A Curious Thing Has Happened After the Market 'Jumped the Gun'

There's a change in the nature in the market that warrants monitoring. Let me explain. Also, a look at the equity put/call ratio, the AAII bull-bear spread and more!

You've reached your free article limit

You've read 0 of 1 free Pro articles.

My apologies for the delay but it seems some vandals in my neighborhood get a charge out of cutting the fiber cable. It went out about an hour before the market closed Wednesday and did not come back on until 2 a.m.

Once again they tried to sell the market off and couldn’t break much if anything. As has been typical of the last three weeks I can argue both sides. The one thing I find most curious is that the S&P 500 closed at the same price on Wednesday that it closed on January 21 (okay, two-point difference). If you recall that was the timeframe we were to get short- and intermediate-term oversold.

The market jumped the gun and began the rally a few days earlier than that. In the last few years that hasn’t been an issue, jumping the gun on an oversold condition. This time the market was not able to run for very long off that oversold (and too bearish) condition.

For the last two years jumping the gun hasn’t meant a short runway, at least not for the S&P and the index movers. That is a change in the nature of the market we must monitor.

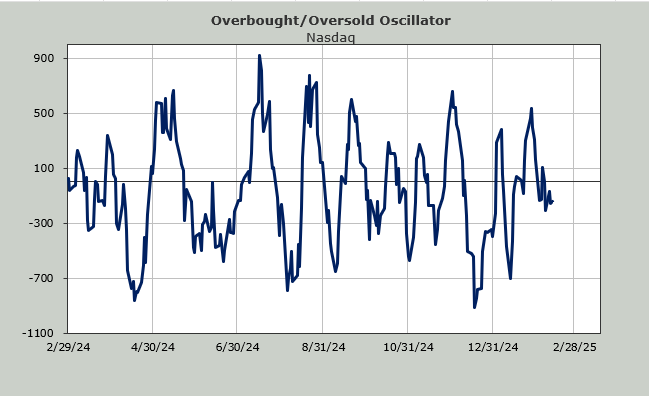

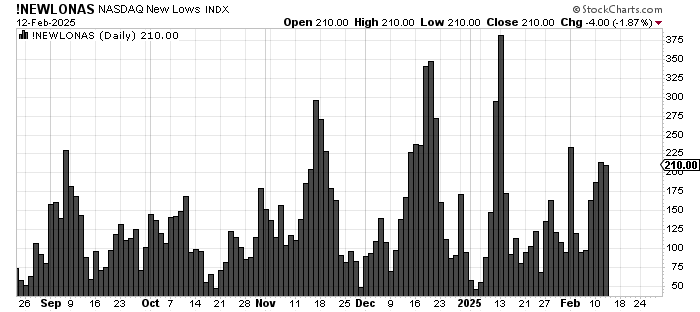

As for any changes in the indicators, here’s the bullish side of the ledger: The Russell 2000 made a new closing low (not an intraday one) and there were fewer stocks making new lows on Nasdaq vs. February 3.

One other change is that — and this is so minor it feels ridiculous to even mention it —the equity put/call ratio was 0.56. For me that leans on the low side, although it is quite minor. The change is that it is the highest reading since January 29. So the appetite for equity calls cooled a smidge. And for the first time in three days we did not have a penny stock that traded more than a billion shares on the Nasdaq.

