You Rolled Over Your 401(k): Now What?

What should you invest in after moving your retirement savings?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Remember 2023? The S&P 500 came roaring back, finishing the year with a 26% gain after its 2022 decline. On a 10-year basis, the S&P was up nearly 160%.

Late that year, I was talking to a friend at a party in Santa Fe. She couldn’t understand how her accounts (I have no idea what type of account it was) were languishing while the S&P had shown those kinds of gains.

It turned out that she was sitting mostly in cash, as she believed that to be safe. There wasn’t much of a mystery there, but it turns out she wasn’t alone in leaving her money parked in cash.

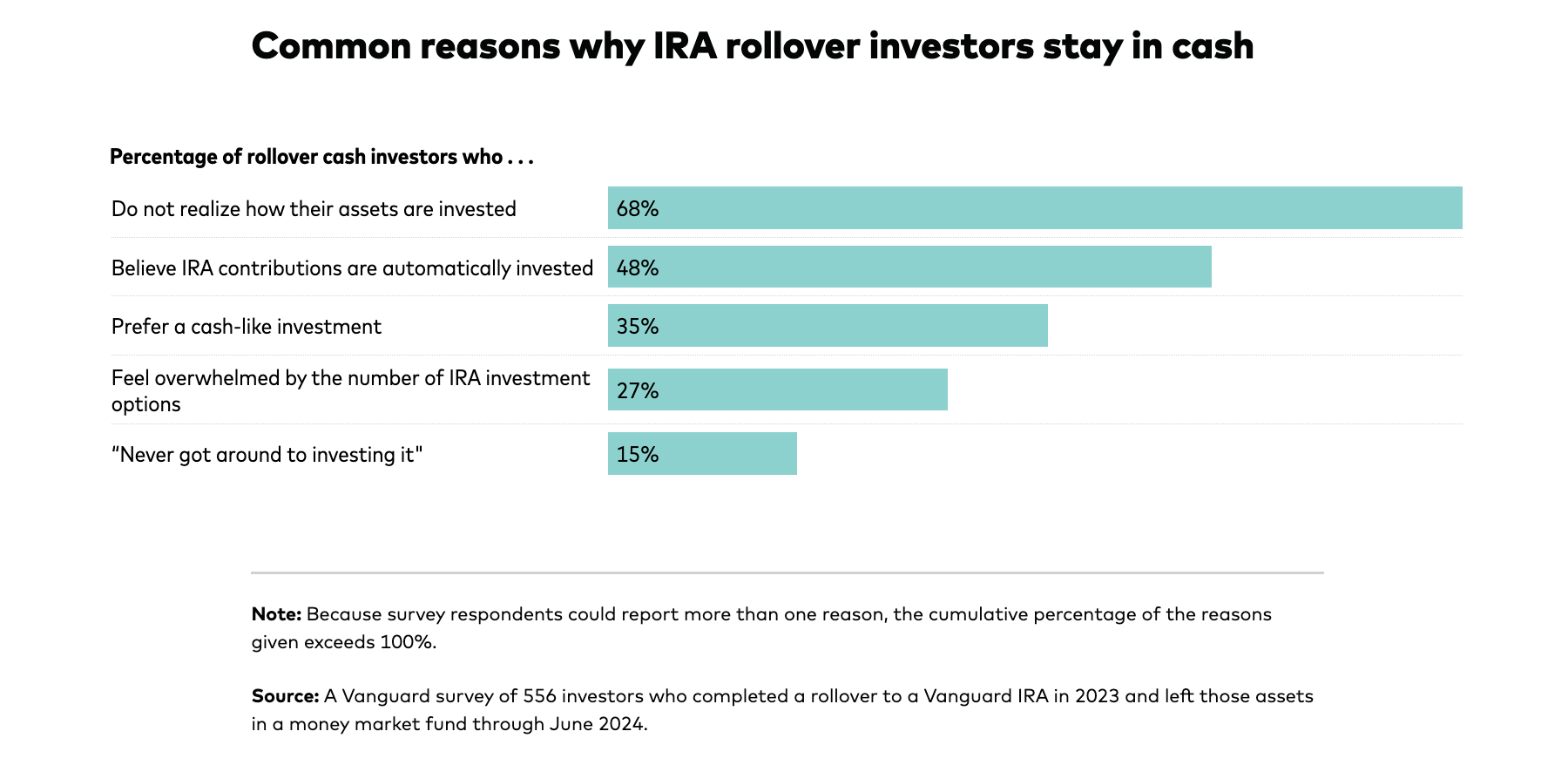

According to a 2024 report from Vanguard, “Out of Sight, Out of Market: The IRA Cash Drag,” a large number of investors who roll employer-sponsored retirement plans to an IRA leave the money untouched, sometimes for years.

