Accentuating the Positive

Apple and Intel power higher in the premarket, Trump talks tough on tariffs, price data lands this morning; also let's chart the markets.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

U.S. equity markets worked their way higher on Thursday, ultimately closing on strength after what had been quite the volatile session. Markets opened higher, continuing the late Wednesday pop experienced after the Fed basically took a semi-hawkish pass that afternoon, but both Tesla TSLA and Meta Platforms META had reported well-received earnings and guidance after that close. Then stocks sold off fairly hard.

After that it was all uphill for stock prices with the exception of an algorithmic jitterbug that hit with about 20 minutes left until the closing bell. The upward momentum smoothed that spasm over rather quickly and the day's final 10 minutes were spent in rally mode. Last night, it was Apple's AAPL turn. The consumer electronics behemoth had a solid overnight session after first reporting disappointing iPhone sales but then providing positive service sector guidance. That, along with an assist by Intel INTC has domestic equity index futures trading moderately higher at zero dark-thirty on Friday morning.

On Tariffs

On Thursday afternoon, Bloomberg News reported that President Trump had spoken from the Oval Office and said: "We'll be announcing the tariffs on Canada and Mexico for a number of reasons. Number one is the people that have poured into our country so horribly and so much. Number two are the drugs, fentanyl and everything else that have come into the country. Number three are the massive subsidies that we're giving to Canada and to Mexico in the form of deficits."

The president added: “We don't need the products that they have. We have all the oil that you need. We have all the trees you need." That was an obvious reference to Canada.

The president also commented on China, "With China, I’m also thinking about something because they're sending fentanyl into our country, and because of that, they're causing us hundreds of thousands of deaths,” Trump said Thursday. “So, China is going to end up paying a tariff also for that, and we're in the process of doing that.”

What was incredible about these comments from a markets' perspective was that the financial marketplace largely yawned. Keyword-seeking algorithms tried to get some volatility going into the close, but the positive momentum at that time overran the negativity. The U.S. Dollar Index strengthened in the face of those comments and there was some minor selling from the belly of the US Treasury yield curve out to the long end, but equities traders cared not.

The president stated that the tariffs on Mexico and Canada would start at 25% for February, implying as he had upon his inauguration that these could hit as soon as this Saturday. The president did not confirm that oil would be included and said that a determination on crude had not yet been made.

Economic Growth

On Thursday morning, the Bureau of Economic Analysis published the agency's first of three estimates for Q4 2024 gross domestic product. The "real" number, accounting for the inflation deflator, printed at quarter-over-quarter growth of 2.3%, seasonally adjusted and annualized. This is a deceleration from the third quarter print of 3.1% and the slowest pace of U.S. growth since the first quarter of 2024.

The U.S. consumer was not the problem. Personal consumption expenditures printed at growth of 4.2%, the strongest quarter of growth for this category since the first quarter of 2023. The glaring weakness in the report showed up in gross private domestic investment. That category printed at a shocking -5.6%, ironically making this the worst quarter of growth for that category since the first quarter 2023. Private inventories were also a negative in the release, also for the first time since Q1 2023.

It does need to be said that the first estimate for quarterly GDP is often inaccurate and is highly susceptible to revision. The BEA also does not release an estimate for quarterly gross domestic income, with the first of the three GDP estimates, which makes it impossible to impose any kind of checks and balances on the results. On that note, we'll see you in a month.

This Morning...

The same BEA will release its data for December personal consumption expenditures and core PCE price inflation. The financial media will make a big deal out of this release, because it is "inflation data" and it is, "the Fed's preferred measure of inflation," and because they assume that you and I are simpletons. The fact is that the marketplace has long-ago priced in December inflation and is working on pricing in January and February inflation. The truth is that there are rarely any surprises in this report, which prints two weeks after the more closely followed monthly CPI release, that are significant enough to force a notable market reaction. Could it happen? Of course. Likely? Nah.