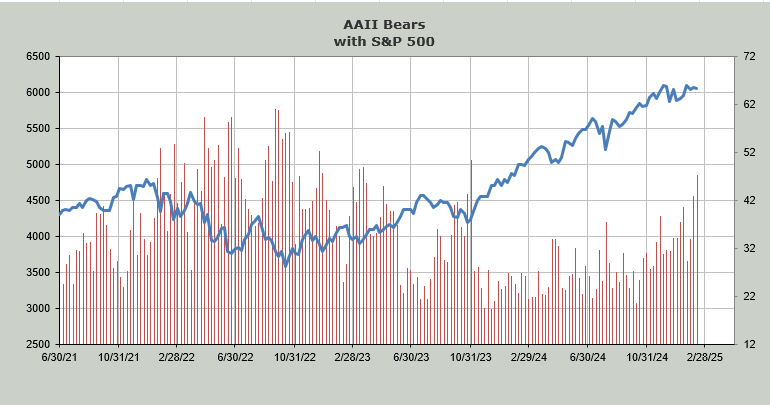

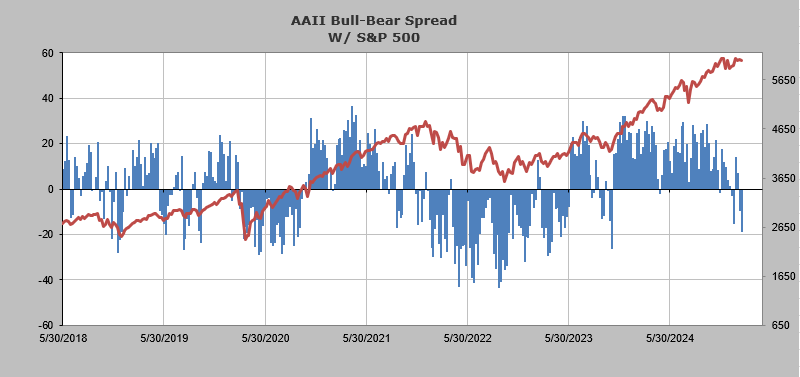

This morning the AAII survey showed a marked decrease in bullishness and all the bulls seemed to jump to the bear side of the ledger. The bulls are 28.4% and the bears are 47.3% so we have the most bears since the October 2023 lows when we had 50%.

Two things struck me when I looked at this survey today. First, if nothing has changed in the market, then the spread between bulls and bears, now at nearly 19 points should be bullish. But if you glance over at the 2022-2023 time frame, that spread (more bears than bulls) stayed wide for more than a year.

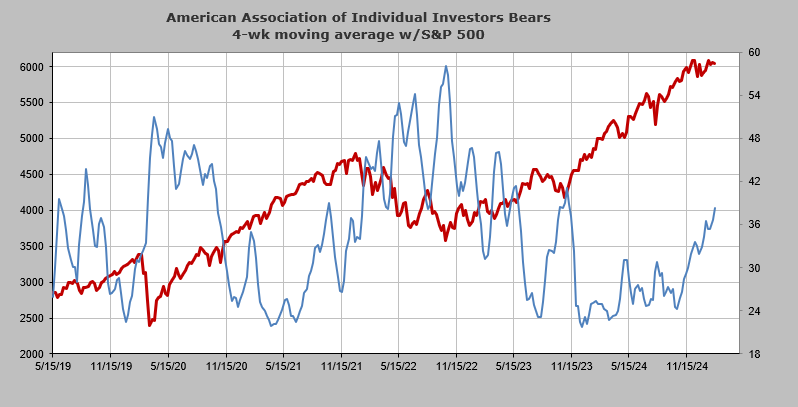

I also like to look at the four-week moving average of bears, which is high and rising. Again, if nothing has changed, this ought to be bullish. But look aver at the fall of 2021 and into 2022 and you will see it remained elevated and therefore wasn’t bullish then.

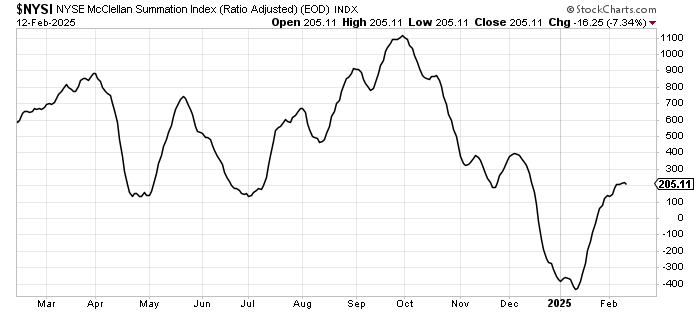

One other change is that the McClellan Summation Index has barely budged this week but it now needs a net differential of +900 advancers minus decliners to turn it back up. We entered the week with that number at +200. Again, it’s a minor change.

Finally, I should address the bonds. We went back up over 4.55% in yield on the 10- Year so I’m wrong to think rates will tag that line at 4.3%.

The DSI is at 22 so it is on the verge of saying folks are too bearish bonds. I am honestly not sure which side of the ledger bonds should be right now.