A Little Panic Would Be Helpful

Why is this decline different from others? A lack of panic.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Panic. It’s an odd concept to most outside the markets.

To most, they think of a horror movie where they get scared or panicky, and their heart races. Or maybe they know someone who suffers from panic attacks when in certain situations. But in markets most traders would welcome some panic. You know the signs: a massive volume day where 90% of the volume is on the downside as people panic to get the heck out of the market, often on some scary news.

And getting out is not enough in a panic, they usually feel they need to hop the fence from bull to bear. Meaning selling is not enough, now they must buy puts as well. Because if you are going to raise cash you may as well also profit from your newfound bearish market stance.

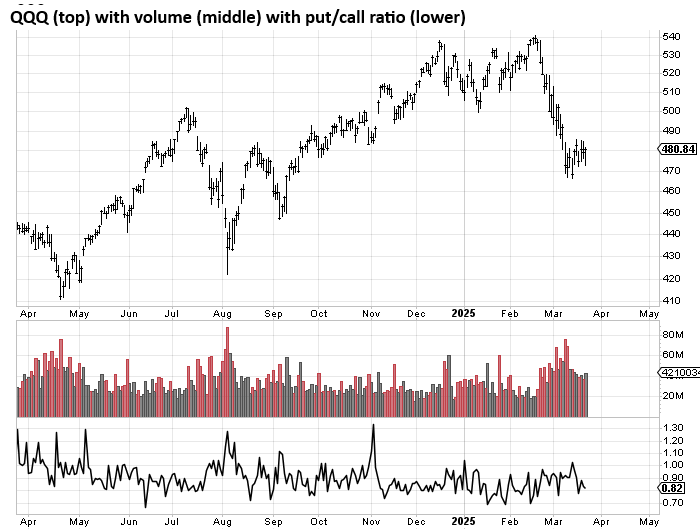

We saw panic last summer when the Yen carry trade collapsed. We saw a modicum of panic in April of last year where I can’t even recall what the scary news was (banks?). In April, we clearly see the rise in volume. We can see there were several spikes in the put/call ratio, well over 1.20 on this chart of the QQQs.

In August, we see it too. Big volume, big spike in the put/call ratio. Heck, we even saw this desire to load up on puts before the election, although there was no commensurate rise in volume (the decline was minimal).

But the recent ten percent-plus decline in the QQQs has only seen a rise in volume, with no spike in the put/call ratio. And that rise in volume never amounted to a big downside percentage. In fact, the only 90% day we have seen thus far was Friday, March 14th, and that was on the upside as if folks were panicking to get in, not out.

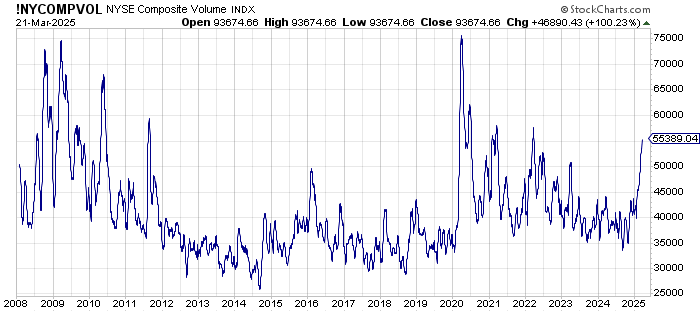

How else do we know this particular decline is different than the others? Look at the rise in NYSE volume. This is the 20-day moving average of NYSE volume. All those other spikes that resemble this one came amid panic. The 2020 Covid Panic is very clear; it was a little bit more, volume-wise, than what we saw in 2009. Both panicky situations.

But even all the other spikes came amid panic. Not this one. This one sees a rise in volume from persistence, not panic. The selling is persistent, not panicky, the put buying is absent. It’s probably because there isn’t one piece of real scary news, there is just a tariff deadline everyone has focused on.

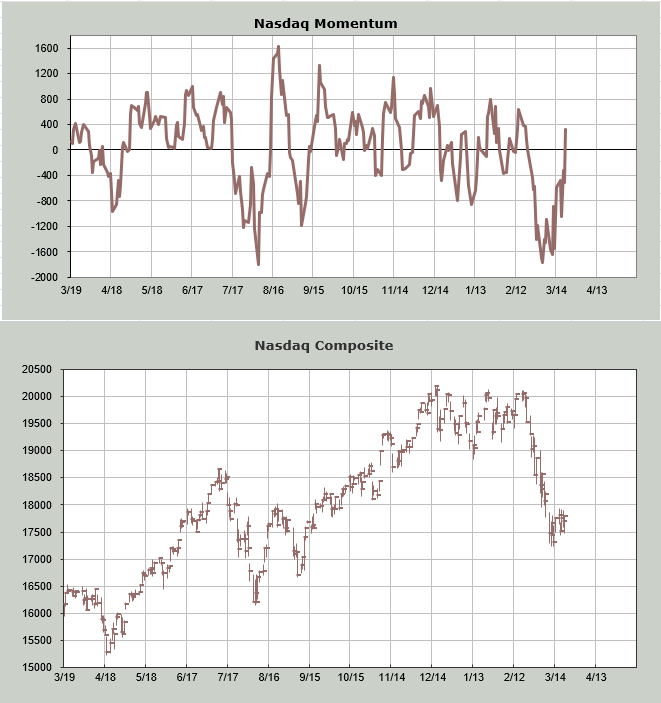

Aside from my own Oscillators, I like to use the Nasdaq Momentum Indicator, which is based on price (my Oscillators are based on breadth). You might recall it got oversold just over two weeks ago. Look how the indicator has surged. Now, notice how there has been no commensurate rally in Nasdaq. All we’ve seen is a lessening of the downside momentum (what oversold is), but the other side of the equation (a rally) has been absent. That, too, shows a change.

Maybe we don’t need panic, but panic would be helpful. So would a spike in the put/call ratio.