Equity Marketplace

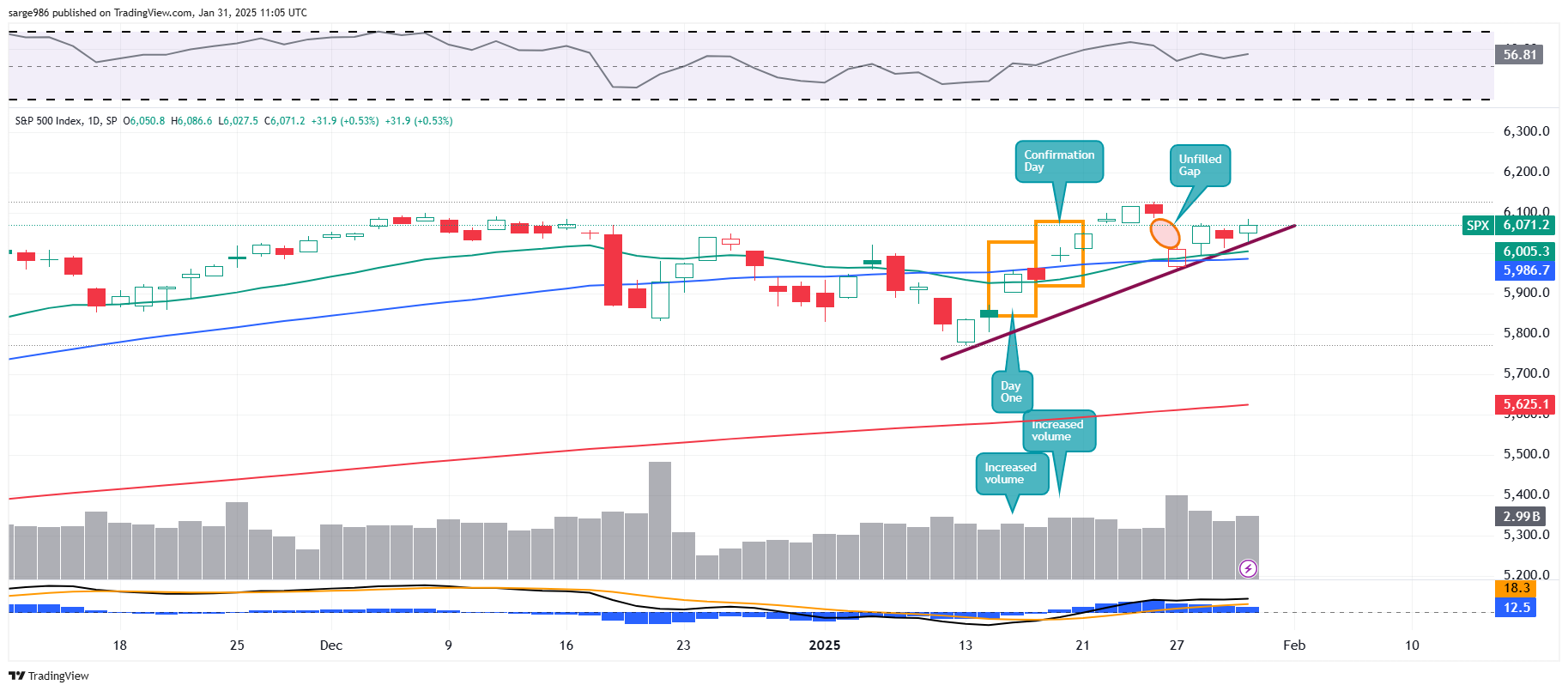

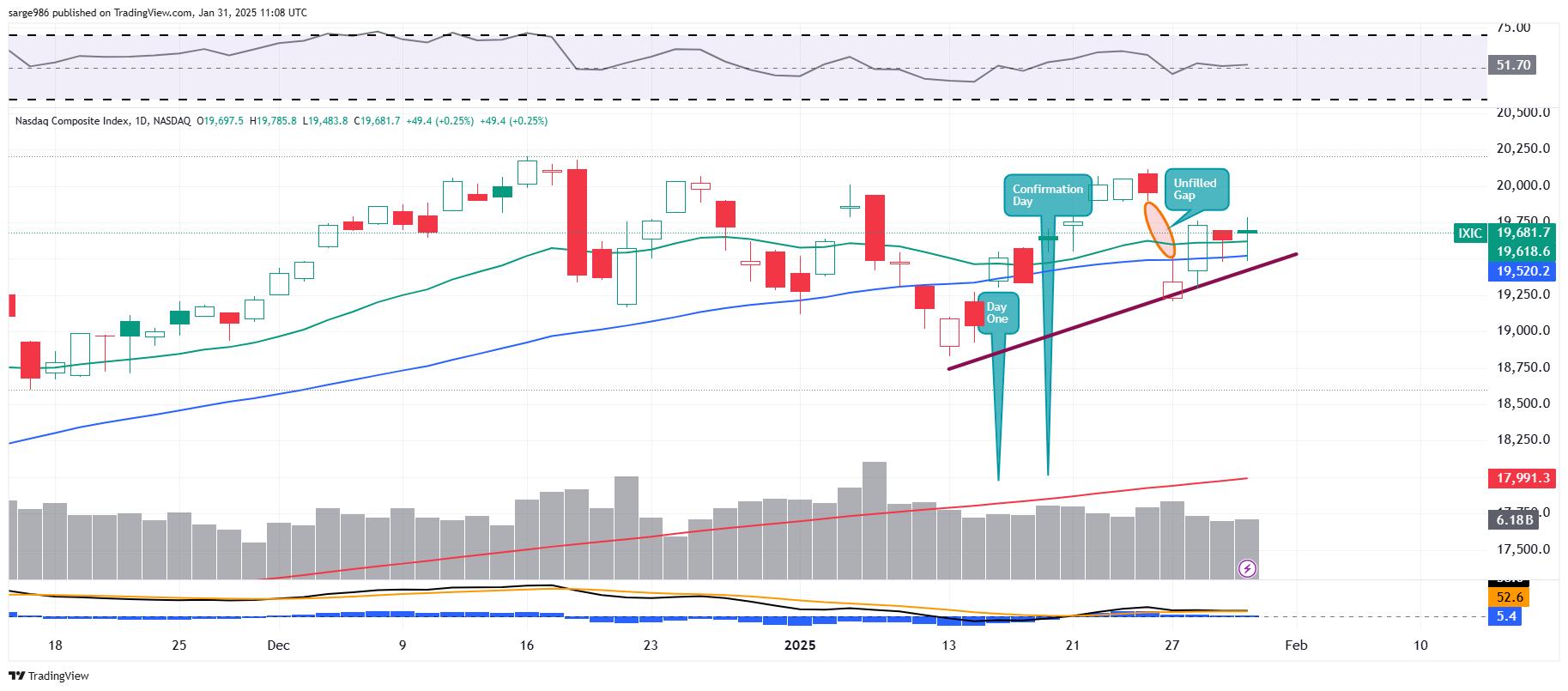

Thursday was a more important "up" day than many likely know. Yes, the mid-major to major indexes were all higher with the exception of the Dow Transports. The S&P 500 gained 0.53%, while the Nasdaq Composite picked up 0.25%. Better than that, the small to mid-cap indexes all rocked as did the semiconductors and the banks. The S&P 400, Russell 2000, Philly Semiconductors and KBW Banks popped for daily runs of 1.15%, 1.07%, 2.26% and 0.85% respectively.

In addition, all 11 S&P sector SPDR exchange-traded funds closed the day in the green, with the Utilities XLU leading the way at +2.08%. If there was a negative, it was in the order that these 11 funds closed out the session. The top three and four of the top five performing sector SPDRs on Thursday were all defensive in nature, while the bottom two performers were the two "growth" SPDRs.

Even with strength in semiconductors, the Tech XLK SPDR ETF closed up just 0.19% as the Dow Jones US Software Index gave up a nasty 3.53% for the day. The beat-down in software was caused by the 11.4% drop in ServiceNow NOW and the 6.2% selloff in Microsoft MSFT. No, I did not add to my long position in MSFT on weakness. I explained this in a deep-dive piece on Thursday here at TheStreet Pro. No, I did not initiate NOW despite swinging and missing on that name earlier in the week (Thank goodness). I am still considering an initiation there.

Breadth