This illustration from Vanguard shows you the main reasons that happens.

Nearly 90% of IRAs are rollovers from defined contribution plans, rather than direct contributions.

Frequently, rollovers arrive at the new custodian in the form of cash. That’s because invested assets are liquidated, since the new custodian can’t necessarily hold the funds which are often specifically designed for 401(k) plans.

That liquidation process unwinds the age-appropriate allocations typical in 401(k) accounts. Unless the account owner reinvests the money, it will sit in cash.

Note: If you work with an investment advisor or financial planner, they’ll either facilitate that process for you directly, or give you instructions on how to reinvest the money.

Get the Money Out of Cash

So what should you do once your money lands in the IRA?

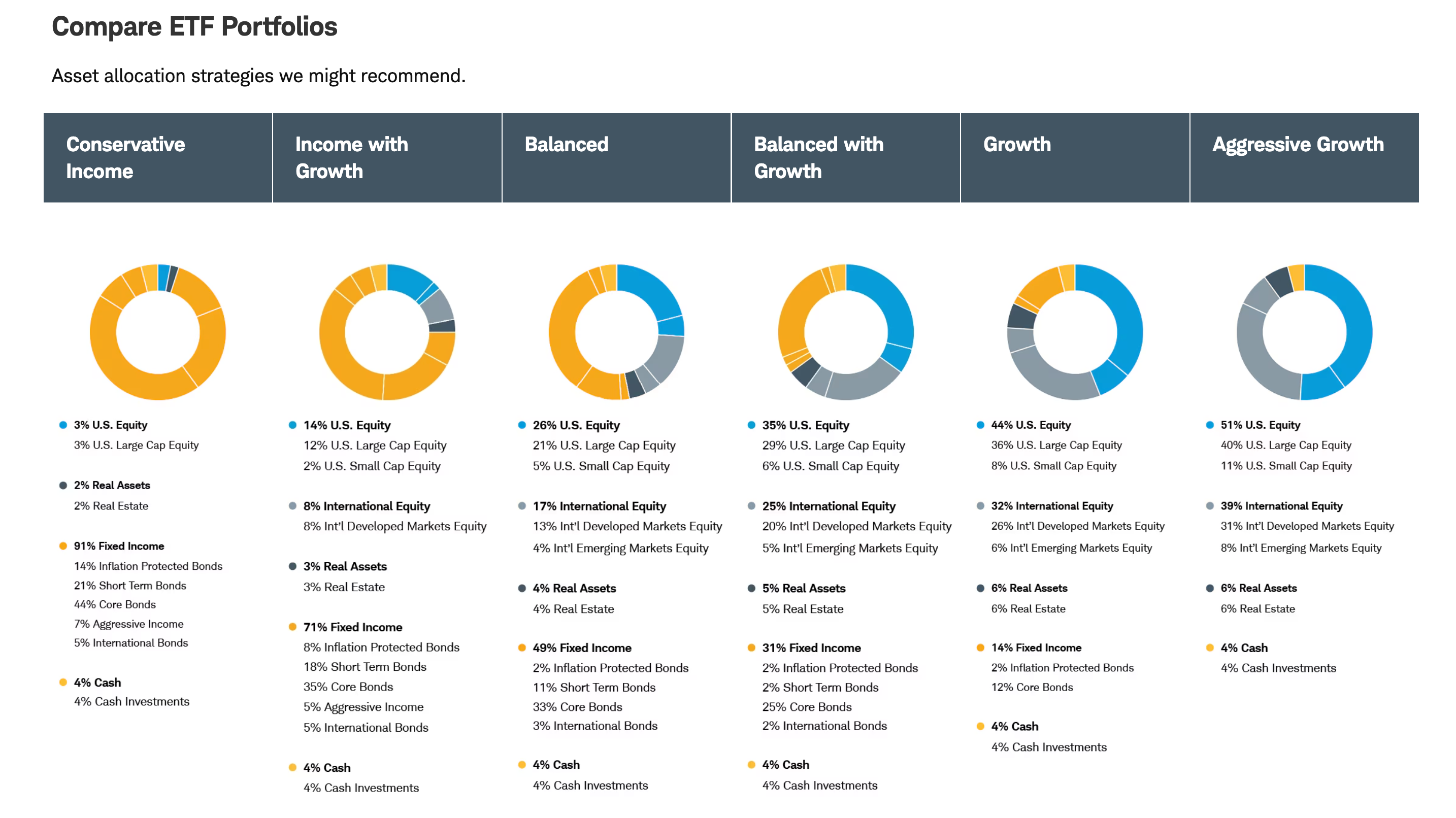

If you’re building an investment mix, you don’t have to start from scratch; there are already plenty of model portfolios offering a mix of assets that can be adjusted to match your situation.

According to a June 2025 article published by brokerage Charles Schwab, “The Role of Various Asset Classes in a Portfolio,” the ideal investment mix should hold an appropriate blend of stocks, bonds and cash.

“Each of these plays a unique role in your portfolio, providing the potential for growth, income, and stability. By adjusting how much you own of each asset class, you can adjust the risk/reward potential in your portfolio to create a mix that suits your financial goals and time horizon.”

Mark Riepe, Charles Schwab managing director

For example, this graphic shows some models that Schwab presents as guidelines for investors.

There's a lot going on here, but implementation is actually simple: If you look closely, you’ll see that it’s broken down into sub-assets.

These distinctions highlight how different types of stocks and bonds play specific roles in balancing risk, generating income and supporting long-term growth.

Schwab’s framework, which aligns with other portfolios designed around common retirement goals, balances income, balanced growth and total return.

These allocations aren’t just theory; they reflect the typical asset mixes Schwab uses in managed client portfolios.

