sight. Stocks surged into the closing bells at the corner of Broad and Wall streets and up at Times Square. The S&P 500 gained 0.24% for the day, closing at a new all-time high, as the Nasdaq Composite tacked on just 0.07%. Note that the Nasdaq Composite held its own on Tuesday despite receiving no help from the "Magnificent Seven."

You read that right. Smaller caps outperformed the broader marketplace on Tuesday, with the Russell 2000, S&P SmallCap 600, and S&P MidCap 400 gaining 0.45%, 0.52% and 0.86% respectively as Alphabet GOOGL, Meta Platforms META, Amazon AMZN, Tesla TSLA and Apple AAPL all closed in the red. Among the Mag 7, only Nvidia NVDA and Microsoft MSFT posted daily wins.

Breadth

On Tuesday, eight of the 11 S&P sector SPDR exchange-traded funds shaded into the green for the session, led by Energy XLE and the Materials XLB. Those two funds rallied 1.37% and 1.27% respectively on the day despite the lack of U.S. dollar weakness that often accompanies strength in commodity driven sectors. Communication Services XLC was the dog of the day, down 0.47% as the Dow Jones U.S. Internet Index gave up 1.48%.

This is somewhat interesting. Winners beat losers by a rough 5-to-4 margin at the New York Stock Exchange for the day and by about 7 to 6 at the Nasdaq Market Site. Advancing volume took just a 48.7% share of composite NYSE-listed trade, but a 57.7% share of composite Nasdaq-listed activity.