This has me somewhat fired up. Winners beat losers at the NYSE on Thursday by a rough 7-to-2 margin and by about 2-to-1 at the Nasdaq. Advancing volume took a decisive 74.4% share of composite NYSE-listed trade and a 68.6 share of Nasdaq-listed activity. Now, here's the kicker. Aggregate trade increased by an impressive 12.6% day over day across names domiciled at 11 Wall St. and a "good enough" 2.8% day over day across Nasdaq-domiciled names. That appears to be quite meaningful coming after a week that included more than one "down" day that failed to qualify as a "day one" bearish reversal.

Note the trendline that I drew underneath the lows of the days for the S&P 500 that goes back to the low of Monday, Jan. 13 (Two days before I called a "day one" bullish reversal and running through the present). This line grazes a four-day series of rising daily lows that has lasted all week. Interesting? I think so.

It's not quite as precise for the Nasdaq Composite, but the rising trendline scraping the daily lows this week that goes back to January 13th is still evident. Positive reinforcement? I think it is.

Economics (All Times Eastern)

08:30 - Personal Income (Dec): Expecting 0.4% m/m, Last 0.3% m/m.

08:30 - Consumer Spending (Dec): Expecting 0.5% m/m, Last 0.4% m/m.

08:30 - PCE Price Index (Dec): Expecting 0.3% m/m, Last 0.1% m/m.

08:30 - Core PCE Price Index (Dec): Expecting 0.2% m/m, Last 0.1% m/m.

08:30 - PCE Price Index (Dec): Expecting 2.6% y/y, Last 2.4% y/y.

08:30 - Core PCE Price Index (Dec): Expecting 2.8% y/y, Last 2.8% y/y.

09:45 - Chicago PMI (Jan): Expecting 40.2, Last 36.9.

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 576.

1:00 p.m. - Baker Hughes Oil Rig Count (Weekly): Last 472.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ABBV (2.69), BAH (1.52), CVX (2.06), XOM (1.55)

At the time of publication, Guilfoyle was long XOM, INTC, MSFT equity.