Understand the Risk and Return Tradeoffs

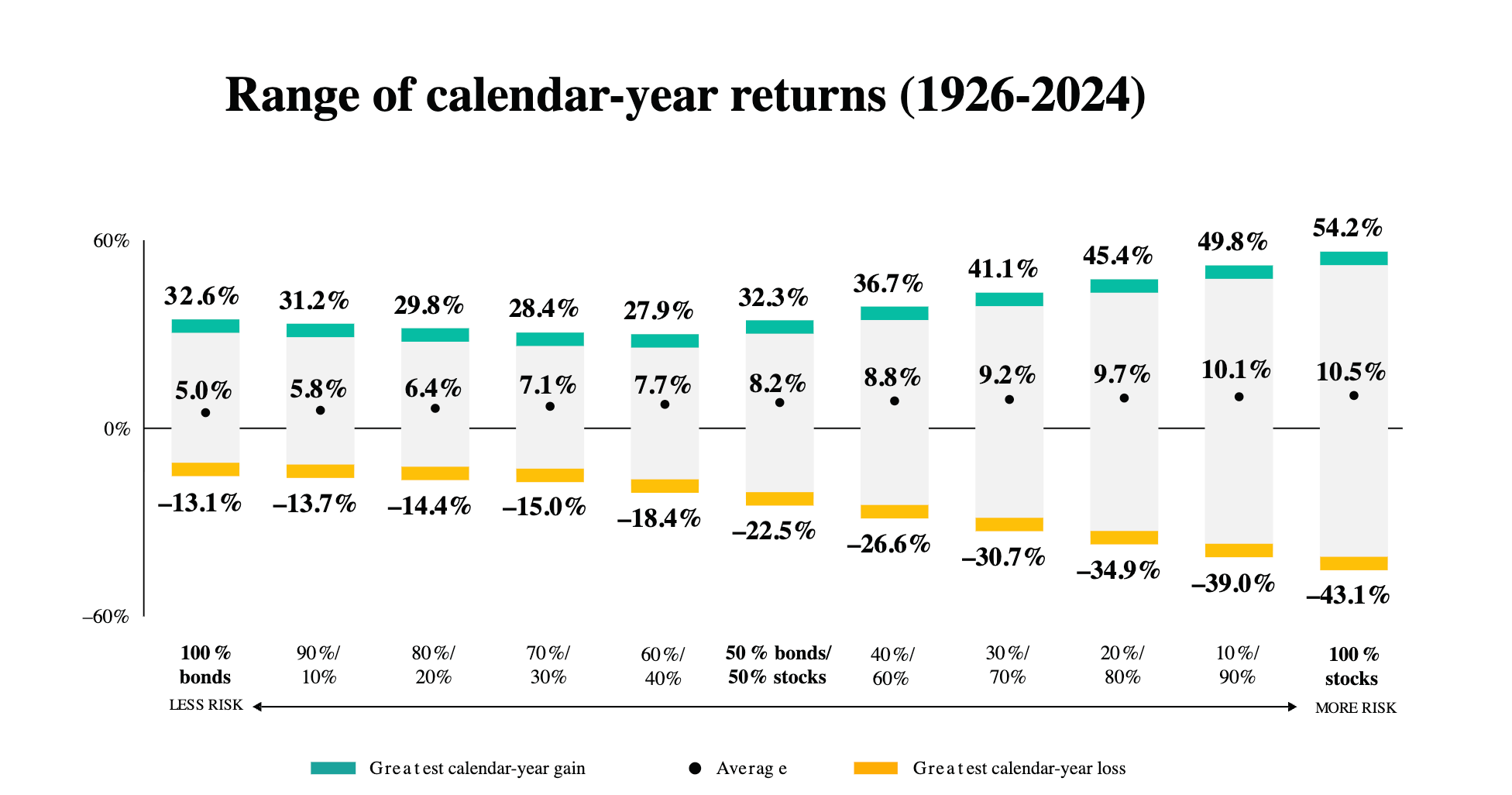

Before choosing an allocation, it’s helpful to see how different stock-bond mixes perform historically. Vanguard’s model portfolio guide includes a bar graph showing average returns, worst-year losses, and volatility levels for allocations ranging from 20/80 to 80/20.

For example, a 60/40 portfolio historically returned about 8.8% annually but lost 27% in its worst year.

A 40/60 portfolio returned less, about 7.8%, but had lower volatility. That’s your tradeoff right there.

For stock traders who have an ingrained mentality that nabbing the most money possible from any transaction, the idea of intentionally managing risk may seem foreign.

I’ve worked with plenty of folks who initially had that mindset. A look at financial planning projections always (as in 100% of the time) helps them understand the connection between minimizing risk and getting the income they’ll need.

This bar chart gives you a terrific way of comparing different portfolio allocations, showing how a mix of stocks and bonds affects investment performance:

Portfolios with more stocks offer higher average returns but come with greater year-to-year ups and downs.

As you move left to right on this chart, going from 100% bonds to 100% stocks, both the best and worst annual returns grow wider, illustrating the tradeoff between risk and reward.

Avoid the 'Too Much Cash' Trap

While it’s tempting to play it safe in retirement, being too conservative can backfire, as we saw in the example of my friend who socked away all her money in cash. Many retirees underestimate how long their money needs to last, and how inflation can erode purchasing power over 20 or 30 years.

“IRA cash is a billion-dollar blind spot. Many IRA holders want to invest their retirement savings in the stock market and think that they’re invested following a rollover. In reality, they’re sitting in money market funds.”

Andy Reed, head of investor behavior research at Vanguard

Choose Intentionally, Not Automatically

Rolling over a 401(k) is usually a smart move. It gives you more control over your investments, but also the responsibility to allocate thoughtfully.