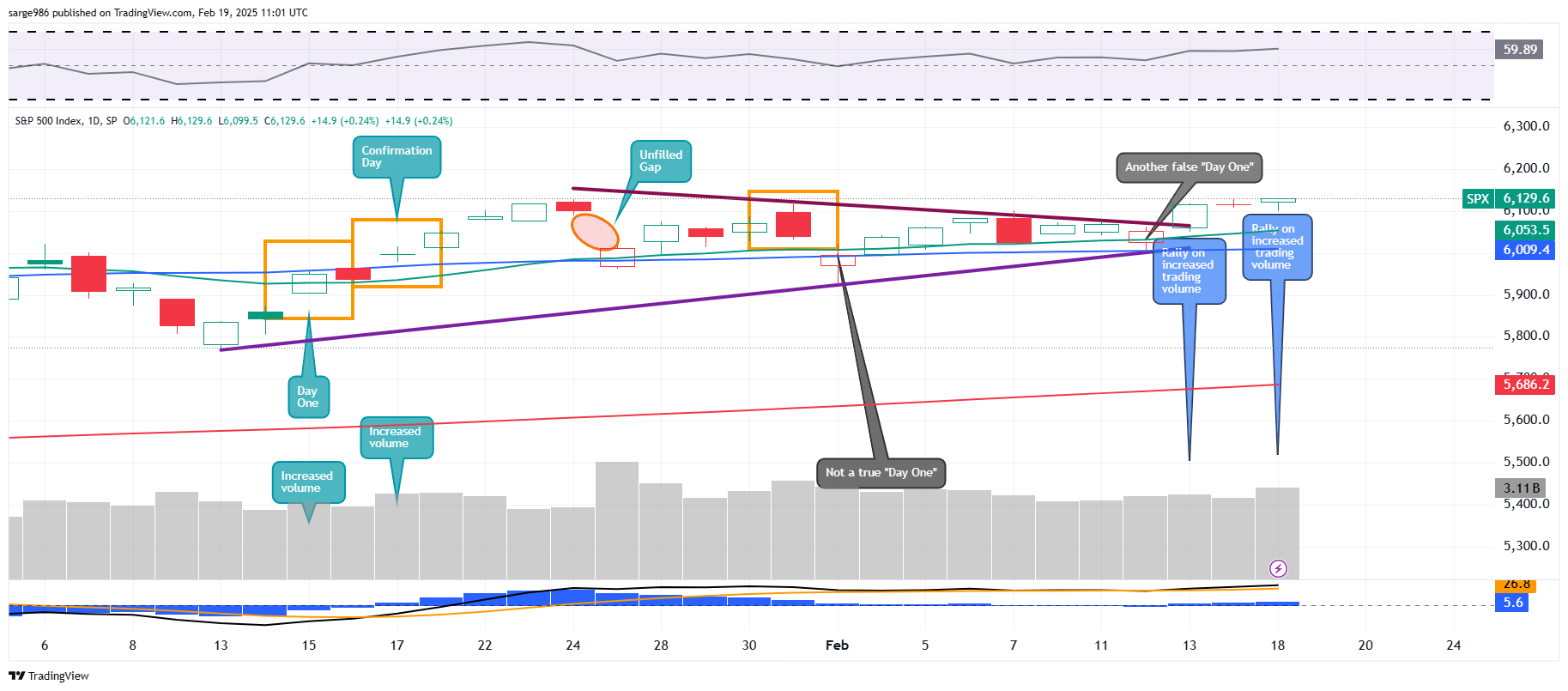

Did it all matter? Aggregate trading volume contracted on a day-over-day basis across the listings of both the NYSE and the Nasdaq, but increased across the membership of the S&P 500. That's where the late surge was. That's where the all-time high was. So, yes, there was something meaningful behind Tuesday's late afternoon push.

Readers will note in the chart below that aggregate trading volume across the S&P 500 has increased on a day over day basis both on Thursday and Tuesday, which were both green candle sessions, while the sluggish Friday session that those days sandwich suffered a contraction in trading volume. This would be considered a technical positive for the index.

Say What, Ackman?

Billionaire investor Bill Ackman of Pershing Square spoke on Tuesday and mentioned that his business had submitted a proposal to acquire 10 million newly created shares of Howard Hughes Holdings HHH for $90 per share. This is up from January, when Ackman had offered current shareholders $85 per share.

The newly proposed transaction would not require regulatory approval, financing, nor shareholder passage. Hence, the whole deal could close within weeks and would leave Pershing Square with 48% of HHH, with Ackman assuming the roles of chief executive and chairman.

Ackman posted on X (formerly Twitter): "We will make available the full resources of Pershing Square to HHH to build a diversified company, or one could say a modern-day Berkshire Hathaway (BRK.A, BRK.B)." Ackman has expressed admiration in the past for 94-year-old Berkshire Hathaway CEO Warren Buffett. Ackman commented that Howard Hughes would continue to develop real estate or "master planned communities" in the Houston, Texas and Las Vegas, Nevada areas as he pursued his agenda.

Holy Toledo, Batman!

Nvidia shares may have sold off 11% after cracking its downward pivot created by a double-bottom pattern that culminated in January.

The stock may have given up more than 20% in the wake of the DeepSeek news before bottoming on Feb. 3. Since then? It does not appear that these investors are overly concerned over the threat posed by DeepSeek and other startups looking to find ways to write large language models for generative AI-training less expensively.

Call it a "February to Remember": NVDA has recaptured 27% since that Feb. 3 bottoming, while also taking back its 200-day and 50-day simple moving averages, forcing portfolio managers to increase long-side exposure and its 21-day exponential moving averages, which got the swing crowd onsides. All hail CEO Jensen Huang? I'll let you know next Wednesday (a week from today) when Nvidia reports fourth-quarter earnings. Rock & Roll.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.95%.

07:00 - MBA Mortgage Applications (Weekly): Last 2.3% w/w.

08:30 - Building Permits (Jan): Expecting 1.46M, Last 1.482M SAAR.

08:30 - Housing Starts (Jan): Expecting 1.395M, Last 1.499M SAAR.

08:55 - Redbook (Weekly): Last 5.3% y/y.

1:00 p.m. - Twenty Year Bond Auction: $16B.

4:30 - API Oil Inventories (Weekly): Last +9.043M.

The Fed (All Times Eastern)

2:00 p.m. - FOMC Minutes.

5:00 - Speaker: Federal Reserve Vice Chair Philip Jefferson.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ADI (1.54), ETSY (1.46)

After the Close: CVNA (.32), NDSN (2.08)

At the time of publication, Guilfoyle was long AMZN, NVDA, MSFT, BRK.B equity.