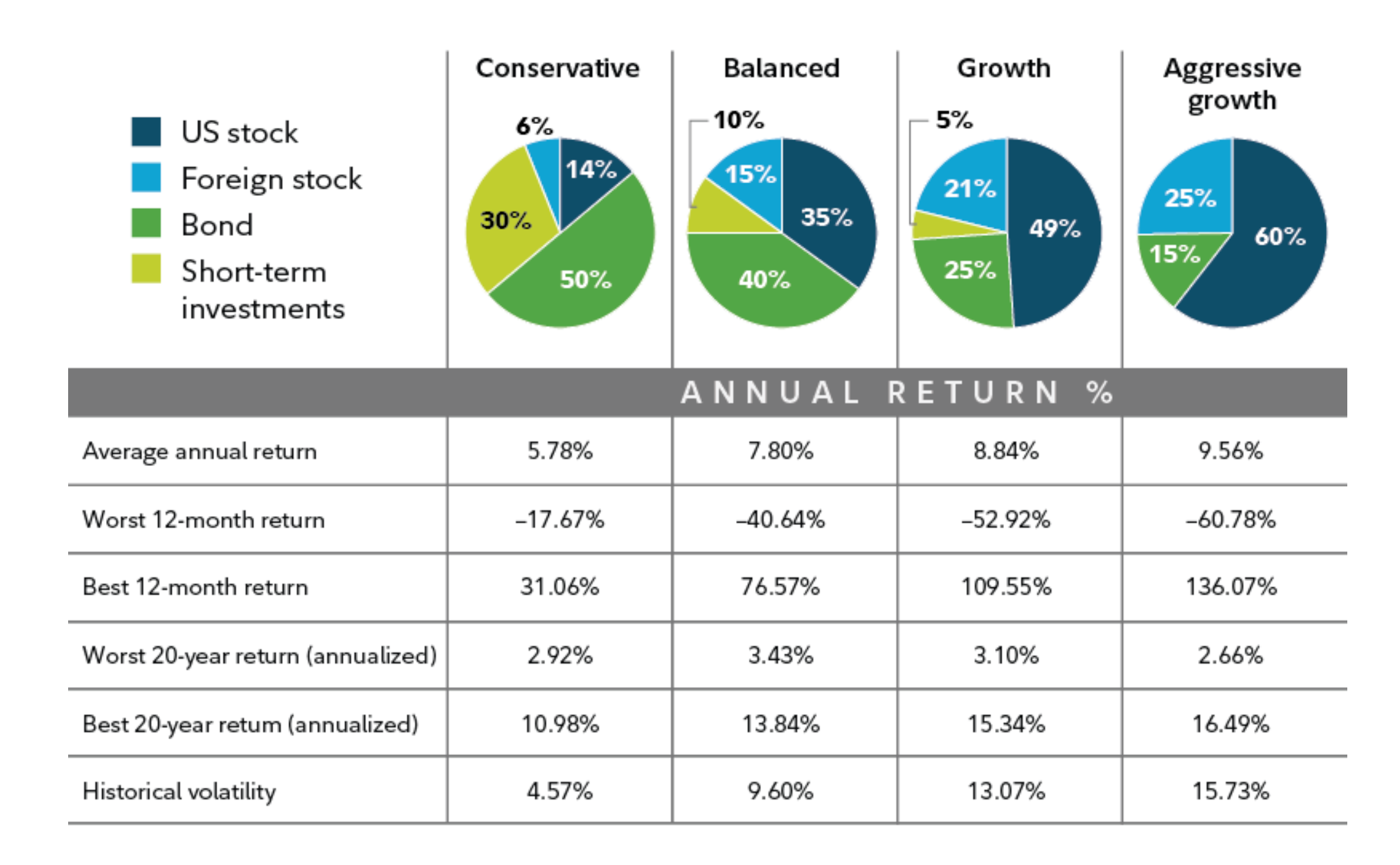

This chart from Fidelity makes a clear case against letting your rollover sit in too much cash.

While conservative assets are a key component of retirement portfolios, the conservative allocation on the far left on this chart is heavily weighted toward cash and bonds. It produced the lowest average returns over time.

In contrast, portfolios with more equities delivered significantly higher long-term growth.

For retirees, this is a reminder that playing it too safe can cost you: Staying in cash may protect against short-term swings, but it also limits the compounding power your retirement savings need to last 20 or 30 years. Getting your rollover IRA invested purposefully, not by default, is an absolutely crucial step.